From categories to companies: A brief look into my portfolio

I will briefly lay out the reasoning behind my portfolio composition and how I think about my three main investment themes.

Dear readers,

I keep telling myself two things:

I want to run a concentrated portfolio, stop looking at new ideas!

I aim to be a long term owner, stop selling stuff!

These two are often connected. I like to learn about new companies, and when I find something great, I want to invest. With limited capital at hand, I sometimes like the new idea better than the old. However, sometimes these two principles end up in conflict. As a rather fresh investors, I have and will continue to make mistakes in my buys and sells. But I have found that I mostly make mistakes when I buy - chasing a good idea, but mostly a good valuation. This has made me realize that I’ve bought several okay/good companies for a usually good price. But they were not companies I would want to hold for years. It has been like this for the first half of the year.

Readers who caught my first posts and who’ve been following my writings will have noticed that I have been able to concentrate my portfolio, but I have made selling decisions more often than I like. In my opinion, I have been overactive in the market, but I also believe I have mostly made the right selling decisions.

This month, I’ve consolidated my portfolio further. Having reflected on what types of companies I want to own, I’ve started caring more and more about owning companies with a global or large geographical market. My small-cap holdings have at times been concentrated in smaller single-nation markets, such as Gofore, Dino Polska, and Royal Unibrew, among others.

This focus has led me to part ways with Dino Polska. It’s been on my mind for a while, and despite my view of the company as a well-run and solid-growth company, I’ve grown less and less comfortable with it’s single-market dynamic. Another factor has been the recent experience of trying to find information to understand daily movements in share price. As Polish is very inaccessible to me, I spent far to long trying to figure out what caused an outsized market reaction recently. After thinking on the experience, I came to the conclusion that the potential uncertainty outweighs the potential returns on investment from Dino Polska. Combined, these two reflections made me sell the company.

Another company I parted ways with is Alimentation Couche-Tard. It is in my opinion, a pretty darn good company, with a solid track record and an ownership that is known for stability and longevity. However, my conviction was shook for two reasons:

Fuel margin cyclicality. Growth should come outside of fuel sales, but fuel sales and margins will have large effects on ATDs development going forward (in my opinion).

I bought into the company due to price and not conviction, which has made me a bit unsettled about the size of this holding.

Therefore I preferred to pull the plug on ATD. This created an opportunity for further consolidation of my portfolio. I added to my SanLorenzo position at what I believe to be a very opportune time, and I have opened two positions: Constellation Software and Lumine Inc.

Owning the whole puzzle, not just the pieces

Having owned Topicus on and off for the last six months, the last couple of reports from Constellation have led me to realize that I would be at a disadvantage as an owner by only owning Topicus.

The board of both spin-offs and the management of all three Constellation companies are not working for the stand-alone companies in isolation. They work for the benefit of all shareholders, and Constellation shareholders are the majority of the owners and operators of the companies.

At the same time, spin-offs continue to trade at premiums to the mothership, while stand-alone CSU continues to outperform. This is probably a result of the abovementioned effect. The new idea looks better than the old. It’s easy to tell ourselves: “These spin-offs are smaller, their growth runways are longer, and they can just replicate the CSU playbook; therefore, they will have outsized returns to the original.” However, if spin-offs succeed, it will be to the benefit of all CSU shareholders. Or, to put it simply: it is better to own the whole puzzle than a portion of the puzzle pieces.

Now, as I continue to learn and adapt as an investor, things will change. I think that investors in general have to accept that we are always learning, and depending on the experience you have, mistakes will be made. I have so far made many buying mistakes, based on what I knew at the time.

I believe that the change to focus on quality growth companies with a globally or substantially geographical spread, growing at an above market rate led by competent and aligned management, will lead to outperformance of the general market. These will be essential for all my investments going forward.

As changes have been made, I found this to be a good time to give a brief overview of my portfolio, the overarching thematic categories, and a introduction to every single company I hold.

