Evolution AB

The market has lost faith in one of the best performers. What is behind this multiple compression, and what can we expect going forward?

Evolution AB is a world-leading provider and developer of online and live casino games based in Sweden. It's a fantastic company when you look at the fundamentals.

This is not a deep dive into the company's business model, history and operational skills. There are far too many people who have written long and good deep dives into Evolution. That's why I'm attaching links that present and elaborate on the company better than I could myself at the bottom of this article.

After the Q1 report, the share price has fallen by around 11%, and over the past three years the share price has gone in the opposite direction to the fundamental development of the company and the return over three years is negative ~25%.

Has the company deteriorated over the past three years? Why does the stock market believe that the company should be priced lower this year than in the summer of 2021? I can't get the share price to match with the fundamental development of the company:

My opinion is that the company has become significantly stronger over the past three years. Why the market value of the company has not been rewarded I suspect can be explained by mainly four reasons:

Less institutional ownership

The Evil Incorporated discount

Consolidation phase

The joker Vladimir Putin

Let me now go into more depth on these four factors:

Less institutional ownership. This has led to greater sell-offs, fewer large players trading on price declines that do not correspond to fundamental developments and poorerprice discovery.

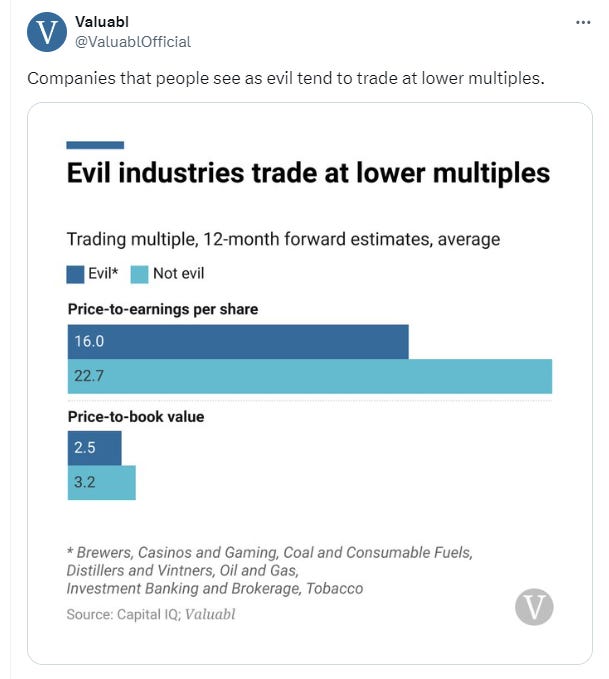

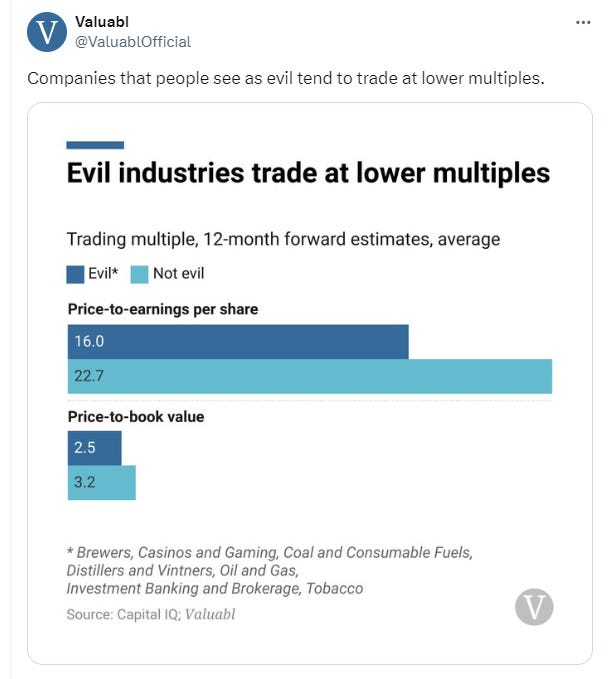

Greater focus on ESG criteria (Evil Inc. discount). This is to some extent related to point one. There have been stricter requirements and regulations on ethics for fund managers and investors in general. Evolution makes gambling games that contribute to people developing a gambling addiction. This is a harmful product. My view is that it's better that Evolution makes these games, as they co-operate with the authorities to put in place regulations and controls on the gambling industry, than that someone else does. I don't think gambling is going to disappear, we humans have been betting and gambling since the beginning of time. In recent years, however, this has led to a lower multiple on Evolution, and something we see across several sectors that are considered ‘evil’:

