Connect the dots - Deep dive into Norbit Connectivity

Guest deep-dive, written by Erik Stangeland, originally written in Norwegian and translated for readers of Learning to Grow.

Before you read

The article is a spare time project I (Erik Stangeland) have been working on during the summer of 2024. The purpose of the article is for the reader to learn more about NORBIT, and NORBIT’s business segment Connectivity, in order to be able to make their own assessments of the business segment and the company as a whole.

The translation is done by the author of Learning to Grow, with the intention of making this valuable piece of research more widely available. All credits and (well deserved) applause should be directed to the author.

The article contains suggestions on what the value of Connectivity is. The content is not intended as investment advice. Any errors in facts, figures or other information may occur. NORBIT ASA or related representatives have not reviewed or approved the contents of this article. The information in the article has been obtained from sources believed to be reliable, but no guarantee is given that the content is complete or accurate.

The original date of publishing was 19.09.2024, written in Norwegian.

As source coding and some images got a bit messed up in the formating from Word to Substack, I recommend reading in PDF form - however for those who prefer the accessibility through the Substack platform, all the material is available in this article. You can find the PDF article below, with original formating:

For some broader strokes introduction to Norbits business model, you can read my (Learning to Grow) not as-deep dive into Norbit from this spring:

Author information

Erik Stangeland, 23 years old, fourth year student and member of “Børsklubben” at NHH – Norwegian School of Economics, celebrating my 10th anniversary as a stocks and company analysis enthusiast this year.

Contact info:

Mail: erikmls@hotmail.com

X/Twitter: @erik_stangeland - https://twitter.com/Erik_Stangeland

Introduction to NORBIT

NORBIT is one of those companies that checks most of an investors lists of qualities. With this I’d list these qualities:

They have been growing for a longer period of time,

Margins are strong,

High return on capital,

Diversified revenues both geographically and product-wise,

Several independently successful product launches across segments,

Integrated business model with design, production and sales,

Strong counterparties in contracts,

Bright prospects for their future,

Good capital allocation,

Low debt and good cash conversion,

Insiders own large parts of the company,

Relatively small company in a stock exchange context,

They receive little attention in the media and from brokerage houses.

As we can understand this is an attractive set-up for a long-term investment. In this article, I aim at providing color and flesh out the various points listed above. NORBIT’s headliner segment is the Oceans segment, where the company develops and sells tailored technology for underwater use. Most of the revenue and growth comes from their portfolio of underwater survey and security solutions. During the writing of this article, NORBIT announced the acquisition of German Innomar - a deal that seems to be very favorable. With this acquisition, it is evident that NORBIT is positioning itself to be a highly relevant supplier in the growing market for underwater acoustic survey systems.

When investing in NORBIT, big parts of the group revenue is from the Connectivity and PIR segments in addition to Oceans. While Oceans is often seen as the most attractive segment, the other two are still crucial to the group. The Connectivity segment is expected to be a key growth driver for NORBIT. Therefore, I aim to raise awareness about the strength and potential of the Connectivity segment. Given the challenges I faced in finding detailed information while writing this article, it’s no surprise that Connectivity is less understood and discussed. In this piece, I’ll explain what Connectivity does, the markets it serves, and the key drivers behind those markets.

The connectivity business has been built brick by brick from scratch for almost twenty years. In the last couple of years, growth has been notable. The segment is divided into ITS (intelligent traffic systems) and Smart Data. The most important products in ITS are DSRC (dedicated short-range communications) modules for toll collection, DRSC modules for use in smart tachographs and products with satellite communication, e.g. for distance-based road pricing. Smart Data consists of the Hungarian company iData, which it acquired in the summer of 2021. iData's core offering is its iTrack GPS tracking system, which it sells as a subscription service to transport companies. As we can observe, it’s an interesting integrated platform combining hardware and software as a service model. The DSRC modules are exposed to razorblade-economics with continues improvements and replacement needs, while iData gives customers a powerful data collection platform to optimize their operations.

There have been considerable volatility in Connectivity's revenue and profitability in recent years. A strong 2019 was followed by a challenging period during the COVID-19 pandemic. The development after the pandemic has been very strong, driven by several large contracts within ITS and strong development in iData since the acquisition.

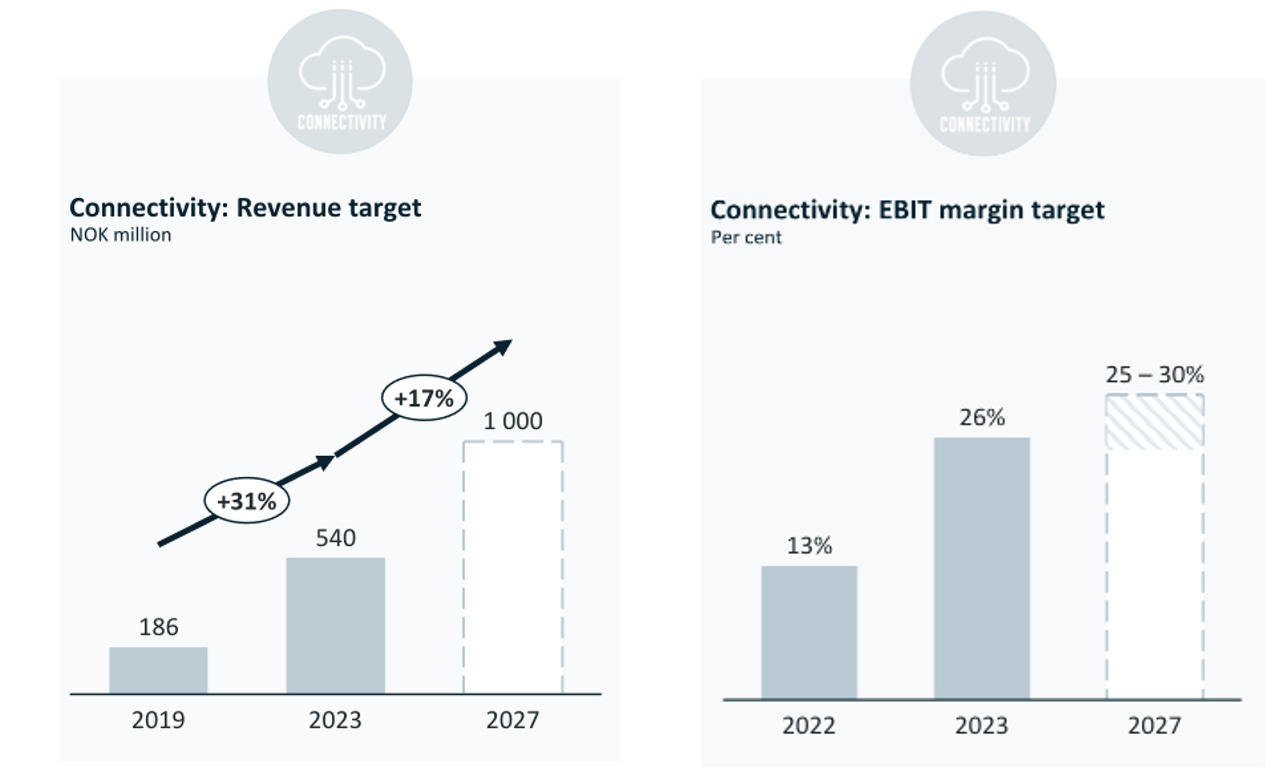

There are also expectations of continued growth in the Connectivity segment. During the presentation of the full-year report for 2023, NORBIT announced new medium-term targets. For Connectivity, this entails a target of reaching NOK 1 billion in revenue, corresponding to a compound annual growth rate (CAGR) of 17% from the full year 2023, up to and including 2027. In addition, they are aiming for an EBIT margin in the 25-30% range.

Due to limited access to valuable information about the Connectivity segment, it has been challenging to assess the quality of this business area. The historical revenue development and profitability suggest that they have managed this segment well and taken good reinvestment decision both with acquisitions but also in driving organic growth. The question we investors should ask ourselves is: how sustainable is this development and can it continue?

In this article, we want to uncover the factors that has driven the good growth over time, explain their current position within their sector, and give a detailed overview of the history of their connectivity business. We will also show which markets they serve and try to illustrate their current market position. The aim is to give you, the reader, enough information to make your own assessment of the quality and value of NORBIT Connectivity.

In the article, we first review the products offered under ITS (Intelligent Transport Systems), then go through Smart Data and the acquisition of iData. If you're interested enough to make it to the last part of the article, I offer some ideas and suggestions for what the value of NORBIT Connectivity could be if it were a standalone company. In the Smart Data section, we present a relative analysis with the Swedish company Opter AB. Finally, we do an isolated value attempt for the the ITS part of Connectivity and then find a proximity for the value of the entire business of Connectivity. We conclude with the value of connectivity in the broader business context of NORBIT.