Get a 15% discount (and support my work) on your Finchat subscription through this affiliate link.

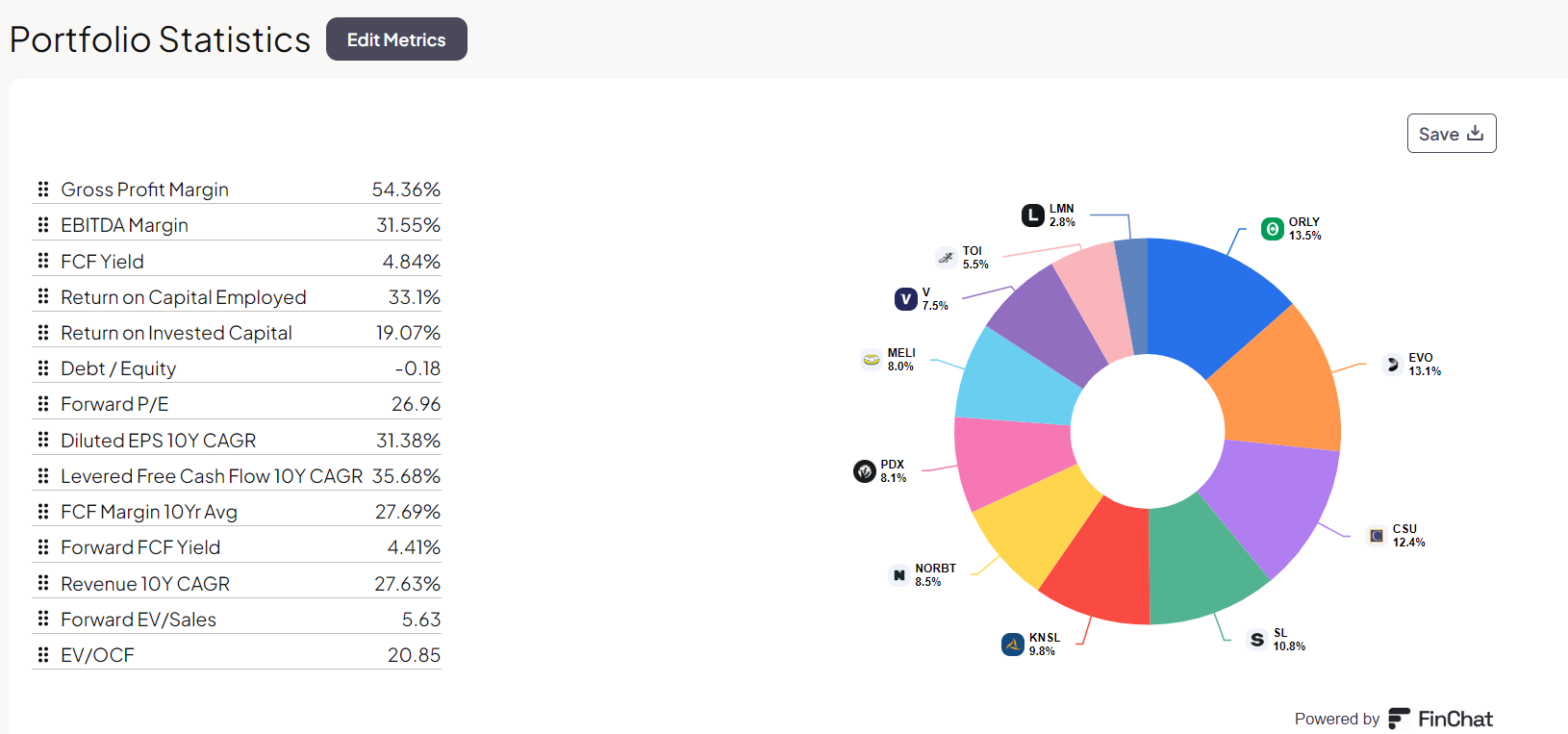

How I categorize my portfolio

I currently think of my portfolio segmentation in three main themes:

