2025 First Quarter Letter

It's been a wild year, rigging myself for the future and new investment pitches.

Dear readers,

Welcome to my first quarterly letter on this platform. I’ve been held back from being able to write my monthly update for March due to work and vacationing coming in the way. That made me think that I might just write a Q1 summary of how things are going.

Wild ride

This year has been volatile. I started with the right idea—overweighting defensives and focusing on counter-cyclical earnings companies like O'Reilly, Linde, Visa, and Hermes. However, I sold too early due to pricing concerns. While profitable, holding these positions longer would have yielded better returns. My "winners for 2025" post has delivered mixed results so far, though Momentum Group, Linde and Topicus have performed well despite market challenges. As Howard Marks puts it well in his newest memo: Nobody knows this time either.

We’ve seen indexes slump at record levels in March and April, hit with the fear of a global tariff war between most developed nations. As Trump gets squeezed by his CEOs on Fox News and the bond market at the same time, the rhetoric backs down. In the end, I have as little clue as to what is going to happen as the next person does.

Thankfully there’s only ~1350 days left of Donald Trumps presidency (buckle up).

Results for Q1

I am at the time of writing (16.04) up by 3.58%. I realized significant gains (+25%) from my lower volatility picks (V, RMS, ORLY) in February. I then rolled most of these gains into new positions. It would’ve been a stroke of genius luck if I had decided to sit on cash for a little while - Oh well, I’ve still got a ton of things to learn about discipline and patience in the markets.

At one point in February, I was up by 16.7%. However, during the worst market drops, returns slumped to negative 4%. I'm knocking on wood as I write this. In the worst of the volatility I committed some trading, falling back to old habits. I’ve been in and out of some very high quality names, mostly following the old Twitter adage valid in bear-markets: Sell the rip (this has obviously not been a bear market quite yet).

My biggest winners in the current portfolio has been: Norbit (+28.3% YTD), Topicus (+22.5%) and Berner Industrier (+20.83%).

My biggest losers have been: SanLorenzo (-12.6% YTD), Harvia (-8% collected across my buying this year) and Evolution (-6% YTD).

Mulling over losses, and deliberate changes

I’ve been quite lucky, having winners that have continued their positive momentum to the extent that they’ve negated my poor picks. I’m not really interested in talking much about winners in a quarterly perspective, it is most likely pure and simple luck. Berner as an example would be in my top three “losers” if it had not restarted it’s acquisition engine in the recents days, but timing guided it into the top bracket of performers.

Now what I want to spend some time reflecting on is bad picks, and selling decisions. As can be seen, two of my three worst performers were the top 2 picks of my 2025 bucket. Both have been sold. The reasons SanLorenzo and Evolution have performed the worst are very different, and probably very much the same at similar times.

My positivity for SanLorenzo this year was based on an assumption that the worst spending pressures were behind us. I reasoned that President Trump would do as he did in his first period leading the country, huff and puff but ultimately give credence to his wealthy beneficiaries and main constituencies. These people would get wealthier, and in result, buy boats. This did not happen, but in my opinion the most negative awakening was the SanLorenzo and yachting is far more cyclical than what I’ve cared to admit. For 2025 and 2026 they need record-breaking order intake just to meet market expectations. This suggests more trouble ahead.

Evolution AB ticks all the quality boxes: elite ROIC, rational growth, and an unmatched position in online gambling. However, the company faced a perfect storm: a doubled tax burden, studio strikes, and illegal streaming in its crucial Asian market. This series of improbable hits created "their worst year ever."

My mistakes with Evolution were multi-layered:

Timing: I bought early dips thinking they were temporary corrections

Analysis: I failed to recognize 2024 would be a recovery year at best following the tax increases

Market psychology: I naively expected a quick re-rating once negative factors resolved, without a new positive catalyst

Strategy fit: Evolution no longer aligns with my evolved investment approach

Additionally, a personal factor influenced my decision: as I begin managing money for my girlfriend and potentially family in the future, I need to respect ethical preferences against gambling investments.

Lessons learned

The key lesson? Be patient when buying but ruthless when selling when your thesis breaks. What looks like a temporary setback can sometimes be a fundamental shift, while some "non-fundamental" changes persist longer than expected. I applied this tough lesson to SanLorenzo, selling when I realized I'd miscalculated the counter-cyclicality of luxury yachts.