Prolonged consolidation phase after several years of strong growth. The return over the past three years may be negative, but if we zoom out to a five-year return, it is very good: A whopping 555%. Most of the return came from 2019 - 2021. The share price simply went a little too fast, and in the meantime the company's market capitalisation has consolidated. There have also been several media events (noise) with short reports, concerns about regulation, expansion and growth in markets that are either grey or black (i.e. markets where gambling is unregulated or illegal

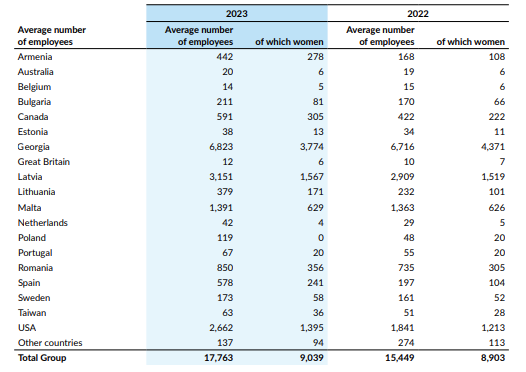

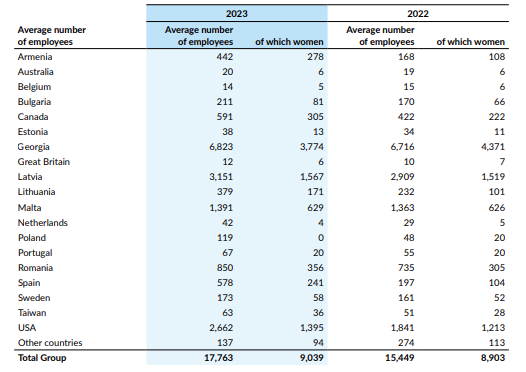

Georgia, foreign agents and Vladimir Putin: Evolution AB has its largest game studio in Tbilisi, Georgia, and 6,800 of the company's 1,600 employees are based in Georgia (38.6 per cent of all employees). The country has experienced a lot of turmoil related to a bill proposed to the Russian-friendly government in the country. There are fears of Russian invasion and great geopolitical uncertainty. What happens next is difficult to predict. Although Tbilisi is a major hub for Evolution, the company is well diversified, but war in Georgia would be a major damper on Evolution's ability to offer games in several key markets and should, in my opinion, hit the company's expected earnings significantly.

Here is the geographical spread of Evolution's studios:

This is the geographical spread of Evolutions employees

Hvor går veien for Evolution framover?