ITS - Intelligent traffic solutions

DSRC On-Board units

The story behind NORBIT’s automatic tolling tag adventure

Until the acquisition of iData in the first half of 2021, NORBIT Connectivity were mainly an Intelligent tolling systems business (ITS). The origins of ITS come from a collaboration between NORBIT’s subsidiary Fenrits and Lyng Gruppen's subsidiary Lyng Elektronikk. Fenrits developed an automatic road toll tag (further referred to as a toll tag), and Lyng Elektronikk manufactured the tag. These are commonly reported under OBU (On-Board Units) in NORBIT’s reports.

The Norwegian road development has over many years been heavily financed partly through road tolling, and tolling units have been a part of the Norwegian car owners consciousness over several decades. A Norwegian company called Q-Free held a strong, monopolistic position in the production and development of tolling units for (amongst others) the Norwegian market over a long period of time. NORBIT made their breakthrough in 2005 when they broke said Q-Free's monopoly on the Norwegian market. A four-year framework agreement was signed with the Nowegian road authorities, under which both Q-Free and NORBIT were approved as suppliers of toll tags to Nowegian road authorities (Statens Veivesen).

At the time, these contractual collaborations between NORBIT’s wholly owned subsidiaries and external partners were a method NORBIT used to reach out to customers. They designed products and collaborated with relevant and serious players who could take care of bringing the product to market. Looking at the acquisitions NORBIT has made in recent years, it is clear that they are now in a position where this has been turned on its head. Other companies now want to be under the wings of NORBIT's marketing apparatus. There has also been M&A moves from NORBIT to further integrated their product value chain, to gain better control and achieve scale advantages. Anyways.

International expansion began as early as 2008, with contracts in Germany and Austria. The tolling tag business quickly became significant for NORBIT, and they wanted to invest long-term in its further development. In 2009, NORBIT acquired Kitron Microelectronics in Røros, together with 35 of its 52 employees. At the time, the manufacturing company had cut more than half of its employees following the financial crisis. NORBIT bought 45% of the shares and the factory employees bought the remaining piece of the production facilities, thereby creating a collaborative ownership structure. After the purchase, NORBIT had its own manufacturing company, which was named Norbitech.

It was the Norwegian Public Roads Administration that was responsible for awarding contracts for the purchase of toll tags for Norwegian cars. As with many other public contracts, the way these contracts were awarded was by winning a competitive tender. There were several specific requirements that the tolling tags had to meet. So, what NORBIT mainly were competing on was the price per tolling tag. In 2011, NORBIT won more than 80% of the volume in that year's tenders. Since then, NORBIT has been the undisputed market leader for tolling tags in Norway. CEO of NORBIT, Per Jørgen Weisethaunets simple explanation for this: "We have efficient production and low costs at all stages."

In the article where this quote is found, the competitor Q-Free elaborates on how they are struggling in the Norwegian market.

In just a few years, NORBIT gained a strong market position in the Norwegian market for tolling tags for passenger cars. This market position in Norway has played an important role in the international expansion of ITS. 2013 was also a good year for NORBIT Connectivity. They continued to maintain their market share in Norway. In addition, they continued to build customer relationships abroad and signed a major contract in France. In other words, their tags have had a presence in several major European countries for a number of years.

Function of the tolling tag

Toll tags are small gadgets that you attach to the windshield of your car. They communicate wirelessly with toll stations and have a lifespan of several years.

Toll roads are far from new; in fact, they have existed in Europe for thousands of years. Quite simply, tolls are what you pay to use a road. The money is used to finance maintenance and the construction of new roads. The Industrial Revolution in Europe created a growing need for efficient ways to transport goods and people. In the 19th century, governments introduced more formal toll collection systems. Toll collection then became more organized, with toll booths placed along key road sections. The revenue from this system has played an important role in the development of Europe's road network, facilitating interaction and economic growth.

In the Second World War, both British and German forces used a form of RFID technology to identify friendly and enemy aircraft. The system was called IFF, which stands for "identify friend or foe", and used radio waves to distinguish between friendly and enemy aircraft. In the 1980s, RFID technology began to become commercially available. In simple terms, RFID is a technology that uses radio waves to read and capture information stored on a tag attached to an object. This was the start of a major streamlining of toll collection into an automated system where you don't have to find change and stop at a toll station.

In the tags we use today, you'll find CEN DSRC technology, which has been developed specifically for use in transportation and traffic management. Its characteristics are that it provides efficient and reliable enough communication, suitable for use in vehicles traveling at high speeds on multi-lane roads. In other words, this technology is a specialized form of wireless communication based on the principles of RFID. Today, this technology is found in over 100 million toll tags and is the technological platform from which NORBIT has developed a curated product portfolio within the ITS sub-segment of Connectivity.

task of the tolling tag

The tolling tag performs an important task in modern mobility. The biggest benefits are:

Improved traffic flow: with a toll tag, vehicles can pass through toll stations without stopping.

Automated payment: The tag automatically detects the toll pass and bills a precise amount from the road user.

Reduced administration made possible by automated payment: Without manual collection of tolls at toll booths, a lot of resources is saved.

Control and overview: Road users can easily manage their toll tags, monitor consumption, and control payments.

In many cases, improved traffic flow is the main motivation behind the introduction of tolls. They are increasingly being used in cities around the world as a tool to prevent traffic jams that cause long travel times on short stretches of road. This is done by introducing fees for the use of certain roads or areas, mostly during rush hours and adding extraordinary prices in periods of rush hour. It can also be done by adding fees in specific geographical areas (I.e. zone pricing). Another argument for congestion pricing, which is often mentioned, is improved air quality.

Tolling stations can also be used as a tool to regulate traffic. Regulations is typically achieved by erecting toll rings in several of the busiest areas and cities. The cities of Oslo, Bergen and Trondheim were the first to introduce toll rings. This happened between 1986 and 1991. Today, there are over a dozen toll rings in Norway. This development is becoming more and more common in EU, in attempts to regulate down car traffics, emissions and to create more accessible cities centres.

Main applications

Otherwise, tolls are mainly used on highways and main roads:

Toll roads: Tolls are used to finance construction and maintenance, especially in countries with large networks of highways. This is a way to distribute the cost to the road user instead over a taxation bill.

Bridges and tunnels: These have particularly high costs associated with construction and maintenance. One example is the 8 km long Øresund Bridge, which runs between Denmark and Sweden. NORBIT has supplied toll tags for this project.

Nationwide systems: In some countries, such as Germany and Italy, there are nationwide toll networks where mainly heavy vehicles pay for road use, based on mileage. This requires other types of toll tags, which I write about in the next part of the article.

The Norwegian geography is characterized by winding fjords, rivers and mountains creating a great need for bridges and tunnels in connecting population centers across the country. Tolls have played and continue to play an important role in the development of many of these. In addition, tolls are used to finance the development of public transport systems and cycle paths. The regional toll company Fjellinjen (in the Eastern Part of Norway), owned 60% by Oslo Municipality and 40% by Akershus County Council, has collected and managed more than NOK 50 billion (equal to around $5 billions) since its inception. The collected fees finances "future traffic solutions in Greater Oslo". You can read more about the project here: https://www.fjellinjen.no/en/about-us

Production

As mentioned earlier, the Røros factory acquired in 2009 is where the core part of production takes place. The factory has seen a lot of changes since 2009. Today, NORBIT is the sole owner of the factory, and it is an important part of their PIR (Product innovation and realization) business segment, which among other things offers contract manufacturing externally and internally in the group. In 2020, they completed an expansion project that doubled the size of the manufacturing area in Røros.[1] This year (2024), investments are again being made in new production lines, which will produce for the ITS segment. NORBIT has a competitive and modern production, characterized by a high degree of robotization.

Before the period 2015-2018, there were around 60 toll companies in Norway, all of which were majority-owned by counties or municipalities, with a mix of private ownership. The national regulation was that before a new road project were to be financed (wholly or partially) by a toll claimant system, there needed to be an independent tolling company for each project. The rationale behind this was to ensure that collections from one project were not used to pay off toll debts in another project, and that road users in one part of Norway did not end up financing road construction in a totally different part of the country. How ever, over time this constructed a far to complex and bureaucratic system.

Historically, there have been state actors such as the Norwegian Public Roads Administration and regional toll companies owned by municipalities/counties. In recent years, there has been a shift in the Norwegian market towards insurance companies taking over the role of issuer. An issuer is a company that enters into toll agreements with motorists. The shift came after the toll reform in 2015. Figure of the toll reform's measures and objectives. The below model is in Norwegian, but roughly translates to:

Main Title: "Measures and Objectives of the Toll Reform"

Toll Reform

Four Sections of improvement of the tolling reform

Transition to 3-5 toll companies owned by the county municipalities

New roles and division of responsibilities in the sector

Simplification of the tariff and discount structure

Separation of the issuer function

Goals:

Efficient toll collection and financing conditions

User-friendliness

Better facilitation for governmental control and oversight

The 2015 toll reform reduced the number of toll companies in Norway from around 60 to five county-owned toll companies. In addition, toll road companies or companies in which a toll road company is a participant should not be approved as issuers. Reforms take time and has been running since 01.01.2019.