Does this mean Evolution is doomed? Hardly. My paranoid investor brain suspects I've sold near the bottom, and existing shareholders may well prosper going forward. But that's precisely the lesson—pragmatism over dogmatism, focusing on where my conviction and understanding are strongest.

On the topic of selling, I remember reading something by an investment legend that I can’t remember the name of now (it might’ve been Stanley Druckenmiller). He discussed selling, and how they were ruthless in selling losers, because you never know why an investment is bad until the damage is done. This always struck me as a faulty way of thinking: If you just sell bad timed buys into great companies, then you will miss out on a lot of great cases, wouldn’t you? I think that’s still a valid point. But my thinking was also based on a far too high confidence level: I assumed that I’d know the future better than mr. Market, that’s too cocky.

The key takeaway from Evolution and SanLorenzo: be ruthless with underperformers. There's no medal for enduring drawdowns out of stubbornness.

Looking deeper, these seemingly different companies shared two critical similarities:

Technical pressure: Both faced severe negative price momentum that created its own downward spiral.

Fundamental narrative shifts: Both transitioned from growth darlings to companies with uncertain futures.

While technical factors aren't fundamental, they matter significantly in today's market. The momentum effect is powerful—evident in how the strongest momentum stocks led the recovery after recent tariff volatility. I haven't found a systematic way to incorporate momentum into my process yet, so I stay neutral to this factor in my own process.

More importantly, I've been studying fundamental momentum—when a company's trajectory meaningfully changes direction. Both Evolution and SanLorenzo experienced negative inflection points in their growth stories with brutal short-term consequences. Though both remain quality businesses, I should have been more alert to these narrative shifts, whether in growth rates, returns metrics, or margin structure.

I previously shared a piece from

on identifying inflecting ROICs. These inflection stories represent the most valuable investment opportunities—companies on the cusp of material fundamental improvement. The real gems are businesses beginning trajectories toward better sales, margins, or ROIC (often all three simultaneously). What's crucial is finding these companies before the market fully appreciates their transformation. Norbit exemplifies this perfectly—a company clearly poised to ascend to a higher quality tier before mainstream recognition caught up.Now my goal for my Norbit investment is to ride this out as best as possible. But I also want to impose discipline on myself, and make room for critically thinking about when the next fundamental momentum shift comes - I.e., when is Norbit moving into the category of a story that is slowing down. It will inevitably come. What I’m trying to say is that as investors we must be open to things changing, also for the worse.

Fair play in investing

Recently, I've been questioning the dogma of "quality investing." This approach typically embraces several Buffett-inspired commandments:

Act as an owner

Have no time horizon limit

Never sell as long as fundamentals hold

Buy great businesses at fair prices

While sound as general principles, these mantras can foster dangerous stubbornness—particularly when combined with the conviction required for stock picking. The cognitive dissonance is powerful: if you believe you've spotted value that thousands of other investors have missed, you'll naturally resist evidence suggesting fundamentals are changing. This creates a blind spot precisely when clear vision is most needed.

Following investment dogma—quoting Buffett and adhering to quality investing principles—resembles chasing the "fair play" award in sports. You play honorably but never hoist the championship trophy. Instead, you collect sportsmanship medals and the moral satisfaction of "investing right."

The cold reality is that markets award no points for righteousness. You either outperform or you don't. In the end, we have to balance principles and pragmatism.

This mindset trapped me with Evolution. I clung to "never sell unless fundamentals change" while failing to see that tax hikes, strikes, and cyber-attacks were fundamental changes, even if temporary. During such transitions, a company enters "no-story" limbo with the market, creating valuation purgatory that can outlast your patience.

Is Evolution permanently damaged? My inner contrarian suspects I've sold at the absolute bottom. Current shareholders may well laugh all the way to the bank.

The lesson is crystal clear: pragmatism beats dogmatism every time. Successful investing requires ruthlessly reassessing your positions when evidence shifts, regardless of investment scripture. We invest for decades, but the only constant is change—our approach must embrace this reality, not fight it.

These sales have been a part of another change for my strategy though, which I’ll outline now.

Narrowing my focus further

A theme that has been prevalent through my investing and my writing is having a narrow focus and concentrating my investing process. I want to keep things simple, and spend my concentration and limited ability to learn on a few things so that I can compound not only money but also hard-earned experience and learnings.