Niche dominators

Capital allocators

Wealth creation

Niche dominators (39.5% of portfolio)

For the first category, the Niche dominators, the goal is to identify and own companies that have products and businesses in niches where they are the absolute leader. The four companies I would categorize under this segment of my portfolio are Norbit, Paradox Interactive, Kinsale Capital Group, and Evolution AB. However, I could argue that most of my holdings operate within niches (excluding Visa), as I prefer owning the biggest fish in small or medium ponds. The reason I prefer companies operating in niches, rather than what I’d call generalists, is that these usually face fewer attacks on moats and less attention from market participants, often creating good opportunities for knowledge edges and buying. But most importantly, it is simply easier to continue to be the biggest fish in a small pond.

Capital allocators (34.1% of portfolio)

My capital allocator holdings are companies in which that I have high confidence in their continued ability to allocate capital through acquisitions of other companies, buybacks, dividends, or other investments for the best return to investors. These are companies with products and businesses that are particularly sticky and recurring. Through this defensive and less volatile earnings pattern, they can continue to redeploy capital at high rates of return over very long periods of time with a repeatable strategy. The two (but really four) companies I view as capital allocators are O'Reilly Automotive and the Constellation Software family of CSU, TOI, and LMN.

Wealth creation (26.4% of portfolio)

Throughout history, the expansion of human welfare and progress have continued on mostly undisturbed. There are instances where life as people knew it regressed, but that has happened very rarely (one example is the collapse of the Roman Empire).

In general, I am an optimist on the long term. More people are going to live better lives and have more resources at their disposal. In this trend, we will see a continued trend of global wealth creation. There are companies that are set to benefit from this trend and that are bound to continue compounding earnings from more people either becoming very wealthy or simply moving from lower to middle-class income. As this happens, more people will seek access to luxury goods, disposable income, material stuff, credit, and banking. That’s why I categorize my last three holdings, SanLorenzo, MercadoLibre, and Visa, as companies bound to grow from this trend.

Company introductions

I want to give brief introductions to all my holdings. As I have a tendency to want to write a lot, I’ll try to keep it brief this time around (and hopefully communicate their excellence through some very nice graphs provided by Finchat.io).

Speaking of Finchat.io, I’m very fond of using this platform to quickly and easily gain insight into companies and their financials. You can visualize portfolios, make watchlists, and create the best graphs out there by using their platform. The free version is pretty good, but the paid one is even better. Get a 15% discount by clicking on this affiliate link and contributing to the work I put into my writing.