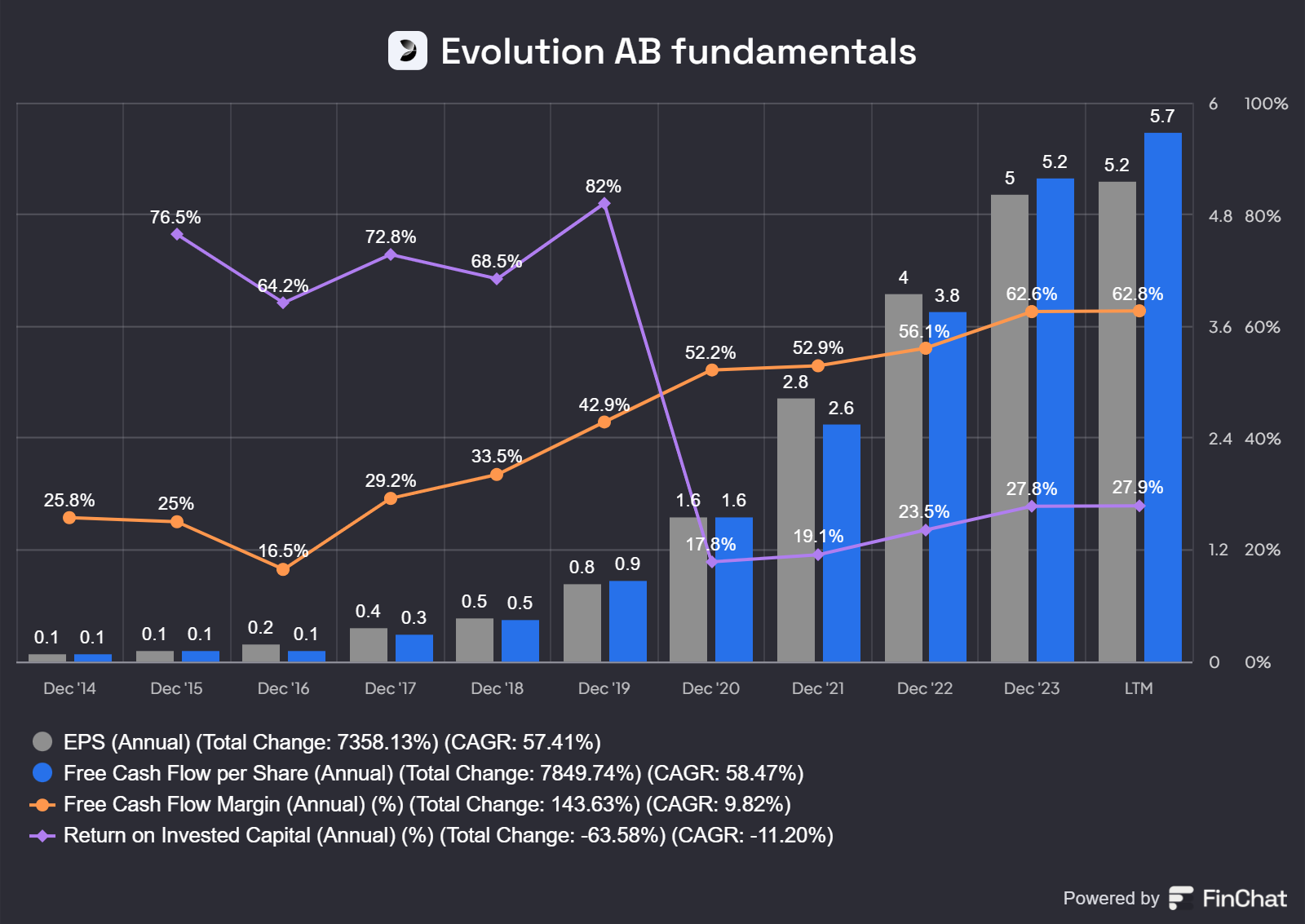

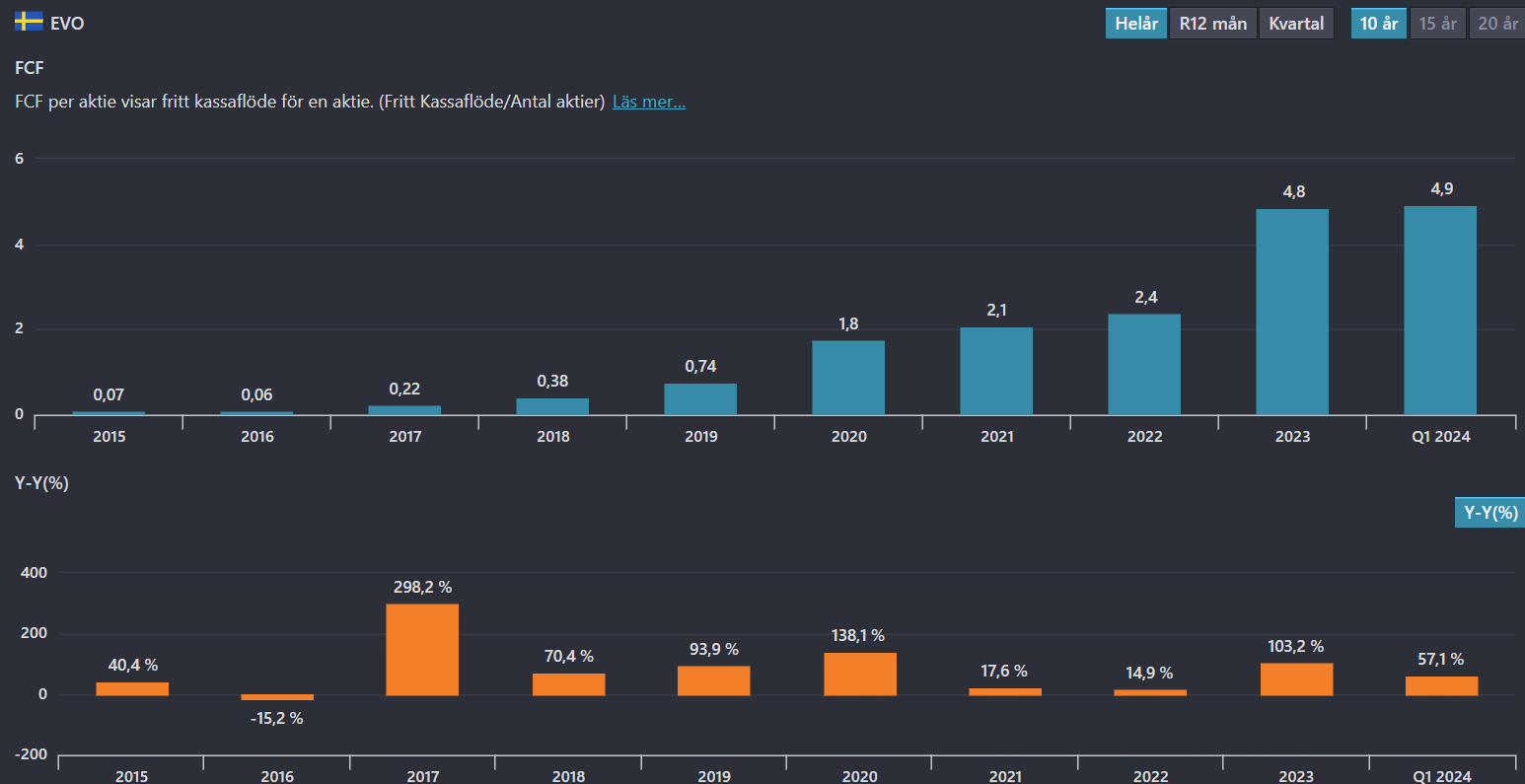

Evolution's fundamental development has been very strong over the past five years:

Over the past five years, EPS has seen strong annual growth of 52% a year, FCF has increased by slightly more at 52.13% annually. EVO's FCF margins are at an incredible 61%, and ROIC has stabilised around 27.5%. This is simply put: quality.