This has caused me to shift my strategy. I discussed this on my subscribers chat in Substack, and I’ve decided to go with my gut and go (mostly) into investing in companies that can be categorised as:

Serial acquirers

Investment companies

Holding companies (re-investors)

Monopolies and/or passion projects

This approach is inspired a lot by Req Capital, but I haven’t been able to commit myself to only invest in acquisition driven compounders. But most of my companies share the fact that they are either programmatic acquirers, or that they have done great acquisitions or investment into other firms.

The change is founded in the belief that I can only get really good at a few things. If I focus on companies that generate outsized return from disciplined acquisitions or investment into other companies through surplus cash flows I can get good at identifying these great capital allocators. This can allow me to focus less on the company, product and sector specific themes and more on the overarching theme of acquisitions and investments.

Anecdotally, I noticed that the companies I love to read about shared these dynamics:

Dominant positions in niches

Acquisitions and investments as a core part of their value creation

Great cash generation and counter-cyclical pricing powers

I want to do more of what works, and less of what I haven’t been that good at. I think I’ve developed some basic understanding of how to assess and measure these types of situations. My confidence in assessing other companies strengths and weaknesses, and at least as important potential inflections in these companies, have gotten a hit lately.

Additionally, I believe that these types of companies come with the great benefit of being diversifiers of risks. Through their nodes of investments and group companies they create a robust structure, very much like a spider-web (the strongest natural structure we know, relatively speaking).

The diversification, the compounding time horizon available to serial acquirers and the strength of this business model leads to some very excellent opportunities and I’m excited to focus more on this business model going further.