In August 2020, 1.5 years later, Fremtind Forsikring acquired the largest toll issuer in Norway, Fjellinjen, which was subsequently renamed Fremtind Service. Having an insurance company take over the role of issuer makes it easier and more transparent for both motorists and companies to manage their toll agreements. Toll payments are part of everyday finances, and with this acquisition, customers of two of the largest domestic banks in Norway: Sparebank 1 and DNB, which own Fremtind Forsikring, gained access to an overview of their toll subscription in their mobile bank, with ongoing deductions from their account, easier handling when changing cars, and fast roadside assistance. As an insurance company owned by major banks, Fremtind is well positioned to handle large volumes of transactions efficiently.

In the spring of 2021, Fremtind Service acquired another issuer, and today they deliver over 1.9 million tags to 1.4 million customers. On September 1, 2024, Fremtind Service changed its name to AutoSync. Another major voucher issuer, Flyt, was acquired by Gjensidige Forsikring (the largest insurance actor in Norway) in the summer of the same year. Both issuers use NORBIT as a supplier of payment tags, illustrating NORBIT’s dominant position in the Norwegian tolling tag production market.

In an interview with TV2 published on 17.01.21, Svein Skovly, head of Fremtind Forsikring's innovation lab, says that they want to be able to offer additional services through the tolling tag. This was followed a couple of months later by the announcement of a collaboration with NORBIT on the development of future solutions for bomb tags, as well as deliveries of bomb tags themselves. The first item on the agenda was the development of automatic notification systems related to crash or accidents.

Strategic shift

However, NORBIT has their aim on more than the Norwegian tolling tag markets. In recent years, NORBIT has focused on shifting its business model for OBUs from public tenders to business to business (B2B). This gives NORBIT the opportunity to be a technology partner, working together with other private players to provide a broader offering, rather than just competing to deliver a standard product at the lowest possible price. By being a technology partner, they also build long-term relationships, which creates switching costs and greater threshold for dropping NORBIT as a tolling tag supplier.

In public tenders, switching costs must be kept to a minimum, which makes bidders vulnerable to competition. The risk of losing the next tender round is high. NORBIT was on the winning side against Q-Free, but what’s to stop other actors from doing the same to NORBIT?

Fortunately, NORBIT has been very successful in shifting its focus away from public tenders. This has resulted in large business to business (B2B) contracts outside Norway. Some of these B2B-deals account for large parts of sales, which means that revenue from OBUs can be very lumpy, both from quarter to quarter and year to year depending on when a large customer places an order for OBUs.

We want to show why this happens by giving a couple of examples of what contracts and customer relationships can look like for OBUs.

Exhibit 1:

Exhibit 2:

Exhibit 1 shows a framework contract with deliveries planned over a period of two years. Exhibit 2 shows a large order from an existing customer, with deliveries scheduled for just five months. From these contracts, it is clear that much of the revenue from OBUs is relies on a few large customers. The customer in example 2 accounted for at least NOK 150 million of OBU revenue in 2023 and approximately NOK 70 million of revenue in 2022 (totaling NOK220mln), i.e. more than half of the segment revenue (NOK432mln) in the two-year period.

With today's customer concentration and the lack of concrete information about who the customers are and what they do, it is an impossible task to assess the long-term revenue potential from these customers. This is not positive from a valuation perspective, but something investors must live with. This dynamic makes it difficult to set a particularly high multiple on earnings from OBUs.

However, we do not necessarily have to demand very low multiples. The transition from competitive bidding to long-term B2B partnerships significantly increases switching costs and contributes to greater certainty of future revenues from existing customers using OBUs. Furthermore, potential new customers may consider these long-term and sizeable contracts as an indicator of NORBIT’s ability to deliver on partnership production. This should increase the chances of expanding the customer base and reduces the vulnerability of losing individual customers in the future. We also see an increase in customized product deliveries from NORBIT to their clients. This indicates that NORBIT has gained a notable reputation which organically drives customers to them to make new tailormade products for their concrete needs. This further drives customer retention and integration into their partners value chains.

Drivers behind the introduction of tolls

We want to give a short discussion on the drivers of further integration and expansion of road tolling. The far the most important driver is public spending. In Europe it is increasing and governments are facing significant financial challenges due to rising costs associated with, for example, ageing populations and swelling public organizations. This is forcing governments to look for opportunities to increase public revenues. Taxing the transportation sector by expanding toll collection systems is a natural response. When done right it is also a fee structure that can get support from the public, as long as the tolling isn’t excessive for individuals but more focused on i.e. transportation of goods.

Another driver is electric cars. As more countries, including Norway, promote the electrification of their vehicle fleets, governments face the challenge of compensating for the loss of revenue that this transition will entail. It seems to me that governments generally prefer to replace lost revenue, rather than cut their own costs. One of the most relevant solutions in this context is the introduction or expansion of toll collection.

Toll collection can be seen as a natural replacement for the fuel tax, as it is easy to argue that motorists, including those with electric cars, should pay for the use of the roads they use. A common argument is that if you don't want to pay tolls, you can switch to other forms of transport, such as public transport and cycling.

Looking at the largest economies in the EU, Germany, France and Italy, fuel taxes account for significant revenues. In these countries, €37 billion, €30.5 billion and €20 billion respectively are collected annually through fuel taxes. This shows how important such taxes have been for government revenues.

Although opinions are divided on how the time frame of the transition to electric cars, (especially in other European countries compared to Norway) the major economies in the EU have set ambitious targets for electrification. There are also plans to invest billions of taxpayers' money in the development of charging infrastructure for electric vehicles. This investment is necessary to support the transition to a more environmentally friendly vehicle fleet, but it also reinforces the need to find new sources of revenue to replace the lost revenue from fuel taxes.

This shift requires governments to strike a balance between maintaining necessary revenues and promoting environmentally friendly transportation options, while ensuring that the transition process is fair for everyone involved.

GNSS

Satellite-based toll collection

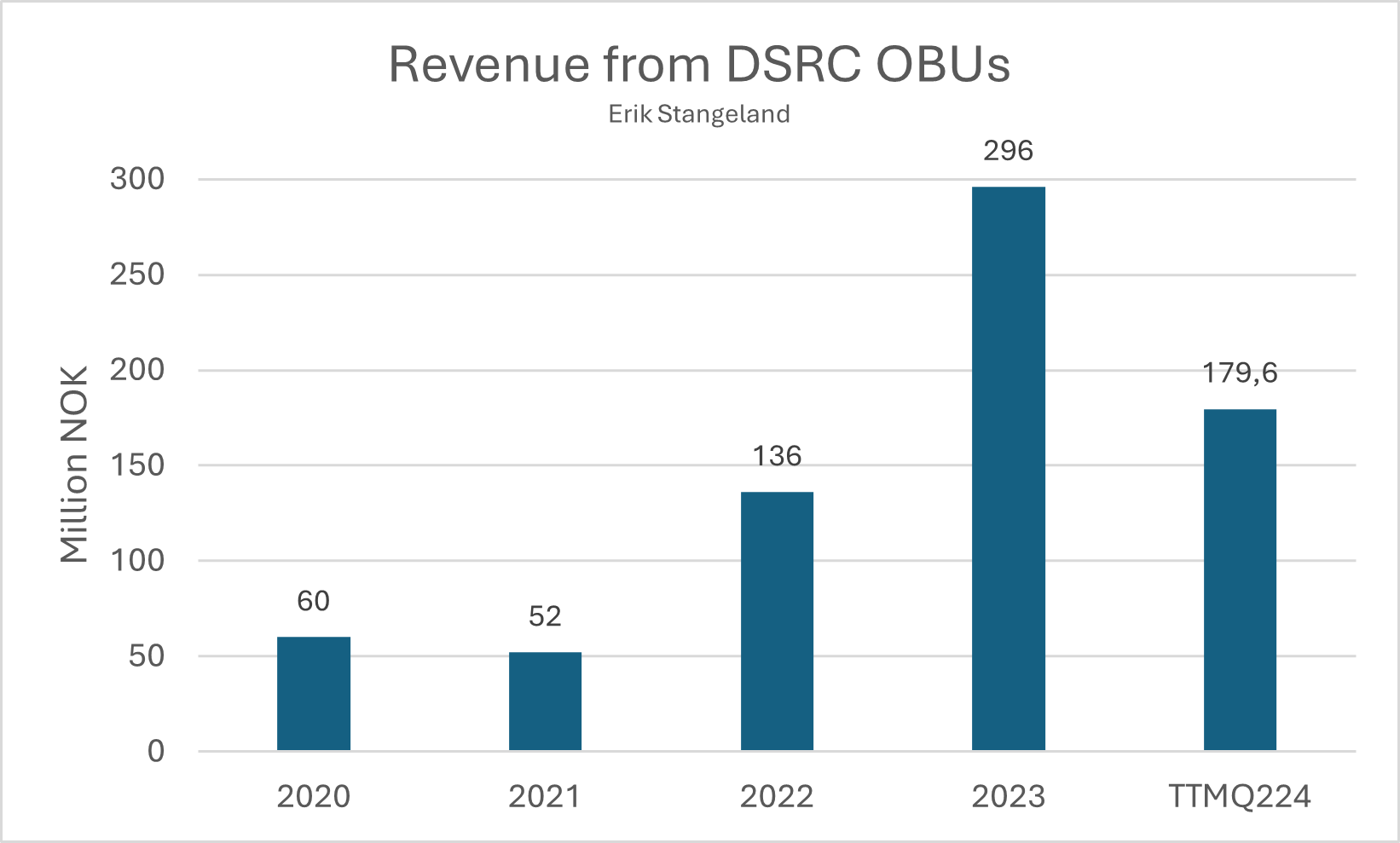

Satellite-based tolling is another solution for toll collection, also known as GNSS tolling. The toll collection system discussed so far is based on paying on passing certain physical points. This is a way of charging for road use that is not particularly accurate, and encourages drivers to try to navigate around tolling points where possible. By using location data, distance-based tolling is made possible. This solution uses satellite navigation technology to identify where the vehicle is, and where it has been, which is then used to calculate what the vehicle should pay for road use on a distance metric and not a check-point metric. NORBIT has developed products for this particular tolling method as well, mostly aimed at commercial freight transportation.

