A piece of finance history

A piece of finance history

I've read a 14 year old report covering the dotcom, housing crisis and beyond looking for the answer to what created shareholder returns in the most turbulent market periods within my lifetime.

I’m personally a really fresh investor. That means that I’ve not been active, nor experienced how it is to invest in markets that either go sideways, or down for longer periods of time. Having been invested since around 2020 (slowly moving towards building my own stock portfolio over the last two years), I’ve simply not been exposed to rough markets yet.

Of course, I was active during the market downturn of the summer to fall of 2022. For some stocks this was quite the hefty correction, and I did hold a bunch of stocks that performed rubbish. So I’ve had the pleasure of seeing my holdings fall by quite a lot, and how that led me to do a bunch of dumb stuff, and some smart stuff. But at the same time, the markets picked up quite rapidly into 2023 and now there’s nothing but blue skies on the horizon.

Companies upping their guidance, talking about AI and splitting shares to make shares more accessible to retail investors have been the winners during the first quarter of the year. Cyclical retailers and consumer companies have been punished across the line, and I’ve seen company after company get punished after not upping guidance. I don’t know what’s coming, as I still haven’t achieved the ability to look into the future, but it does make me think on how I can prepare myself for a change in sentiment and market conditions. My portfolio has been mostly flat these last months, so I don’t feel any pressure at all, and a couple of months is nothing to write about.

Trying to learn from history

This thinking has led me to look at periods of underperformance and troubling market conditions. One interesting report that I’ve come across is Boston Consulting Group’s Value Creation report from 2010.

You can skip reading my thoughts, and just read the PDF here if you want.

This report was launched the year after what probably was the deepest bottom in the financial markets in my lifetime (born in 1993). The report discusses what has driven returns for shareholders over ~20 years, with a lot of different market cycles affecting returns from stocks.

The time period covered by the report was a very interesting period. From the ‘90s to the Dotcom bubble, the markets presented a fantastic return, that burst violently in 2001 after rallying for 5 years or so. After this, the markets lagged but eventually recovered only to be dragged down again by the housing bubble burst, which made the stock markets perform poorly until it bottomed out in 2009. The BCG report looks back at a time period with great turbulence, and should in my opinion give insight into how markets perform under what are some dramatic contexts.

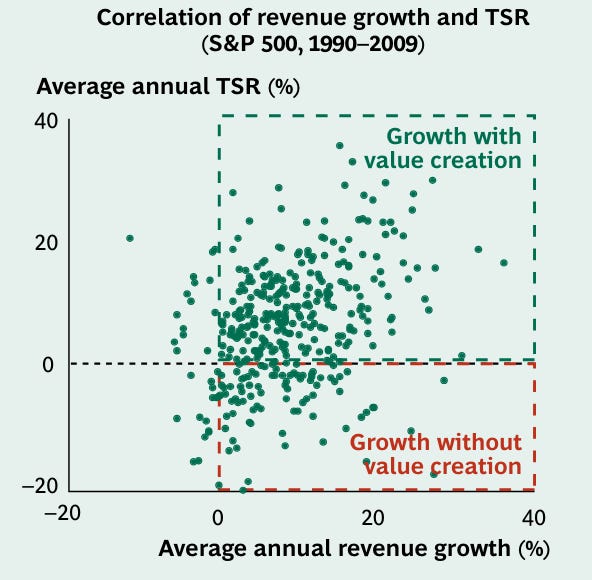

The shared traits of stocks that returned great shareholder value

The above graphic is from the report, which illustrates what characterises the companies with the best total shareholder returns (TSR) for the 19 year period of ‘90 - ‘09. There are several implications we can take from this graph:

As most investors know, what drives shareholder returns over longer periods of time is mostly the fundamental growth of the company’s earnings and margins.

For the three first years, what price you pay for a company (multiples) had the largest impact on returns.

What I found surprising is the impact free cash flow (FCF = FCF-yield) has on the TSR. Dividends and buyback had a limited implication for TSR, but less and less the longer you own a company.

But there’s always exceptions:

As we can see, revenue growth does not always lead to TSR. The bottom of the right corner of the spread plot is companies that have increased their revenues over the period of time, but have lagged behind on returns.

BCG gives two main reasons for this:

Multiple contractions

Margin contractions

I.e., if you buy a company at high multiples and margins, revenue growth would not be enough to create shareholder value. Given the time period that the report looks at this is in my opinion an interesting learning, as people keep investing into the growth story of various AI or technology companies

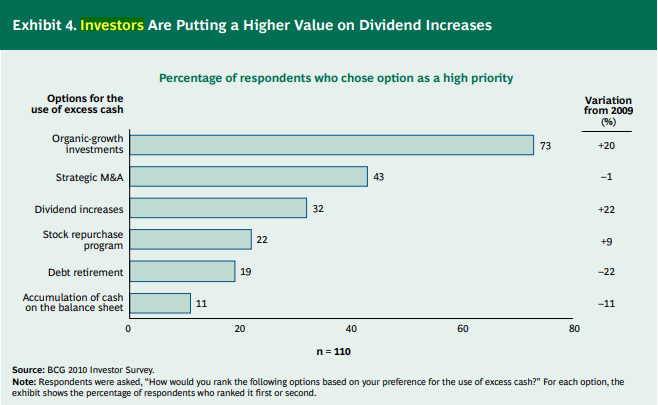

What did people look for in their investment between ‘90 - ‘09?