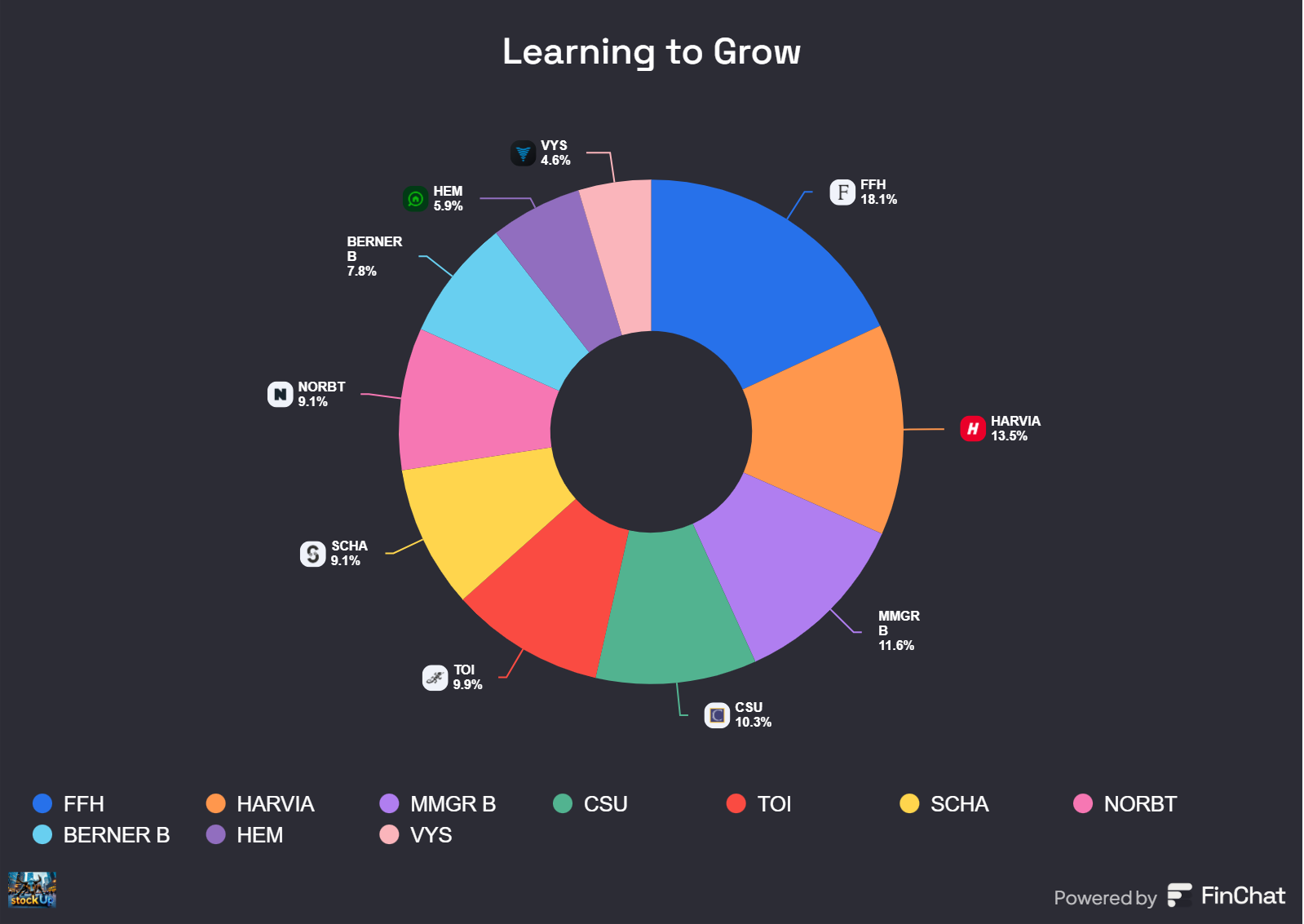

Enough chatter, time to unveil the Learning to Grow portfolio 2.0:

You can see major changes have happened. I am quite optimistic for my companies, several which are in the middle of quality inflections at different points in time.

The various portfolio themes

Serial acquirers (~45%)

My largest bucket, consisting of Constellation and Topicus at 20%, Momentum Group and Berner representing industrial niches and parts acquirers at ~18% and Vysarn (~5%) as a young wildcard acquirer and consolidator of anything to do with water. I could probably have the last one as an industrial acquirer as well, but I think it’s a bit different from Momentum and Berner in how it’s focused on several verticals within the same sector: Water resources handling.

These companies all either have a world-class track record, or are in the midst of turning into quality companies. I’d put CSU+TOI and Momentum Group in the first bucket, and Berner and Vysarn into the quality inflection bucket. The first bunch are priced as such, and the latter still has quite a lot of room to run both in terms of overall growth (the best is ahead of them) and in terms of multiples.

I’ve discussed VMS Serial acquirers and Momentum Group before, so let me spend some lines on Vysarn and Berner Industrier.

Vysarn has shown an incredible ability to consolidate across all the water verticals in Australia. It’s got some very interesting new additions made to it’s portfolio in the second half of last year:

1. Expanding into eastern Australia through the acquisition of Waste Water Services and more importantly CMP Consulting. These additions should allow Vysarn to ride the infrastructure investment and upgrading that is bound to happen as the climate shifts more volatile and hot.

It’s launched Vysarn Asset Management, focused on water asset management in Australia can provide some excellent quality inflection by moving them towards more asset light management parts of the business.

These two changes can prove to be incredibly powerful for Vysarn, turning the income stream to less cyclical parts of the water industry in Australia. This is a highly attractive resource and segment for our time on earth, and I suspect this might very well be a very early inning for the potentially great story that I hope Vysarn will turn out to be. Find a great video pitch on Vysarn here.

Berner Industrier is far more dull. This is a 100+ year old company that has operated in the industrial trading segment of the nordics for a long time. They have since 2021 been through several changes, which can quickly be summarized as: Step 1. Organisational shift from centralisation and synergistic focus to a decentralised structure. Step 2. A deleveraging and profitability focus that has created a robust cash flow and balance sheet rigged for growth, and now finally Step 3. Buying great niche companies in industries with secular tailwinds.

Last week Berner Industrier announced their first acquisition since 2021: Autofric AB. Autofric deals with water industrial components and machinery, and have shown great growth and margins. This acquisition will add around 16% EBITA for the group as a whole on a full year consolidated basis, and in addition strengthen margins. The share price have naturally been rewarded, and we are up around 25% just the last week.

But that does not mean that the train has left the station. We’re trading in the range of 15x EV/EBITA for 2024, and the hurdle rate for Berner to hyper-accelerate their growth is quite low. If they manage to snag one more company with the qualities of Autofric, we’ll quickly see growth in EBITA exceed 30% simply through in-organic growth. Add on that Berner managed to grow it’s cash flow by 25% in Q4’24 and order intake highly accelerated we’ll quickly see three growth engines hit at the same time:

Organic growth accelerating

In-organic growth hypercharging the growth

Market pricing Berner as an niche industrial acquirer and bringing multiples in line with peers (probably 20x EV/EBITA).