We can observe that sales from this technological solution have developed well in recent years:

Toll collection using the GNSS-technology requires less investment in infrastructure than the system using DSRC. For the same reason, it is also easier to scale up and expand coverage. These advantages are leading some countries to move away from DSRC and towards GNSS. There are also arguments to be made that this is a fairer and more precise way of charging for road use.

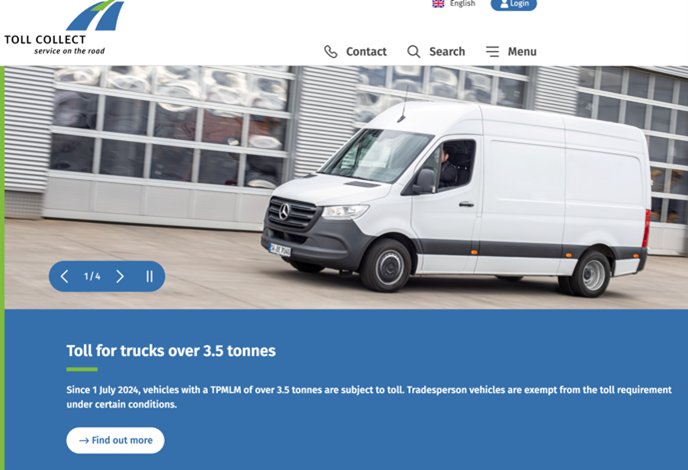

Supplier to German Toll Collect

German Toll Collect is a key customer for NORBIT in this product category. Toll Collect operates one of the world's largest toll systems, with primary responsibility for collecting fees from heavy vehicles engaged in freight transportation. The money they collect goes directly to the German treasury and is earmarked for improving road infrastructure. In addition, the same toll tag can also be used in Austria, making the system practical for international transportation.

NORBIT entered into a framework agreement with Toll Collect in the spring of 2019. At that time, vehicles with a gross vehicle weight (GVW) of more than 7.5 tons were required through regulation to have equipment for distance-based tolling installed. Since the signing of the agreement, this weight requirement has been gradually reduced to GVW over 3.5 tons. This, of course, increases the number of vehicles to which the requirement applies. As of 01.07.2024, the requirements for which vehicles are included were expanded again. The determining factor was changed to TPMLM (technically permissible maximum laden mass), which is the maximum total weight a vehicle is technically approved to carry. Extending the requirements leads to increased volume for NORBIT ITS, which supplies the equipment. In both 2022 and 2023, they were awarded contracts from Toll Collect worth NOK 30 million.

Advantages and disadvantages of GNSS

There are several advantages to satellite-based tolling, compared to automatic sign recognition and toll tags. It provides the fairest charging for road users, as the amount of wear and tear you cause is calculated based on actual use. The road wear and tear is mainly calculated based on weight class and mileage. GNSS is also less demanding for costly infrastructure to survey passing of various checking points roads. In addition, if an emergency were to happen, tracking the exact location of the vehicle can provide faster help.

However, the real-time monitoring that satellite-based tolling entails is the biggest source of criticism for the solution. Privacy is a bigger concern when using satellite-based tolling than DSRC toll tags and license plate recognition. The same feature that gives satellite-based tolling an advantage in the event of an accident is the biggest drawback when trying to gain support for the solution.

This excerpt from a satellite road pricing feasibility study conducted in New Zealand explains the problem well:

"Early implementations of congestion pricing identified some sensitivity to privacy as an issue, with both Singapore and London conscious of the need to protect individual privacy. Privacy is much more likely to be a concern for proposals for GNSS based systems than others because of the need to collect vast amounts of vehicle location data including information for travel which is not subject to charging. Privacy issues tend to get raised by opponents along with other issues as a reason to fear road pricing, primarily out of concern that the government or companies will record all vehicle movements and potentially misuse this data. Privacy concerns ultimately led to the abandonment of many such schemes internationally.

Although privacy protections can potentially be designed into a GNSS based system, misperceptions and lack of proof about how the technology works can mean that a narrative about "spy in the sky" or "tracking the public" can quickly gain credence, raising concerns that the scheme is a Trojan horse for mass scale government surveillance. GNSS is often related with invasive government "tracking" and the data could be applied for other traffic enforcement purposes or wider law enforcement purposes. In addition, there are likely to be concerns that such data could be sold for commercial use. By contrast, the public perceives ANPR as less intrusive than GNSS.

Building privacy into the technology is possible but technically difficult due to the opportunity for malicious parties to affect the distributed system in so many ways. Even more difficult is the task of proving that the system is technically secure and data stored is private."

Source, Transport New Zealand.

Hybrid OBU: both DSRC and GNSS

However, concerns about privacy are not shared by the heavy transportation industry. This is visible through the success of the business model of NORBIT's subsidiary iData, which I cover in the Smart Data section of the article.

In April, NORBIT announced a development contract for a new product with a new blue-chip client, worth NOK 160 million, with planned delivery in 2025. On July 29, more information was released about the contract and the product.

The customer was German Toll4Europe, which works to simplify toll collection for heavy vehicles. Their goal is to offer an OBU that is valid and covers the whole of Europe. As of today, their solution is available in 14 European countries, including Germany, France, Spain, Portugal, Austria, Italy and Poland. They plan to extend coverage throughout 2024. Toll4Europe works with toll companies in different regions and collects all toll payments for its customers in one single invoice, simplifying administration for carriers.

This is a toll payment system that the EU has been working towards for 20 years. The toll reform in Norway in 2015 can be seen as a nano-version of the project the EU started working on in 2004. The aim was to streamline a Union-spanning system, which consisted of 300 different toll companies with widely varying practices and regulations. A few years later, in 2009, EETS, which stands for European Electronic Toll Service, was introduced. The EETS directive was created to simplify payment systems for road use through interoperability across national borders in Europe.

To achieve interoperability, the permitted technological solutions were limited to DSRC, which constitutes short-range communication, and GNSS, which constitutes long-range communication. To be able to drive throughout Europe with one OBU, this must be a hybrid that has both GNSS and DSRC technology. This is what NORBIT will now develop and deliver to Toll4Europe.

Hybrid OBUs have been on the market for a long time, and NORBIT has actually been a supplier of DSRC modules for this type of product for around 10 years. The contract is a result of Toll4Europe approaching NORBIT and asking them to develop a new hybrid OBU with increased usability, new functions and new features. The fact that such a large and serious actor makes the first move, speaks volumes to the strength of NORBIT's reputation in the industry.

With this contract, NORBIT is moving up the value chain, from supplying components to delivering finished products. During the presentation of the Q2’2024 figures, CEO Per Jørgen Weisethaunet said that if they had only delivered DSRC modules for this contract, it would have been a contract in the order of 10 - 15MNOK, instead of 160MNOK. He also gave the impression that this is a product with revenue potential not only for this specific contract and mentioned that NORBIT has delivered two million DSRC modules to this type of hybrid OBU since 2019. We don't know the exact volume involved in this contract, but given the 10X+ step-up in revenue, it's probably reasonable to assume that it's far lower than two million, indicating a potential for additional contracts in the future.

It may not be many years before these contracts materialize. Per Jørgen appeared on the Norwegian brokerage firm Arctic Securities' podcast "ArcticPodden" on the 16th of August this year (2024), where he pointed out that a significant portion of the installed base of Hybrid-OBUs will need to be replaced due to the phasing out of 2G technology in the units. Several of the largest countries in Europe plan to shut down 2G within the next few years.[15]

I mentioned earlier in the article that NORBIT used to hand over responsibility for the production and sale of its products to other companies. The fact that they are now being contacted by major players with requests to deliver complete solutions (box-build) for products for which they previously only supplied components is a clear sign of their impressive development, or as we can call it a class journey, in the industry over the past twenty years. This class journey has given NORBIT a stronger position in the market, where they now have significantly greater and ever-increasing leverage. They have gone from a small but efficient player, to a highly integrated operator delivering fully customized and tailormade technology. This is bound to give NORBIT scale advantage, but also a valuable integration into customers value chains.