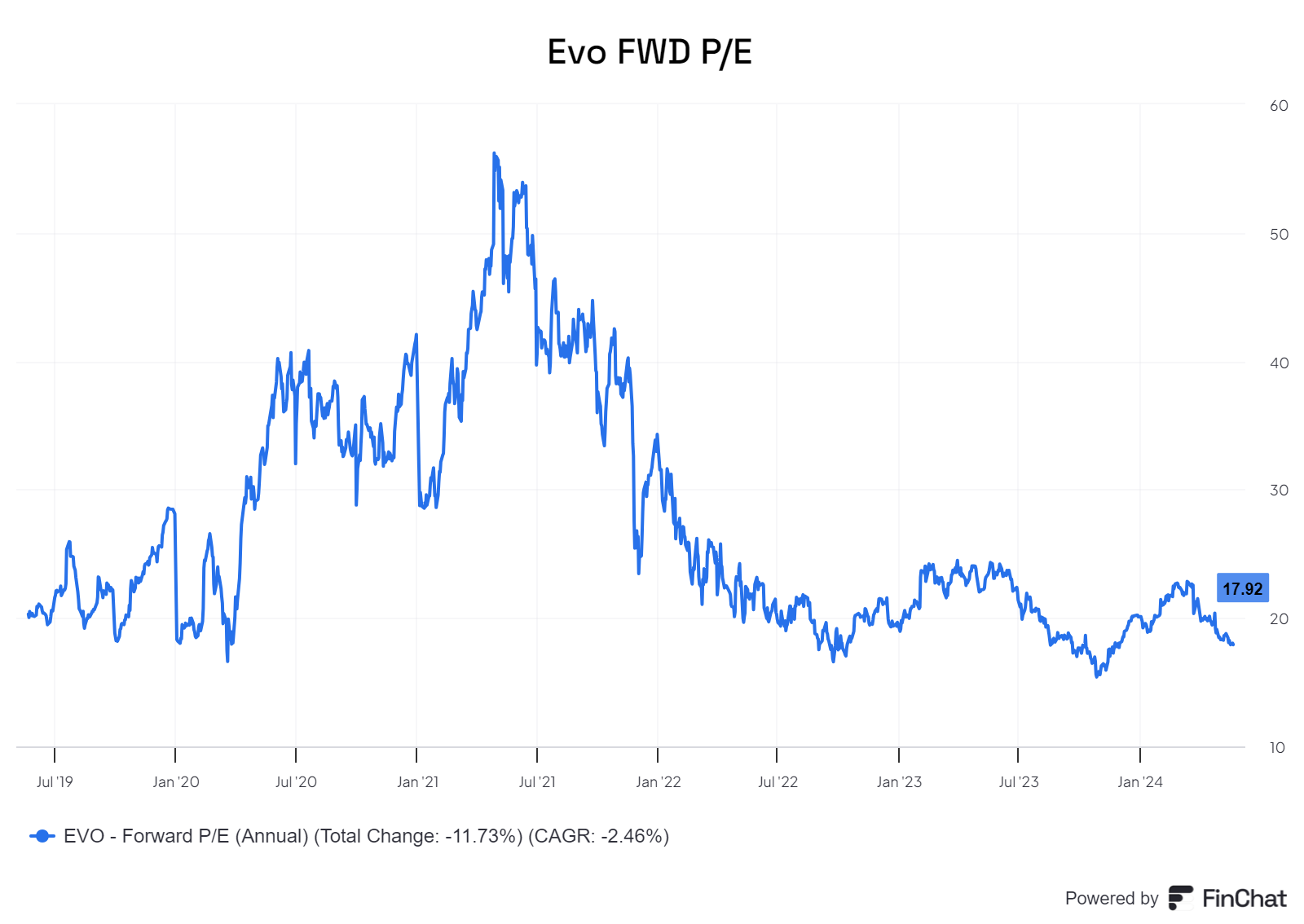

But as I said, the share price has not reflected the fundamental development. Today, the company is trading at a FWD P/E of 17.92, which is right at the bottom of what the company has been priced at over the past five years:

Furthermore, I have performed reverse DCF analyses, as well as a multiple scenario overview. These are only guesses about the future and should not be taken as reliable estimates.