Category leaders with acquisition engines (23%)

I need to find a better name for this bucket, but I could’ve just called it my “passion projects” bucket. Within this ~23% of my portfolio we find Harvia and Norbit. These are both great companies that share some similarities despite operating in widely varied segments.

They both have market leading products across price ranges, they’re both really good at bolt-on acquisitions, they’re both head and shoulders above competition in their return on capital metrics and both are positioned within secular trends. For Norbit they’re in the automatisation, robotisation and digitalisation of mobility and ocean mapping and exploration, for Harvia it’s all about wellness, health and the focus on living better lives.

They stand to gain from being better than their competitors in several parts of the value chain: 1. They’re more efficient on costs and production, 2. They have better products, 3. They stand to consolidate their niches through acquisitions.

Both Harvia and Norbit have decades as companies, but in my opinion they share the trait of currently hitting their best stride. The opportunities in these companies exist because the market is underappreciating the longevity of their growth trajectories (particularly for Norbit in my opinion). I’ll be looking to provide a write-up on my thesis for Harvia some time this year, but I’ve covered Norbit extensively in my earlier writings.

Investment companies (~20%)

This bucket holds a large, but single-company position: Fairfax Financial Holdings. Fairfax is a float investor in the midst of a lasting quality inflection. They’re still growing faster than peers, whilst at the same time being cheaper than them. Fairfax holds a sort-of contrarian position in my portfolio. They have a high quality insurance company which generate great profits from a global scale that is diversified in markets with strong secular growth (Gulfs, India, but still most of the insurance business in the U.S.).

Fairfax adds a dimension of value investing to my portfolio, as their investment style is mostly value based (but turning more and more quality at a reasonable price). They have shown remarkable good timing, Eurobank, their largest investment is having a blaster of a year (up 32% last year), and a couple of years ago they invested heavily into Orla Mining, a great gold mining play. These are investments I’d never make for myself, but I’m comfortable delegating these types of investments to Fairfax.

FFH is in my opinion a perfect holding in these volatile times. They have a strong defensive position as P&C insurance is not affected by tariffs, nor by a slowing economy. Quite contrary, insurance tends to outperform in these times. But, the canadian insurer have the ability to go on offence if volatility really hits, as it has what we can describe as a fuck-ton of cash and cash-equivalents through short-term bonds. If we face even worse market conditions than what we’ve seen in March and April, Fairfax can capture future returns either through rolling their bonds into higher yields, or taking out cash and start investing into cheaper and greater equities.

We also have a rather high certainty on the operating income (insurance and bonds yields, i.e. defensive incomes) will stay strong for the next three years or so, meaning that the foundations of Fairfax are as solid as ever.

Now add in the fact that Fairfax is a veritable babushka doll of value, I’m super comfortable having this as a large and outsized position. At ~2000 CAD Fairfax Financial Holdings is priced at ~0.8x it’s investment float, and around ~1.3 it’s price to book (which is comfortably growing 15-18% in the next few years). What the float pricing tells us is that the market is pricing Fairfax’s insurance business at a discount, in my opinion a ridiculous conclusion by mr. Market. If you price a company that has been able to grow its investments by around 16% annually at a discount, I’m happy to take a position.

I expect Fairfax to compound its book value by 12-15% annually. Share price growth should follow a similar trajectory. But, the real kicker is how there’s layers upon layers of positive optionality with the company: 1. Steady buybacks and dividends at around 3-4% annually as long as mr. Market underappreciates the company, 2. A re-rating of its insurance float to at least the share being worth 1x the float (but honestly it should be rated at around 1.3-1.5x), 3. A rerating of Fairfax investment ability, leading to a higher appreciation of its assets and equities.

I’m comfortable with the baseline return profile being linked to the book value accretion, but I see great potential for the market realising it’s mistake in either point 1, 2 or 3.

Online classified groups (~15%)

My newest portfolio addition is online classifieds (~15%), represented by Schibsted ASA (soon to be renamed Vend) and Hemnet AB. These businesses possess underrated moats and exceptional cash flow characteristics.