Another thing I find really fascinating in this report is the discussion on what shareholders prioritise in their investment. In their 2010 investor survey, BCG found that they prioritised organic-growth investment at the top (73% of respondents valued these investment), 43% strategic M&A activity and 32% dividend increases.

I find this to be an interesting insight into how investors thought about their investments in an uncertain time. Dividends were fairly high on the agenda, whilst most of the investors prioritised organic growth. From 2009 to 2010 these two factors were the top growers in what investors valued.

This leads me to think that in troubled times in the market investors will be looking to own assets returning cash to their shareholders, and growing organically. This is very much aligned with my own portfolio, where my goal is to find quality companies, growing at a reasonable pace and with strong market positions.

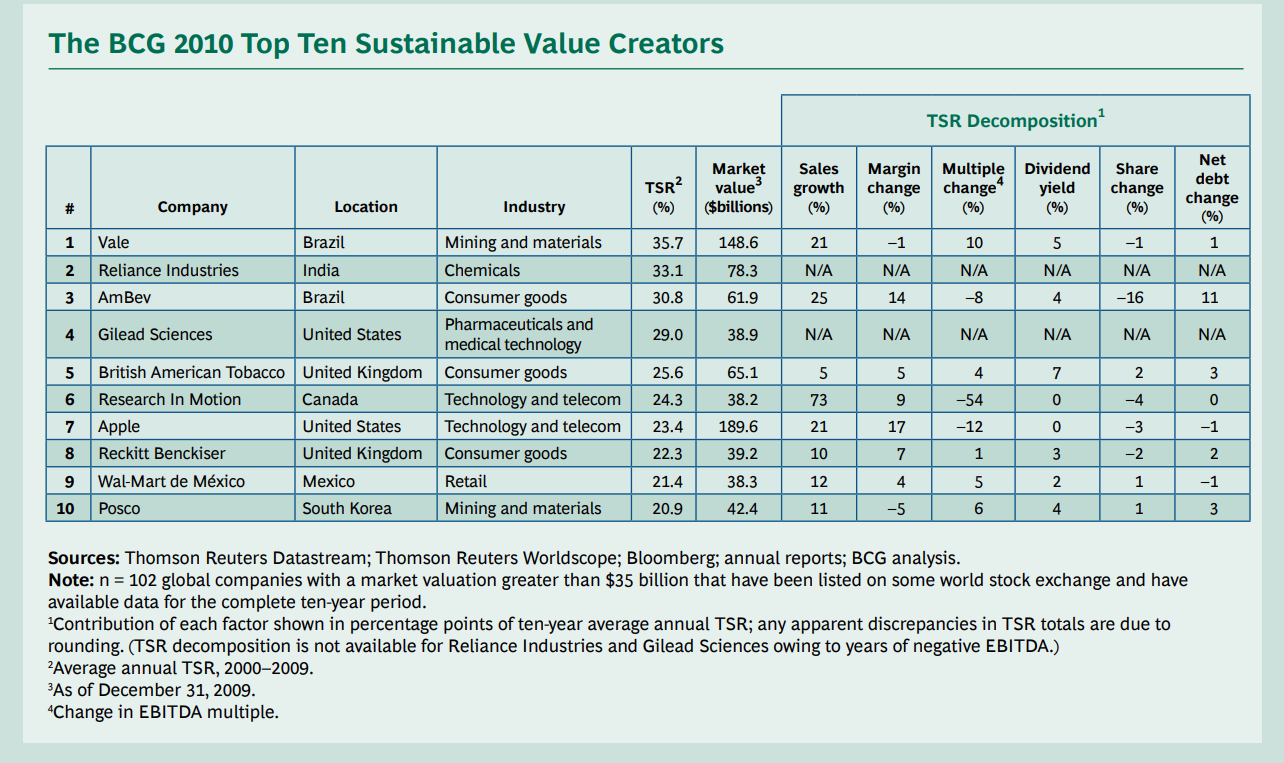

The BCG report also shows what companies that generated the best shareholder returns in the period of 2000 - 2009:

It’s interesting to note that despite a lot of what we now know as great technological companies such as Amazon, Microsoft and Broadcom are missing from the list. The only big tech company on the list is Apple. The best returns for shareholders were gained from what are unpopular industries in the current stock market: Mining, chemicals, consumer goods and so on. There’s another interesting insight to be gained, and that is the global flair of the list. The U.S is tied with Brazil for the country with most companies in the top ten.