This contract clearly illustrates that the development of NORBIT Connectivity is still going strong, and that the company continues to lay brick by brick at a controlled pace. In the past, NORBIT’s ambition has been to be a niche leader, but during the presentation of its new medium-term goals, it announced a shift from being "niche" to becoming "notable." This marks a strategic transition towards greater visibility and the execution of larger operations. In the future, NORBIT could move further up the value chain for the product I will discuss in the next part of the article.

Wireless communication device for smart tachographs

Innovation driven by regulation

Hybrid OBUs are not the only products where NORBIT supplies DSRC modules. Another ITS product that NORBIT has had great success with in the recent years is its tachograph enforcement module. This is a DSRC module that works as a component in smart/digital tachographs. The main purpose of these tachographs is to enforce road safety regulations by monitoring and ensuring that drivers do not exceed permitted driving times. In addition, they ensure that working conditions for drivers are in line with current regulations and standards. As all transport vehicles are required to use these tachographs, they also help to enable and ensure fair competition among transport companies.

The component, which NORBIT supplies, enables wireless reading of data from tachographs. This can be done with e.g. equipment that is permanently mounted along road sections, or they can be in mobile devices. This means time and resource savings for road authorities and the police, who now receive data about driving and rest time compliance without having to stop the vehicles. This means that authorities can use their resources more efficiently, and only target vehicles not following the relevant regulations in their respective zones.

This product is an answer to a need created by a new EU regulation, where all tachographs had to be wirelessly readable. A digital tachograph had to be installed by June 15, 2019, in all vehicles with a weight of more than 3.5 tons, transporting goods, or with more than nine seats.

Start of customer relationship with Continental in 2019

NORBIT entered into framework agreements with two suppliers of tachograph-monitoring. These were Continental and Intellic. Of these two, it is Continental that is most significant and important to know about. At the time, Continental had about 70% of the tachograph market, which meant large volumes for NORBIT. In the reporting year, the continental deal gave a huge boost to the ITS results of NORBIT.

Apart from the large volume from the number of digital tachographs going from zero to numerous right after the regulation, there is also a need for all new vehicles to be equipped. This creates positive demand-dynamics for NORBIT going forward. Approximately 350,000-400,000 new vehicles corresponding to the regulations that need a tachograph are registered. This means a solid annual volume, which provides good visibility for earnings from NORBIT’s tachographs.

There are few other players in the market. The most notable are Stoneridge and Intellic. Intellic also uses the DSRC module from NORBIT. Link to overview of approved tachographs over the past 20 years: https://dtc.jrc.ec.europa.eu/dtc_vehicle_units_status.php.html

Framework agreement with Continental in 2023

Since the regulation on digital tachographs in 2019, there have been two iterations of "Smart tachographs" as well as extended requirements from authorities. The requirements mean that:

All vehicles with the first version of digital tachographs must replace these with the latest smart tachograph by 31.12.2024.

All vehicles with the first version of the smart tachograph will be replaced with the latest smart tachograph by August 2025.

Heavy-duty vans, vans with a GVW of more than 2.5 tons, which are used to transport goods across national borders. Gross vehicle weight is the total weight of the vehicle when fully loaded. These must be equipped by July 2026.

These requirements for retrofitting the latest version of the tachograph have naturally led to increased demand for tachographs from Continental, which leads to more orders for NORBIT. In addition to retrofitting, there will be newly bought and registered vehicles to be equipped every year. In May 2023, a new framework agreement with a record-breaking value of more than NOK 500 million between Continental and NORBIT was announced. The contract provides good visibility for revenues from the product over the next few years.

Continental is still the major market leader for smart tachographs in the European market. During the presentation of the figures for the full year 2023, CEO Weisethaunet commented that Continental currently has around 80% market share. In addition, it was mentioned that a new production line for DSRC modules is planned in the CAPEX program for 2024 consolidating NORBIT’s ability to deliver on orders further.

Revenue from the product has developed well and received a good boost in 2023 and has continued strongly in 2024. In addition, the product was mentioned as a growth driver in the outlook for Q3’24.

An interesting value proposition available to NORBIT through the Tachograph-market is to move up the value chain, as NORBIT did with the contract with Toll4Europe for hybrid OBU.

The market for smart tachographs

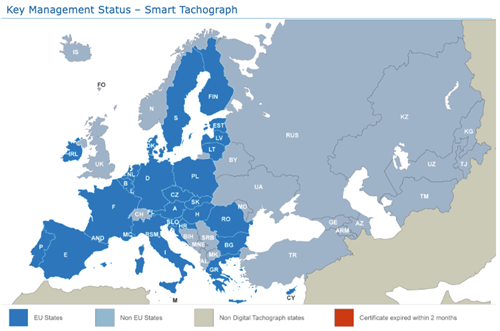

The image below shows which countries are included in the European Commission's security standards and protocols for smart tachographs. What stands out here is how many non-EU states are included, such as Turkey and Russia. "EU States" and "Non EU States" represent the Continentals market for tachographs.

The next image shows an illustration of the interoperable system that these countries are part of. The system enables seamless control of vehicles across national borders for all three parties involved.

The features of smart tachographs

The latest version of the smart tachograph has expanded functionality with far better usability. Although the equipment is mandatory, it is my understanding that drivers and fleet owners welcome this technology. It can be used to register different cabotage activities and not just driving and resting times. The picture shows additional features on the latest generation of digital tacographs from Continental.

Other

Desktop reader (DTR) allows you to read information on a tolling tag manually. It can be used to verify the status of the tag's function. In markets where payment tags need to be recharged with money, just like a cash card for mobile phones, this system is used. DTRs can also be used to change affiliation information on the tag. DTR is compatible with several variants of payment tags.

Roadside units (RSU) are antennas that recognizes toll tags. These can be mounted along the road, in a drive-thru or parking garage or where-ever it is needed.

Competitive landscape

Kapsch, Q-Free and MOVYON are relevant competitors in the European market. Unlike NORBIT, they all supply heavy traffic systems, in addition to toll tags. When we talk about heavy traffic systems, this largely applies to multi-lane free-flow (MLFF) systems. These are modern toll booths and enable passing without the need to stop, or to brake at all.

These systems are fitted with equipment for identifying vehicles. In the EU, sensors for registration of toll tags are most common. In addition, equipment for license plate/registration number recognition (ALPR) is also installed, in order to be able to collect from vehicles without a toll tag, or with a defective toll tag. The toll tag is the link between the vehicles and the toll stations.

Since the toll tag is only a link, this means that revenues from MLFF systems are far greater than those from tolling tags. In Europe, Kapsch gets an average of 12% of its total revenue from its tolling tag segment (Components) over the past four years.[1] This fact probably played a role when Q-Free didn’t fight with tooth and nail to defend against NORBIT in the Norwegian toll tag market 15 years ago. This is an advantage for NORBIT, which focuses on toll tag development and production, rather than heavy traffic systems as their product constitutes a proportionally small part of the total revenues for many of these tolling tech companies.

In addition, I have mentioned the shift from public tender competitions to private players being tolling tag issuers and "technology partners" with the tolling tag manufacturers. The buyers of heavy traffic systems are public actors and road builders. This difference in customers creates competitive dynamics in advantage of NORBIT’s ITS-segment. As direct competitors are providers of heavy traffic systems, the competitive field surrounding NORBIT will not be able to shift their focus in the same way, and will continue to have public sector operators and road builders as their most important customers.

Run-down of NORBIT’s direct competitors

Q-Free

Like many of Norway's technology companies, Q-Free has its origins in Trøndelag. Until last fall, the company was listed on the Oslo Stock Exchange but was taken private following a bid from a joint venture between the then largest owner, Norwegian Rieber & Søn, and Canadian Guardian Smart Infrastructure Management. The acquisition price was approximately NOK 1.3 billion.

Q-Free has two business segments, Tolling and traffic management. They offer DSRC tags and readers, solutions based on automatic license plate recognition (ALPR) and image analysis, as well as other electronic toll collection systems, such as multi-lane free-flow, truck tolling and congestion pricing. They have over 35 years of experience with DSRC technology and have delivered over 40 million toll tags.

In 2022, they had 621MNOK in revenue from the tolling segment.

Kapsch

Kapsch is an Austrian listed company and the largest ITS player in the world. They operate with two business segments, Tolling and Traffic Management. They have executed projects in over 50 countries globally and have offices in over 25 countries. In the last full financial year, Kapsch had a turnover of EUR 539 million. In 2004, they delivered the first country-wide MLFF system in the world.

The Tolling segment is divided into three: Implementation, Operations and Components. Under Components, Kapsch delivers in-vehicle components (toll tags) and road-side components, such as RSUs, cameras and sensors.

In the last financial year (April 1 - March 31), they had revenues of 36.2MEUR from Components, corresponding to 425MNOK as of 03.09.24. In comparison, NORBIT had just under 450MNOK in revenue from ITS in 2023. NORBIT is no longer a small time player, but a significant actor in the European Components market.