Initially, I questioned their capital redeployment opportunities, wondering if their ROIC metrics were overstated. I've since recognized their nearly unassailable competitive positions. Even CoStar—one of America's best-run companies—has spent hundreds of millions trying to unseat incumbents like RightMove (UK) and REA (Australia) with barely managing to make a dent in their market positions. Why? These markets naturally consolidate to one dominant player, exhibiting what Buffett called "the economics of the fattest" when describing newspaper dynamics.

In Scandinavia, wealth creation revolves around real estate. When selling what is typically your largest financial asset, you'll prioritize maximum exposure over modest listing fee savings. No rational seller would use a second-tier platform to save 10,000 kroner while potentially missing out on 100,000 in a competitive bidding process.

This creates a virtuous cycle: dominant platforms get all their traffic through organic means. Every Norwegian knows to check Finn.no for real estate prices—it's culturally ingrained. This natural monopoly position enables steady price increases that customers readily absorb.

Another interesting part of this is the economic promise that real-estate holds in our collective Scandinavian minds. A story here is that friends and family often chat about this and that listing of some wild property, or we tend to check Finn.no for listing prices to dream about our potential payday when we can sell and move to a new apartment. Finn and Hemnet function as the toll-booth of our biggest economic ambitions.

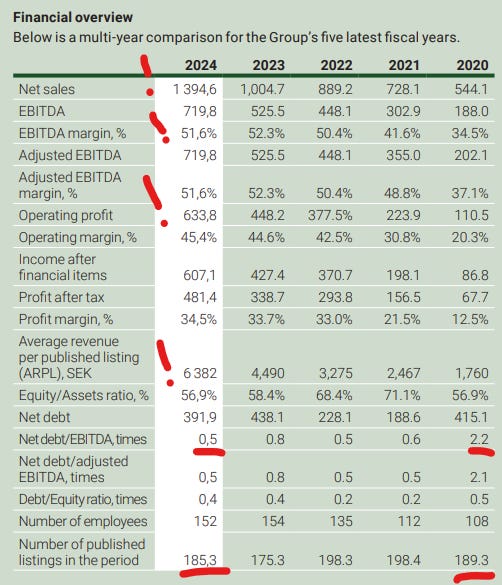

These platforms generate scale economics that yield extraordinary financial results. Consider Hemnet AB: with just 152 employees, they produced SEK633.8M in operating income for 2024—an impressive SEK4.17M per employee. This metric becomes even more remarkable when tracked over time: in 2020, they generated a mere SEK1.02M per employee. This 4x improvement in productivity occurred despite growing headcount by >40%.

What's driving this operational leverage? Pure pricing power. The counterintuitive reality is that Hemnet achieved this without volume growth—their 2024 listing volume was actually ~2% lower than 2020 levels, and they grew by >30% in some quarters in 2023 when they experience volume declines above 20%. This makes Hemnet one of the most impressive scale stories I've encountered.

Now imagine the growth potential if volume growth returns while their commercialization initiatives continue expanding. The combination could supercharge an already impressive trajectory.

Schibsted ASA has historically been a corporate tangle—a collection of media properties and digital platforms ranging from excellent to mediocre to outright poor performers. Following a strategic overhaul, they've consolidated around their top performing assets: Nordic online classifieds including Finn.no, Blocket.se, Dba.dk, and Finnish platforms Oikotie and Tori as the most attractive names holding number 1 positions in their verticals.

While still somewhat messy, their indisputable prize asset is Finn.no's real estate listings—a true pricing-power machine. Their car, job, and re-commerce verticals offer additional value, though with more cyclicality and less market dominance.

Management has executed an impressive turnaround since their 2022 crisis: divesting most of Adevinta (though their remaining equity in the now-private Adevinta represents around 100nok per share of value), shedding the societally important but financially draining news media division, and eliminating cash-burning venture experiments.