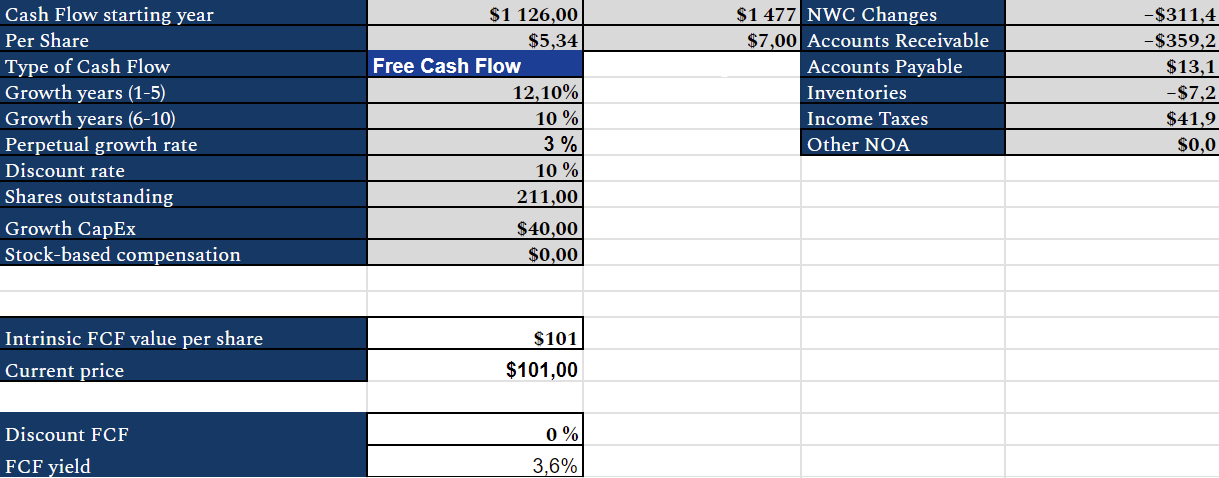

I have carried out three reverse DCF analyses, one by entering figures from the accounts into a template (1), the second is based on Børsdata.se's DCF calculation, which I have entered so that I get as close as possible to the current share price, and the last through stockinvestoriq.com's reverse DCF calculator, which is very useful.

In the following, where I've entered the figures myself, all values are in euros (including the share price). The most important thing to note is Growth years 1-5 and 6-10, which say something about how much expected FCF growth the market is pricing in, intrinsic FCF value per share is a result of this compared to the current price, which is the share price today (21.05.24).

The below calculation carried out in Borsdata.se is slightly less complicated and not hard typed. Here I have adjusted annual growth until I arrive at the current share price, and thus get 10.5% expected growth.