Commentary on the European market from Kapsch 2023/24 group report

Road telematics solutions correspond to intelligent traffic systems. Kapsch sees continued positive development in the European market.

MOVYON

MOVYON is an Italian company specialized in Intelligent Transport Systems (ITS), focusing on the development and implementation of technological solutions for transport infrastructure. The company is part of the Autostrade per I'Italia Group, one of the largest players in highway operation and maintenance in Italy.

Their technology is used on 75% of the highways in Italy and they have delivered over 10 million on-board units across Europe. They offer both DSRC OBU, and hybrid OBU, similar to the product NORBIT will deliver to Toll4Europe. In addition, MOVYON also supplies MLFF and ALPR.

Summary of ITS

Now we want to give a summary of the segment and how it looks currently. It's approaching twenty years since NORBIT entered the Norwegian toll tag market. Since then, they have laid brick by brick. Today, ITS stands on several legs and has a strong market position in several attractive product segments. They have long-term relationships with strong players in good and profitable markets. In addition, they continue to show that through the development of new products, they can continue to improve their opportunities for further growth from ITS.

NORBIT is a subcontractor to Europe's largest supplier of tachographs. With the current state of European regulations, the demand for tachographs is expected to remain strong in the years ahead. NORBIT has a customer dependency, and need to make sure that Continental remains satisfied. In addition, the company has a strong market position in the two technological solutions for toll collection permitted in the EU, DSRC and GNSS technology.

The demand for these is largely supported by governments, which want to maintain or increase state revenues. Some would claim that ITS is supported by a strengthening of the governmental trend of more regulations and taxation in the EU. However, we also see that some of this technology is independently wanted by transportation companies looking to effectively manage their fleets with live-time data provided by NORBIT’s technology.

There will be a need for efficient transportation and funding for this, for longer than most people's investment horizon. When you value ITS, you have to assess whether you think the NORBIT team of Per Jørgen Weisethaunet, Erik Ryan and Asbjørn Dahl will be able to help drive development and gain market share where it counts in the future. With a strong track record to show for, we believe there is good evidence to support that they will continue to be good operators within this niche and continue earning revenue from this secular transportation trend.

A continuation of the financial analysis of ITS is provided in the "Concluding financial analysis".

Smart Data - iData

iData overview

Smart Data consists of the software and service provider iData. NORBIT acquired the Hungarian company iData in 2021, thereby gaining a foothold in a new market segment. At the time of the acquisition, iData had a market-leading position in Hungary in vehicle tracking and fleet management services. Through the acquisition, NORBIT has gained exposure to a different type of business model, namely subscription and software-as-a-service. Through its marketing capabilities, NORBIT would help iData expand its market footprint in Europe.

Acquisition snapshot of iData, year prior to NORBIT buying them.

Idata 2020

Turnover: €5mln

EBITDA: ~€1.9mln

EBITDA margin: ~38%

Interest-bearing liabilities: 0

Acq. Enterprise value: €14.5mln

Acq. Multiple paid, EV/EBITDA: 7.6

When NORBIT completed the acquisition on 30.07.21, the exchange rate stood at ~NOK/EUR 10.4, which means an acquisition price of approximately NOK 150 million. Of this NOK25 million was paid with ~1.2 million shares with a price per share of NOK 20.65.

The founders, or sellers of the company, still make up the top management of iData today, pointing to NORBIT allowing the team to continue operating as it has been and underlines their focus on decentralization which is common in many other successful companies engaged in M&A.

iDatas core product is their proprietary iTrack GPS tracking system, which provides online live-time tracking of vehicles. A typical customer is a cost-concious company with a small fleet of vehicles, who wants a full overview of their vehicles. With the GPS tracking system, they can track their vehicles online, check their routes, see a log of the driver's work, get accurate information about fuel consumption and make toll payments easy.

NORBIT develops and sells products in the ITS segment that enable, for example, tracking and, of course, toll payment. Through iData, they gain direct insight into what their customers need and want, which helps them to make good decisions related to further product development.

GPS tracking services have become a standard practice in the transportation industry due to several positive effects. The service can be considered from three perspectives: fleet manager, drivers and customers.

Monitoring of the vehicle fleet:

Route-overview: The administrator gets insight into the routes the vehicles follow, both planned and ongoing.

Driving time analysis: The service records the driving time, distance and fuel consumption, which helps to calculate costs for future assignments and potential for improvements.

Cost overview: Other costs, such as tolls, are also documented.

Efficient fleet management:

Real-time information: Location information from the vehicles allows the fleet manager to optimize the use of the vehicles.

Easy planning: The service simplifies fleet management and makes planning more efficient.

Improved predictability for all parties:

Planning: The administrator gets a better overview and can plan more precisely.

Predictability for drivers: More planning gives drivers a better overview of their tasks and deadlines.

Customer information: Customers can get accurate information about delivery times and easily request updates.

To put it very simply, the service generates data, which is valuable for both administration, drivers' working conditions and the customer experience.

Valuation of Smart Data

It has been a few years since the acquisition of iData, and I would like to attempt an updated valuation of the company. Apart from revenue, information about iData is very limited. Fortunately, there is a listed company in Sweden that in many ways is very similar to iData. The company is called Opter AB and is listed on Nasdaq First North.

Opter AB (Opter) is a software company that offers transport management systems. This is an umbrella term for systems that handle practical tasks related to the planning, implementation and follow-up of transport and logistics services.

Over 85% of Opter's revenue is subscriber-based recurring revenue. This is in line with iData, which received over 85% of its revenue from recurring revenues in 2021.

In addition to business model, they are also very similar in size and growth. Since 2019, Smart Data has grown its revenue in Norwegian kroner from 53 to 101 million, giving a CAGR of 15.4%. Opter, on the other hand, has grown its revenue in Swedish kronor from SEK 43 million to SEK 84 million, giving a CAGR of 16.1%.

In regards of the profitability of iData, we only know the EBITDA margin in 2020 and 2021. It varied greatly in these two years, and it is worth remembering that 2021 was the year when the acquisition was completed. Opter's margin took a hit during the COVID-19 pandemic but has since risen nicely along with sales. Considering NORBIT’s strong history when it comes to margins, we believe it is fair to assume that Smart Data's margin has also risen along with sales since 2021.

Regarding EBITDA vs EBIT, I would like to mention that Opter has approximately SEK 0 in assets, which means that their EBITDA ≈ EBIT.

Opter released a strong second quarter report on August 30, 2024, and the share closed at SEK 106.5. With 6,000,000 shares outstanding and no interest-bearing debt, this gives an enterprise value of SEK 639 million. Based on earnings over the past four quarters, this gives an EV/EBIT multiple of just over 30.

If you plot Smart Data's margin and EV/EBIT multiple equal to Opter's, it gives a company value of a hefty 760MNOK. Personally, I think that's a high multiple, and it's not something I would invest in.

The sensitivity analysis below shows that the iData investment has most likely met or exceeded expectations. The internal rate of return in the most conservative scenario is ~25%. The scenario in bold corresponds to Opter's EBIT margin and NORBIT’s ~EV/EBIT multiple for 2024, per 30.08.2024. Given iData's favorable growth and margin profile, it is probably safe to assume a somewhat higher multiple is appropriate. I therefore prefer the scenario in green.