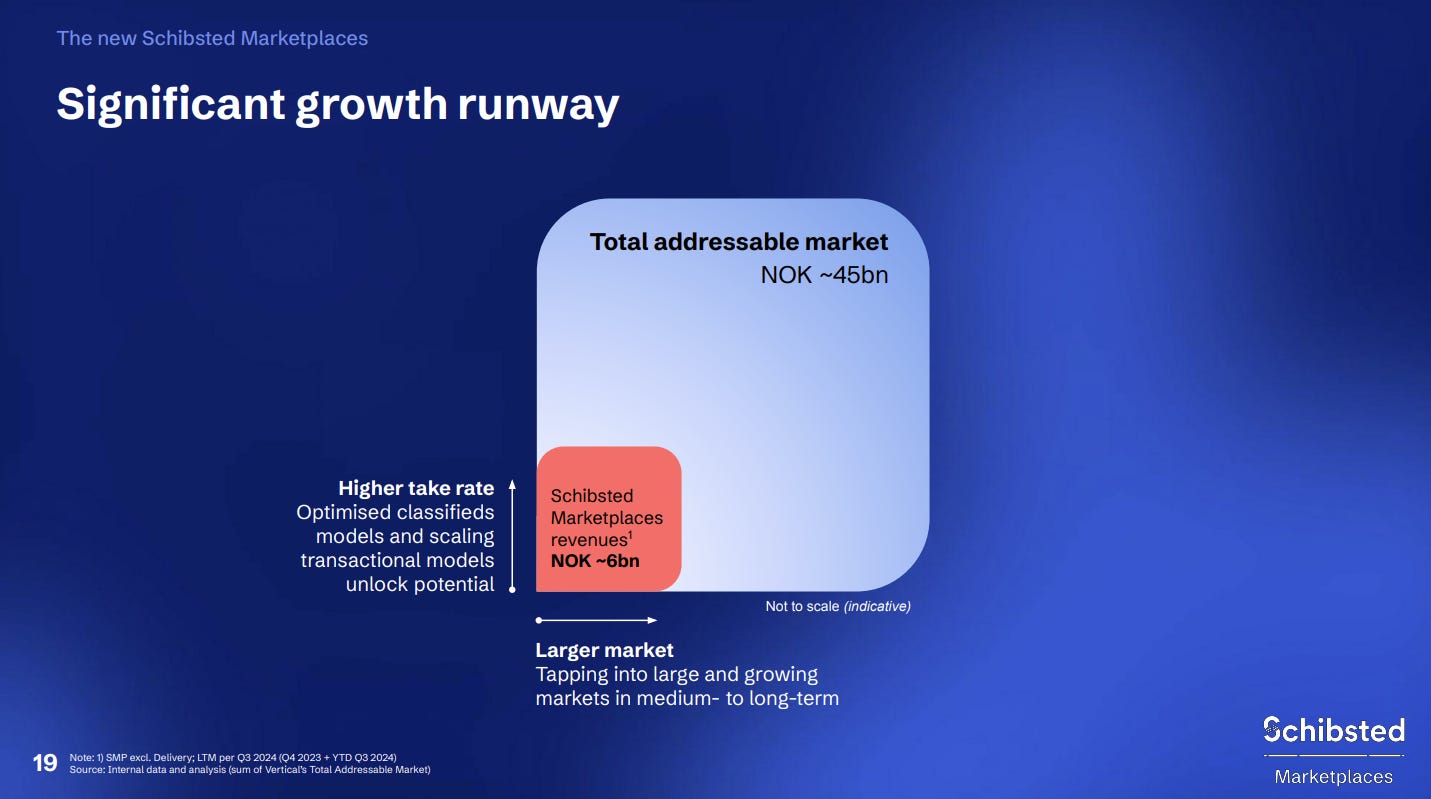

Their upcoming rebranding to Vend (or Schibsted Marketplaces) will complete their transformation into a pure-play Nordic classifieds group with multiple #1 market positions. As with many conglomerates, the consolidated structure obscures the value of individual assets.

Most compelling is Finn.no's pricing runway. Norway's dominant platform for real estate, cars, and jobs is dramatically undermonetized compared to international peers. My analysis suggests they could implement 3-10x price increases by simply matching monetization levels seen in comparable markets like Australia, UK, and Sweden.

My conservative sum-of-parts valuation (attached below) projects 16% annual returns for the remaining parts of Schibsted Marketsplaces even without assuming full pricing potential. If the market properly values their real estate and automotive platforms, returns could be substantially higher—a classic case of an attractive base case with exceptional upside.

The primary drawback is Schibsted's complex structure offering limited synergies between platforms. It's essentially a collection of classified assets under one roof. If Finn.no were a standalone entity, I'd be fully committed at current prices.