Niche dominators

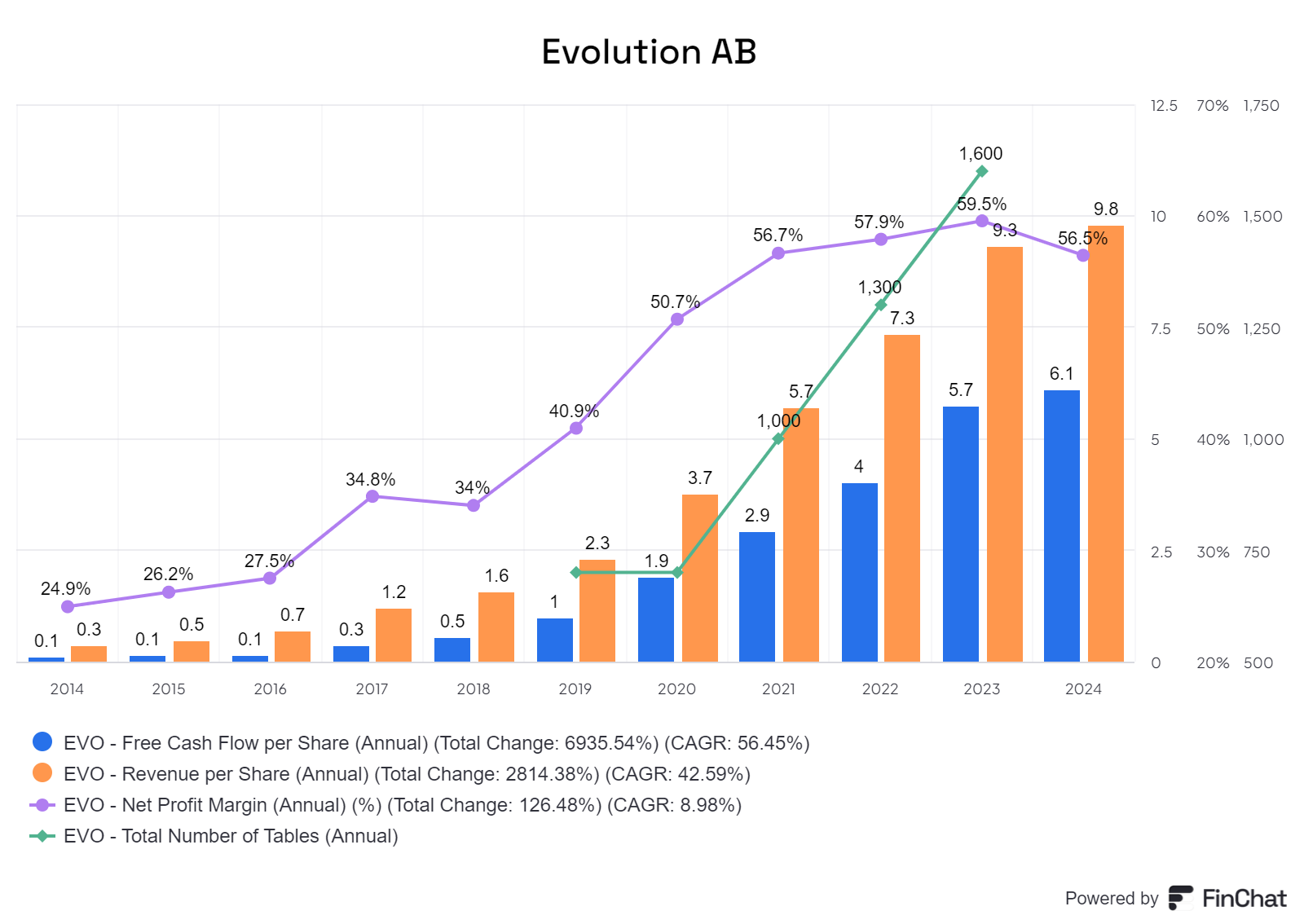

Evolution AB

Evolution AB, the leading developer, provider and operator of online gambling and casinos, Evolution had a mixed story. Despite the bleak medium-term returns, the company is trotting on. They are the absolute leader of online live casinos, with an unmatched product offering and excellent growth. They are now on the route to becoming a proper stock cannibal, with strong free cash flow streams being allocated towards returning capital to shareholders through both dividends and buybacks.