Concluding financial analysis of NORBIT Connectivity

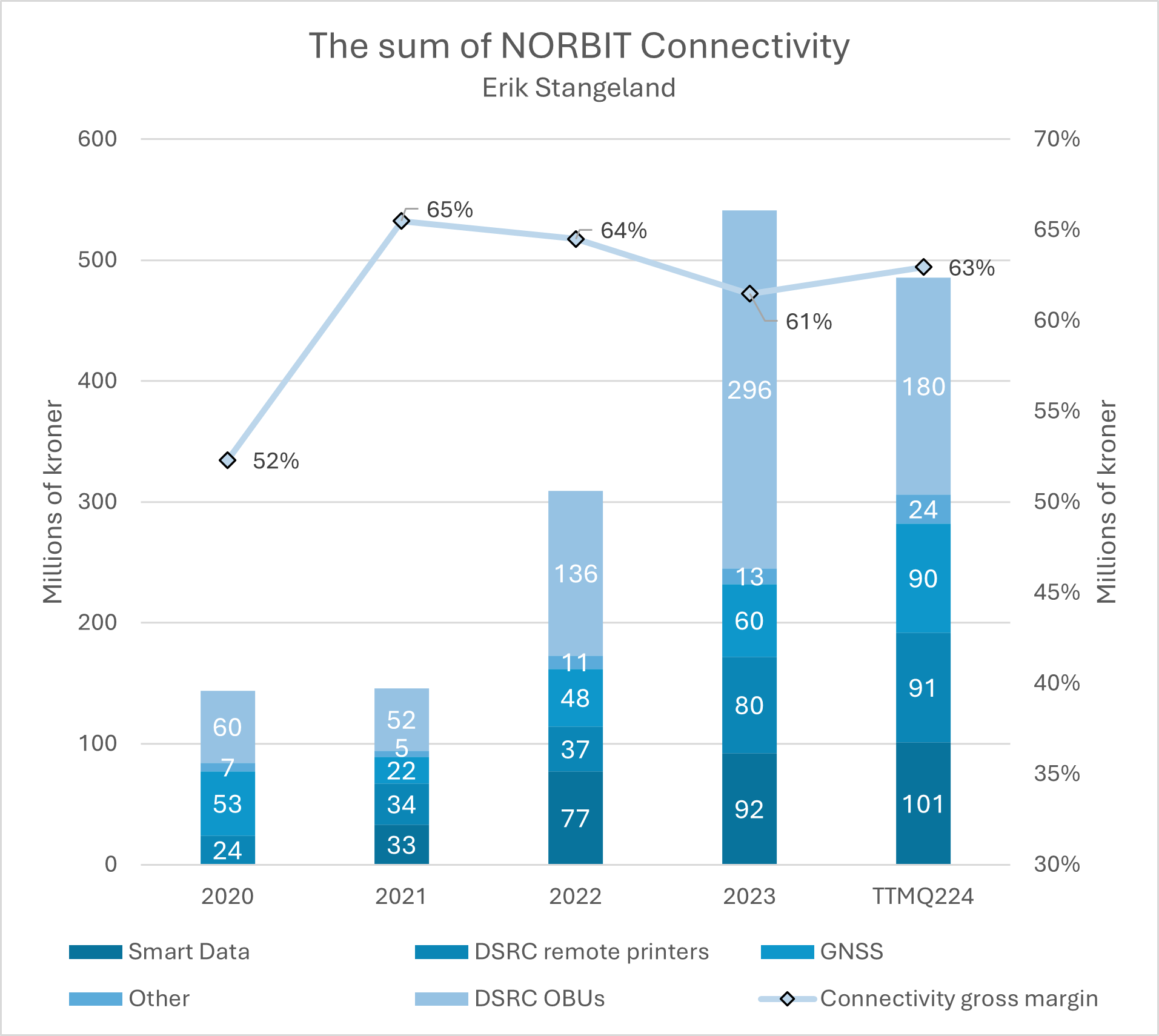

From the below chart, you can see that Connectivity's growth in recent years has been diversified, with contributions from across their entire product portfolio. It can also be observed that they have managed to hold on to their margins, even though their customers have committed to large volumes which typically gives the ordering party more say over pricing. Margins are lifted by Smart Data, which is reasonable to assume have significantly higher gross margin than ITS. However, ITS had 62% and 65% margins in 2018 and 2019 respectively, which suggests that the weak gross margin in 2020 was mainly a result of the pandemic.

The strong gross margin is another good indicator of how strong NORBIT’s market position is within their Connectivity segment. They are not only a respected player in the Norwegian market, but throughout Europe. While writing this article, my perception of the quality of the Connectivity business has become increasingly positive. NORBIT Connectivity has built a strong brand in Europe.

If we look further down in the accounts at operating costs, we see that there are no signs of costs swelling. Since the start of 2023, Connectivity has secured contracts worth over NOK 1 billion. So far, these larger operations have not affected operating costs. Weisethaunet seems to have the attitude that "if it doesn't make money, it doesn't make sense".

Two things I like in companies are high revenue visibility and low customer concentration. In the NORBIT Group, you get both sides of the scale, but in different segments. This means that, overall, NORBIT ends up scoring averagely. Not as good as Kongsberg Gruppen, but better than Nordic Semiconductor.

Concerning valuation, it is always the future that we should put our focus towards. I believe Connectivity has good opportunities to continue to diversify and grow its revenues. Both through a more evenly distributed revenue contribution from the different product areas, as well as a gradually lower customer concentration through hopefully new contracts. My thought is that customer concentration may decrease in the long term as ITS continues to demonstrate its ability to deliver competitive products. And although customer concentration is high, these customer relationships have apparently become stronger in recent years. The combination of this, I believe, makes Connectivity deserving of a respectable multiple.

I would like to remind the reader of the long-term goals for Connectivity by 2027, which will be central to result of this valuation exercise regarding a sum-of-all-parts assessment. There are several strong arguments to be made for having confidence in the management’s guidance. NORBIT has a track record of staying true to their strategy, as we can see they have managed to carefully and controlled have managed to take on larger and more complex projects. A clear sign of their ability to deliver is that they already reached their 2024 target, set in early 2021, a full year ahead of schedule in 2023.

No one is immune to over-optimism or other psychological tendencies we humans are ever so prone to be exposed towards. Therefore, I would like to emphasize that this valuation exercise is intended only as an illustration of what the Connectivity segment may be worth if it were an independent unit, and to show how it’s importance within the NORBIT group. The aim is to give an overview and an idea of the potential of this segment, rather than a precise valuation.

To reach the strategic goal of NOK 1bln revenue in 2027, Connectivity needs to grow its revenue 23% annually from Q2’24 onwards. Some of the risks to this ambition are:

Loss of one or more major customers,

Unfavorable regulatory changes,

Slower implementation of toll collection,

Connectivity fails to capitalize and adapt to market changes,

Significant Norwegian krone appreciation

I will offer a low threshold and somewhat creative valuation of Connectivity, basing it on 2027 guiding. Earlier I have suggested a possible value for Smart Data, so that leaves ITS. I extract Smart Data by assuming that the segment continues its historical revenue CAGR of 15.4% and has a 30% EBIT margin in 2027. We then end up with NOK 167 million in revenue and NOK 50 million in EBIT. I would say that these are optimistic estimates for Smart Data, which gives some margin of safety to ITS.

I subtract Smart Data's estimated contribution to Connectivity's revenue of NOK 1 billion in 2027. With my assumptions, ITS will account for NOK 833 million of revenue and NOK 225 million of EBIT. ITS had sales of NOK 385 million in the last four quarters and thus needs a CAGR for sales up to and including 2027 of 24.7%.

I would value ITS using the EV/EBIT multiple, as I did with Smart Data. They reported NIBD of 184MNOK in the Q224 report. Since the end of Q2, NORBIT has taken on new debt in connection with the acquisition of Innomar of ~450MNOK. In addition, they raised 200MNOK through a share issue, to ensure sufficient financial flexibility. With these events included, I end up with an updated NIBD of 434MNOK for NORBIT as a whole.

Since NORBIT is currently priced with Innomar included on the public listing, I will add their TTM EBIT to NORBIT’s. This makes it easier to see the value I find for Connectivity in perspective. In the investor presentation from the acquisition, NORBIT stated that Innomar had had an EBIT in Norwegian kroner of 76 million. I add this to NORBIT’s EBIT from the last four quarters. This increases NORBIT’s EBIT by over 30% to ~324MNOK. This is clearly a major acquisition for NORBIT, which will be very exciting to follow in the period ahead.

he EBIT that I found for NORBIT + Innomar above can be compared to EBIT from Connectivity over the last four quarters. The Connectivity segment has accounted for ~34% of EBIT in the last four quarters. Let’s assume pretend that this is also Connectivity's share of NORBIT‘s NIBD, and add this to the equity value, to find the enterprise value. Since I assumed zero debt for Smart Data, ITS gets all the debt. 34% of NIBD of 434 gives Connectivity a debt of just under 150MNOK.

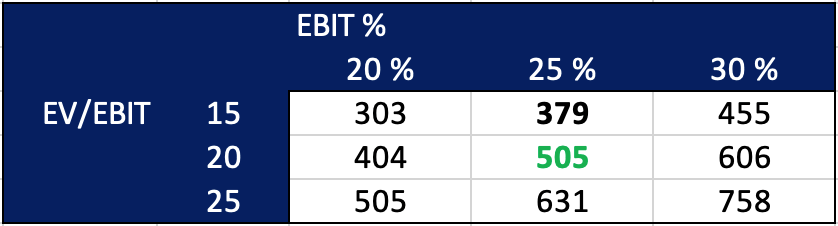

In the end, we end up with a sensitivity matrix that looks like this for ITS:

In the scenario marked in green, I have assumed an EV/EBIT multiple for ITS in 2027 of 12, and a discount rate of 14%. In this scenario, you can pay up to NOK 1.674 billion for ITS, get a 14% annual return, and end up with an EV/EBIT multiple of 12 for earnings in 2027.

A curious question is whether an EV/EBIT multiple of 12 is the right one in 2027, if ITS achieves its targets. It is not inconceivable that they will have a lower customer concentration and an even broader product portfolio at that time. In that case, this would in my opinion be a basis for arguing for a higher multiple for the segment. In any case, the most important thing will probably be what growth you see for the segment in the future. The total addressable market is large, the question is just how big a role NORBIT ITS will play.

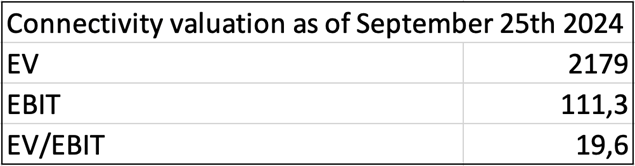

The sum of the figures marked in green from Smart Data and ITS's sensitivity analyses is just under NOK 2.2 billion.