It’s not surprising that there’s an absence of tech companies in the list. The dotcom bubble burst was a violent drawdown that shook the confidence in the sector at its foundations. However, had one started investing into rising tech in 2009, the total shareholder returns would have been amazing. Easy to say with the power of hindsight, and I’m willing to bet that few of the BCG reports readers takeaway in 2010 would have been that it was time to invest in technology.

Another lesson learned here for me is hard assets and ability for a stable and growing revenue drives shareholder returns in more troubling markets. I’m not saying that anyone should run and buy mining companies and Mexican retailers. My approach has been to find companies with defensive characteristics in their revenue growth. As a shareholder I want my companies to be able to earn money despite depressed macro conditions, with products that there is a demand for even in downturns.

I believe my portfolio has some great examples of companies with these characteristics: auto part retailers (ORLY), growing defensive consumers (Dino Polska), insurance companies with pricing power (Kinsale Group) and true high end luxury (SanLorenzo).

Did you find this article interesting and helpfulfor your investment process? This substack will remain free for the foreseeable future, but I would be very happy if you pitched in for a cup of coffee.

Wrapping things up

The BCG report from 2010 is a very interesting snippet of investing history. They look back at times of euphoria and great depressions, and some of the years with the most volatility that have been observed in my lifetime. Three things that I take with me from this report is:

The longer you own shares in a company, the more the fundamentals matter.

In the medium-to-short term, multiples and price paid for a company matters (quite a lot).

In troubled times, the sources of total shareholder returns expand beyond the U.S. market and into sectors in which cash is generated and returned to shareholders.

I want to end with a graph that illustrates one of the edges an individual investor should strive to work towards: Longer holding periods. Since the 70s, the average holding period of stocks have plummeted:

It’s also interesting to see that in downturns (1987, 1999-2001, 2008) holding period goes notably down (i.e. selling due to market sentiment). The average holding period of shares are now below a year, which means that the metric that drive total shareholder returns for most equity holders is the price you’ve paid for a company.

I’m working on my own patience and discipline, and I have a goal to be less active in markets. My first two years I’ve bought and sold companies far to often, and have recently become better at acting like a long-term owner of small pieces of businesses. However, with a limited cash pile (as I’m rather fresh I want to inject as much of my money into great companies that are reasonably valued) it is hard to let apparent opportunities pass me by.

A couple of things I’ve done to discipline myself lately:

Delete the brokerage app from my phone.

Turn off any stock related alerts.

Stopped reading financial news outlets daily (I catch up with news a couple of times a week).

Investing should not be entertaining. It can very well be interesting and stimulating, but should never be about getting a kick. Paying attention daily to everything is probably doing retail investors a disservice, and aligning their interests with short term valuation changes and not fundamental company-level growth.

Nothing I’ve written in this article should be understood or interpreted as investment advice. I’m a simple hobby investor who likes writing, and I am not competent or qualified to be giving investment advice. Do your own research, be critical of my assumptions and look into the companies discussed before making any investing decisions.

Thank you for the thoughtful and elaborate comment Magnus! I agree with what you write, and try to work towards all of these things. Worry less, save better and find my style.

In my first three years of investing I’ve been back and forth on whether to index or invest in companies. After “missing” learning about economics, companies and business I’ve landed on that I want to put the work in 😊

Also, I hope the post doesn’t seem to much of a “I’m worried about what will happen”, as I hope to have constructed a robust portfolio that fits my temperament (as you very rightly point out). My goal was mostly to try to learn something from history that I did not personally experience. As the romans said “if you want peace, prepare for war”. The BCG report is an interesting glimpse into the dynamics of a market I never got to experience.

Personally, what I find most interesting is the time tradeoff between multiple effect on total shareholder returns and revenue growth. The investment time horizon should be central to how one analyse an investment.

This is my advice for young investors after over 30 years of investing.

Rule 1. Invest (at a steady pace).

Rule 2. Worry less about what you invest in.

Rule 3. It isn't a defeat if you find out that investing is not for you. Index funds are a great saving vehicle.

1. If you are interested in economics, markets, and equities, study finance but not primarily for picking the next Nvidia. Study to learn more broadly. Find an investing style that suits your temperament etc. The main point is that you invest and let compounding work for you. Build that savings muscle. When you get older and your pot of money is larger you can employ what you have learned to great effect. It takes time to be a good investor with both ups and downs along the way.

2. Let's say you have invested $1000 in Nvidia, and now you have $2500. This is great! But in a lifelong financial journey this return isn't going to mean much. In the long run it is much more important that you don't forget about rule number 1. The same goes for losses. In the great scheme of things, it doesn't mean much when you are young, still learning, and operate with small funds. You will bounce back. Believe me! Thus, worry less about individual stocks, live more, and focus more on learning than getting rich fast.

3. Investing is not for all. Parts of it can be viewed as boring. Valuation., listening to earning calls, reading quarterly reports etc. If you find that this is too boring. It is not a defeat to just say; I want to spend my time doing stuff I find more fun , sexy, or whatever. Index funds are there for all. You are not going to be the next Buffet by indexing, but you can retire in style just by letting compounding work on autopilot.