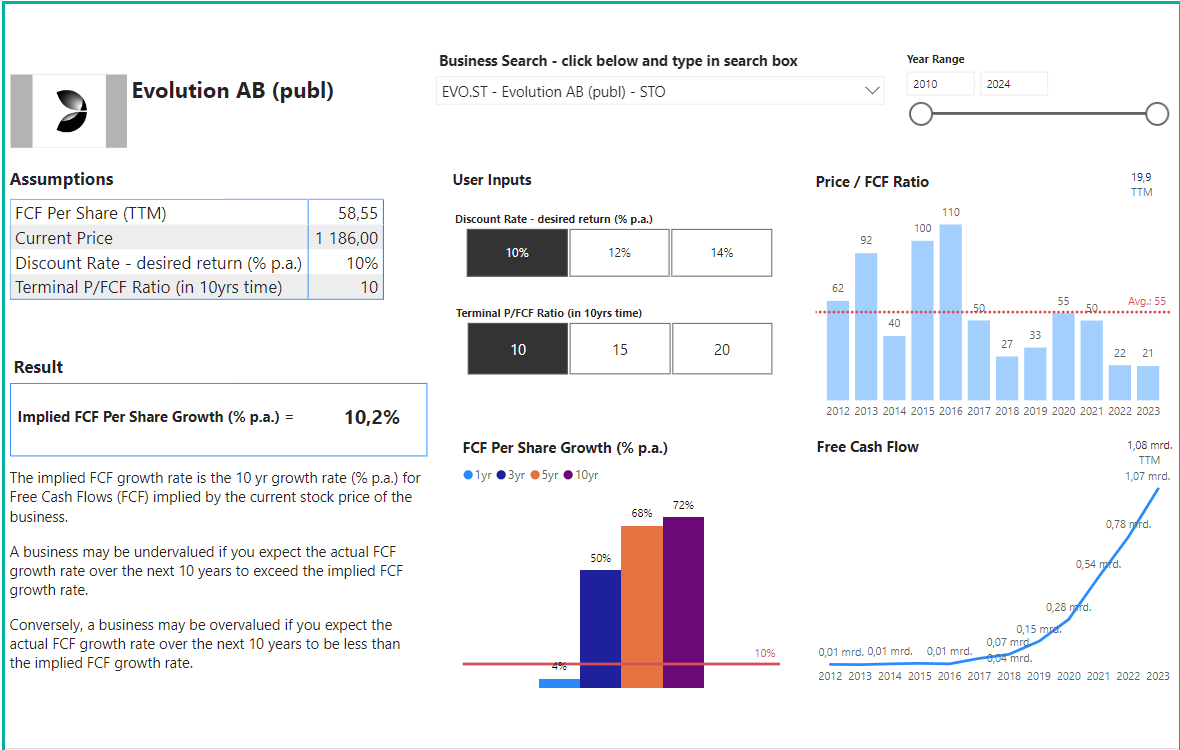

StockinvestorIQ is an open and free website where you can calculate expected growth based on FCF growth, price to FCF and required return (discount rate). Here, I have set fairly conservative targets, but also a low discount rate. With a terminal P/FCF of 20 (compared to a ten-year average of 55), the realised FCF growth is only 4.9%.

The reverse DCF method is about researching how much growth is priced into a company's share price. As can be seen above from several calculations, the implied growth in today's market capitalisation is around 10-12% FCF growth. Evolution has historically delivered much stronger FCF growth (last 10 years of FCF growth):

In other words, it looks like the market is pricing Evolution for a sharp decline in their growth in FCF. 10% FCF growth would in my opinion be the result of a very negative scenario for Evolution. The company has invested heavily in more employees, expansion of studios and is launching a record number of games this year. I strongly disagree with the market's pricing of the company today, and have been buying steadily since Q1.

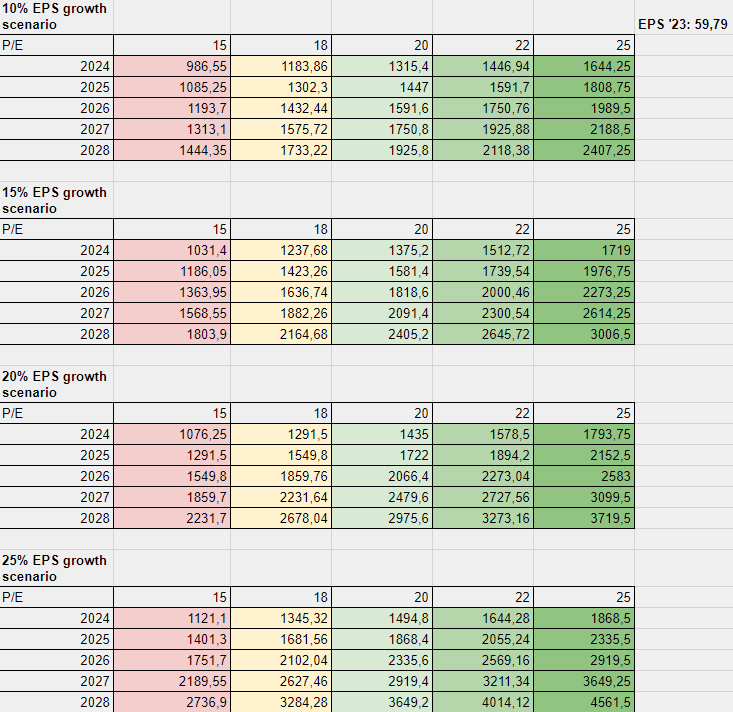

Furthermore, I will present a multiple analysis to show different outcomes of different EPS growth and multiples. As previously discussed, companies that fall outside the ESG categories receive more conservative pricing, so it is not inconceivable that there may be further multiple compression. Here are four different price-to-earnings scenarios:

Did you find this analysis valuable? If you buy me a cup of coffee, I will be motivated to continue writing company analyses.