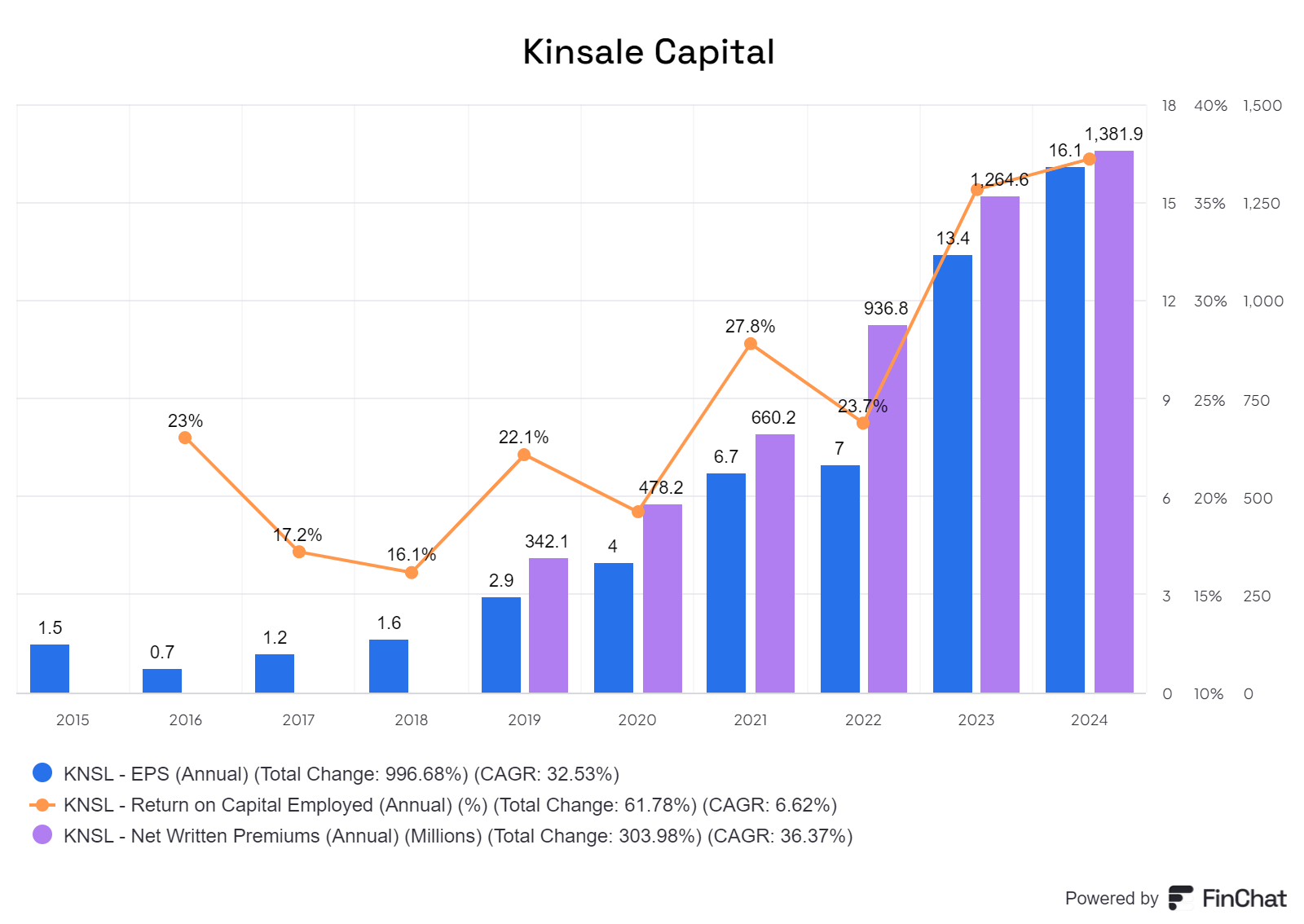

Kinsale Capital Group

Insurance company operating in the E&S segment, allowing them to better control for risk by increasing or adapting prices. They have a strong competitive advantage through their superior organisation and use of technology. It’s a company built from the ground up by management that is both experienced and very capable for the sole purpose of being the best in it’s niche. Kinsale will continue to take market share and out-compete legacy operators in a very strong niche.