This value corresponds to an EV/EBIT multiple of 19.6 today. When you base a valuation on high future growth, you end up justifying high multiples today.

This is comparable to the current EV, which has reached over NOK 6 billion. This means that NORBIT is starting to reach a size that makes the company more attractive to larger funds and other players. The EV/EBIT multiple, with Innomar included, is 18.7. Although this multiple is of course considerably lower looking forward, NORBIT is no longer considered particularly cheap. Given the company's history and other positive factors, it should not be valued cheaply either.

The opportunities for multiple expansion in the NORBIT share are smaller today than they were two years ago, that is indisputable. This means that returns in the coming years will be largely dependent on increased earnings, which in turn depend on Per Jørgen Weisethaunet and his team continuing to make the right decisions and continuing to navigate their markets successfully.

In the scenario where Connectivity is worth NOK ~2.2 billion today, this represents ~36% of the current company value. I do not believe that the entirety of this value is reflected in the current market price. However, a more accurate pricing of Connectivity will not have a major impact on the groups collective multiple but rather continue to contribute to a good return in the share price appreciation. To see a major impact, a combination of higher multiples and lower required rates of return must be applied than I have done in my calculations. I believe that such an adjustment can only be considered if we see concrete developments in 2025 and 2026, i.e. that NORBIT acquires contracts and/or favorable regulation is decided, which indicate that these goals are increasingly likely to be achieved. Let’s wait and see.

The table below demonstrates how any higher multiples and lower required rates of return affect the value of ITS.

The investment returns from NORBIT can come from several business segments. When you buy NORBIT you buy the whole package, consisting of Connectivity, Oceans and PIR. The collected package is better than the sum of the parts. At the same time, it's an interesting exercise to calculate what it would look like if they were to be separated. If we subtract my theoretical value for Connectivity, we end up with a residual value of just under NOK 3.9 billion.

Most of this value is accounted for by the Oceans segment, which specializes in delivering technology for underwater use. The segment derives its revenue from a highly regarded proprietary product portfolio. The cornerstone and main revenue contributor is their portfolio of multibeam echo sounders (MBES), which has a wide range of use cases. Their MBES are typically mounted on smaller survey vessels and unmanned vessels such as AUVs and USVs.

In addition, NORBIT is also actively working on expanding their product portfolio through continued innovation and acquisitions, to capitalize on their strong market footprint and wide customer base. Notable developments in the last few years is:

· The launch of their proprietary GuardPoint product range, aimed at the extraordinarily relevant offshore security segment.

· The acquisition of the side-scan sonar (SSS) producer PING DSP

· The acquisition of Innomar, the global market leader for sub-bottom profilers (SBP)

The Oceans segment has been a huge success for NORBIT. Profitability turned from negative to positive in 2017 and has experienced an incredibly strong growth and profitability in recent years. This has been possible due to a rising gross margin, which today is around 70%, combined with NORBIT’s best in class cost control, and not least steady revenue growth. From Q3’24, Innomar will also be included in Oceans. I have used an EBIT margin estimate of 35% in the calculation of the revenue contribution from Innomar, the same as the Norwegian analyst house SB1M. With Innomar included, Oceans has printed just under NOK 250 million in operating profit over the last four quarters.

NOTE! If you add up the profit from NORBIT’s segments, you will get a higher amount than what is shown in the consolidated financial statements. This is due to eliminations. Group eliminations in an accounting context involve the removal of internal transactions and balances between companies in a group structure, to avoid double counting and provide a clear picture of the group's financial situation as a whole. This occurs during consolidation, when a parent company combines the accounts of its subsidiaries. In the last four quarters, eliminations have reduced operating profit by NOK 57.8 million, corresponding to approximately 20% of the Group's operating profit. I could have estimated Connectivity's earnings after eliminations, but concluded that the conclusion would be the same, and therefore did not. All figures for the entire Group in the article are after eliminations.

The guidance for 2027 in Oceans and PIR is shown in the below graphs. The contribution from Innomar will be added on top of this guidance. There may also be other contributions, small and large, because there is always something exciting cooking in the NORBIT kitchen. I would like to mention two smaller acquisitions that were made in 2023 in the Oceans segment. One is the acquisition of its distribution partner in North America, Seahorse Geomatics ($1.5M), which was made to increase vertical integration and strengthen NORBIT’s sales and distribution chain. With a strong sales and distribution apparatus, NORBIT can help smaller players. A few months later came the acquisition of Canadian PING DSP ($3.2M), which expands Oceans' product portfolio. Stone upon stone.

There is also expectations for strong growth for the PIR segment, which will continue to offer competitive contract manufacturing and benefit from the onshoring trend. For 2024, investments in PPE (property, plant and equipment) of as much as NOK 90-100 million are planned. The investment is a result of NORBIT’s nominal revenue growth skyrocketing in the recent years. The fact that NORBIT engages in competitive contract manufacturing also ensures that the production of its own products is done efficiently and that they see these efficiency results in their internal product processes.

At group level it looks as follow. The ambition is to deliver a 16% CAGR of revenue with an EBIT margin of 20%. In 2023, the EBIT margin was ~19%. Innomar is also at the top of the guidance here. I look forward to following the further development.

With that, I'm happy to conclude. Hopefully, reading this article has given you valuable input on how to think about NORBIT and especially the Connectivity segment, giving you more time to think about Oceans and PIR, and other opportunities.

Thank you for reading the article!

Feel free to get in touch if you have any questions or suggestions for other companies that deserve a deep dive!

The article was researched and written in Norwegian originally by the author Erik Stangeland. You can reach him here:

Mail: erikmls@hotmail.com

X/Twitter: @erik_stangeland

English translation was performed by the author behind the Learning to Grow newsletter. Contact info is as follows:

Mail: ltgsubstack@gmail.com

Twitter: @ikkenospes

If you enjoyed this article, I just want to take a minute of your time to say thank you! There are many ways you can give back: Leave a comment with criticsm or feedback - I really enjoy discussing with other engaged investors and feedback is what helps me grow.

You can also subscribe to my publication, or share it with a friend you think would get some value out of reading it. And if you are especially generous there are ways you can pitch in: Either by buying me a coffee through the button below, or buying a subscription on my favourite investment data platform: Finchat.io. You get a 15% discount, I get a part of the sales - win win baby.

None of this should be understood as investment advice.

Due to formatting being very hard to bring over from Word to Substack, sources are listed not in order. It took too damn much time to format - refer to the PDF for the correct sourcing order.

https://norbit.com/no/norbit-to-acquire-the-maritime-technology-company-innomar/

https://norbit.com/no/norbit-acquires-idata-and-broadens-the-its-business/

https://opter.com/varfor-opter/

https://www.movyon.com/en/all-movyon-solutions

https://www.kapsch.net/en/ir/download-center

https://rieberson.no/

https://gsim.guardiancapital.com/

https://e24.no/boers-og-finans/i/zEjWlK/bud-verdsetter-q-free-til-13-mrd

https://www.q-free.com/wp-content/uploads/reports/annual/2022/Q-Free-Annual-Report-2022.pdf

https://norbit.com/media/PS-110018-4_Norbit_Desktop_Reader_DTR_Datasheet-1.pdf

https://norbit.com/media/PS-100003-11_Norbit_ITS_FZ58058_datasheet-1.pdf

https://transport.ec.europa.eu/transport-modes/road/tachograph_en

https://www.syscom.ch/2g-3g-network-shutdown

https://norbit.com/no/norbit-awarded-frame-agreement-with-toll-collect/

https://norbit.com/no/norbit-receives-nok-30-million-order-from-toll-collect/

https://norbit.com/no/norbit-receives-nok-30-million-order-from-toll-collect-2/

https://www.t-systems.com/in/en/success-stories/digital/toll4europe

https://www.tv2.no/broom/snart-betaler-du-parkering-og-mye-mer-med-bombrikken/11851676/

https://norbit.com/no/norbit-strategic-partnership-with-fremtind-service/

https://www.adressa.no/okonomi/i/aW9XlM/na-skal-norbit-legge-verden-for-sine-fotter

https://www.rfidjournal.com/expert-views/the-history-of-rfid-technology/76202/

https://www.itsstandards.eu/its-application-areas/cen-dsrc/

Toll roads in Norway - Wikipedia

https://www.adressa.no/okonomi/i/7d0onB/brot-monopolet-pa-autopass

https://www.tu.no/artikler/industri-hoyteknologisk-opptur-pa-roros/251934

https://www.tu.no/artikler/industri-norbit-passerer-q-free-i-norge/249101

I find it remarkable how deeply you have delved into the connectivity analysis. Do you really see anything special here? I work in the logistics industry and even from the text I can't recognise any strong ‘power’ that the company has. In addition, there is the customer concentration and the fact that we are only talking about a sub-segment of sales for Connectivity. I am invested in Norbit myself, but have a small observation position. I am really puzzled as to why you at Norbit have delved so deeply into one sub-segment. There are competitors, there is always technological change and the company is also heavily affected by regulations and laws.