Evolution has had an average P/E of 37.9 over the past 10 years. At the same time, the multiples have come down well since the fastest growth phase, and over the past three years the average P/E has been 30.1 and the lowest LTM P/E figure was 14.2 in 2019, closely followed by 15.8 LTM P/E today.

As shown earlier, the FWD P/E today is around 17.8, which is among the absolute lowest figures we have seen in the last 10 years. This is also characterised by a higher tax rate that will normalise in the future, and for which Evolution has started early to set aside funds. I consider 25 P/E to be an optimistic valuation for Evolution, but not impossible.

Given that Evolution's EPS CAGR over the past 10 years has been around 57%, it is not unreasonable to expect strong growth going forward, but I would not base my expectations on us seeing equally strong growth going forward. It's better to have realistic and conservative estimates than high and hopeful ones.

Let's assume EPS growth of 20% annually going forward (impressive numbers, but still well below half the average growth over the past 10 years), and P/E stabilising at 20. This gives an expected annual return of 15.3% from today's share price of around ~1180 SEK. There is an optionality of higher growth and higher P/E multiples baked into this assessment. At the same time, a more pessimistic scenario with 18 P/E and 15% EPS growth is also attractive, with an expected return of 13.15% from the current share price.

This was a quick review of where the company is now, and some attempts to explain the development in the share price. Perhaps the market is pricing out the studio in Georgia?

Maybe it's just a technical consolidation playing itself out? Or do larger institutional owners need to step in to create better price discovery? Who knows, I'm sticking to the fundamentals and will continue to buy on further declines unless it becomes clear that Russia is on the border with Georgia.

Videre lesing:

Great deep dives on Evolution AB:

If you prefer to listen to discussion, this is a great podcast episode on the company:

Ali Gündüz follows the company closely. The author has recently attended both the annual meeting and travelled to Malta to follow Evolution. Here are some of his articles on Evolution's most recent quarters:

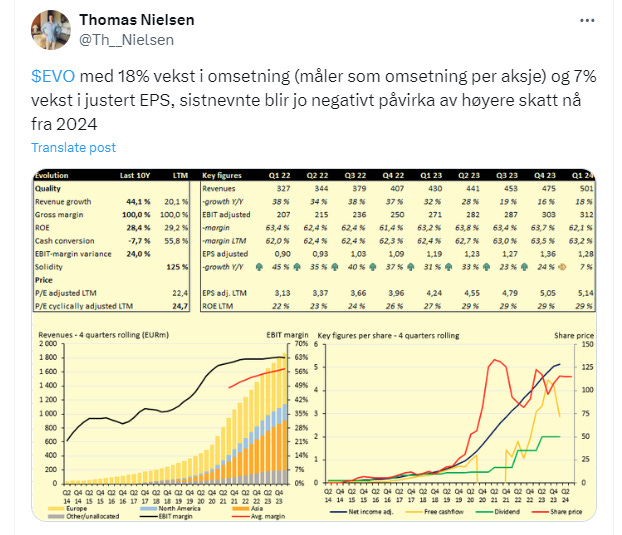

Thomas Nielsen who manages First Veritas owns shares and follows the company closely, here is his update from Q1 2024:

The companies discussed on this Substack should not be construed as investment advice. The content of this article is for entertainment and information purposes only, and the author is not a certified advisor or someone on whom you should base your investment decisions. If you decide to invest, I am not responsible for any decisions you make based on what is written on this Substack. I am and may be exposed to the securities discussed, and therefore have an interest in talking about them. My investments can and will change without me updating this immediately. All investments carry a high level of risk and may, in the worst case, break even.

By reading and using this Substack, you as a reader recognise that you are responsible for your own investment decisions and outcomes. The author is not responsible for any choices you make after reading an article on this substack, or the outcome of those choices.

Like all other information on the internet, the newsletter should be read critically. I encourage everyone to investigate multiple sources, and be aware that the writer has biases and possible misconceptions.