My research into online classifieds led me to Hemnet, a Swedish real estate platform that's become a price-setting juggernaut since its 2021 listing.

Hemnet's dominance is staggering: 92% of brokers and 90% of traffic. Its nearest competitor, Booli, captures only 20% of traffic—likely from users who also check Hemnet, meaning no truly unique audience.

The results speak volumes. In just four years, Hemnet has:

Grown operating earnings 6x

Nearly doubled margins

Significantly reduced debt

Achieved 3x topline growth

This explosive performance stems from ruthless pricing power, with their take rate expanding from negligible to ~0.3% of listing prices. Their playbook includes tiered pricing options and broker incentives that share some operational leverage while maintaining their dominant position.

April's introduction of "Max" advertising (priced 25% above their Premium tier) suggests analyst estimates may be too conservative. Looking at comparable monopolistic platforms globally, I believe Hemnet's commercialization journey is still in early stages.

At forward EV/EBITA in the upper thirties, I think Hemnet is extremely high priced, but still priced at a discount to their Australian peers. It still has a lot of room to grow, no commercial competition and a product that can rationally be priced higher through adding services and products that make sense for sellers. Their dynamic pricing and rational parasitic position on the real-estate market is great. We have to hope that for both Hemnet and Finn they can grow into the positive parasites of cleaner fishes instead of leeches, but I’m sure the returns will be great from here on out.

Let’s have a look at the current pricing dynamics between Finn and Hemnet.

Finn is quite a bit behind Hemnet in terms of sheer pricing, granulation and sophistication in terms of pricing. Finn only operates with three tiers, they barely have started selling advertisment tools on the same level of Hemnet and so on. I’m very optimistic that Finn will take the same route as it’s Swedish cousin, especially considering that Vor Capital, the main shareholder of Hemnet has substantially invested in Schibsted.

Before I end this online classifieds pitch I’d say that the read-across from Hemnet to Schibsted is quite attractive. Hemnet has raised its prices by 5x since 2019, and their base in 2019 was priced higher than where Finn is pricing their listings today. In addition to this, the market position of Finn is even better than what Hemnet has, where the only competitor to Finn was started in the middle of 2024. Good luck to them I’d say, I’ll be interested to see for how long they can manage before declaring bankruptcy.

If you’ve enjoyed these pitches, feel free to contribute to my caffeine addiction by donating a cup of coffee.

Wrapping things up

Q1 has been a very interesting time in the markets. I’m both happy and disappointed with my navigational skills. I had the right trajectory, but I turned a bit too fast, and got hit by some headwinds that I could’ve avoided.

I’d like to end by reminding my readers that I’m still just a happy amateur, fumbling my way through investing. I’ve spent a considerable amount of time being disappointed in myself for closing the position on names that I’ve been bullish on because I’ve feared readers have taken my bullishness as a signal to either buy or hold the companies. I want to reiterate that you should not listen to me. I have no formal training, and I am still very much a beginner. If my writing gives you inspiration to look at companies, I am happy to hear that - but always act based on your own research and conviction.

Outlook

Looking ahead to Q2 and beyond, I'm cautiously optimistic despite ongoing volatility. My repositioned portfolio now emphasizes capital allocation excellence through serial acquirers and investment companies, which should provide both defensive characteristics and offensive optionality. I'm particularly watching for acceleration in Berner's acquisition strategy, continued fundamental momentum in Norbit, and potential multiple expansion in my undervalued online classifieds holdings. While macroeconomic uncertainties remain—particularly around tariff policies and interest rate trajectories—my portfolio's focus on high-quality compounders with pricing power and reinvestment opportunities positions us well for long-term outperformance regardless of short-term market conditions. I'll continue refining my investment process, focusing on fundamental momentum shifts and being pragmatic rather than dogmatic when evidence suggests a change in thesis.

Let’s keep on learning and compounding, and if you have made it this far - thanks for reading!

Kind regards,

Mathias

As always: None of this should be understood as investment advice. I am a hobby investor, with no professional training. I may sell or buy stocks without disclosing it at once, so you should not be following me. Do your own research, or you are bound to lose conviction when convicition matters.

Thanks for the mention. Norbit sits on my watchlist btw.

Interesting. Basically the opposite of what I've done. I bought more Evolution and Sanlorenzo.