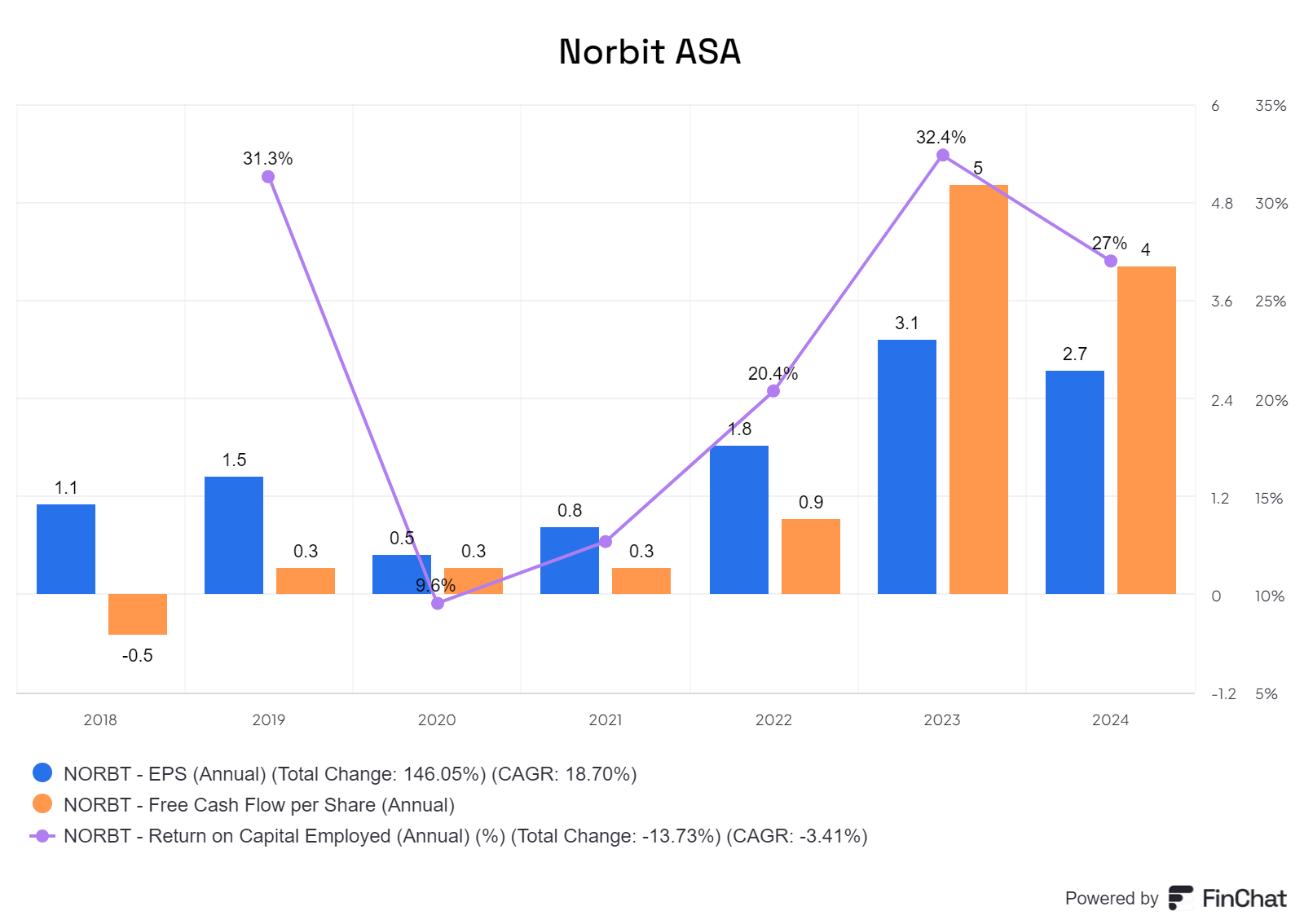

Norbit ASA

Norbit are in the business of problem solving. Yes, they make sensors, tolling units and underwater guard tech, but what they really do is try to find ways to create products that solve difficult problems. They explore for more niches to make and produce products. They have world-leading sonar offerings used by world-leading companies, an underwater guard point that Paris Olympiques used to ensure safety in the Seine and much more. They keep finding new and profitable products (and acquisitions) to ensure growth.

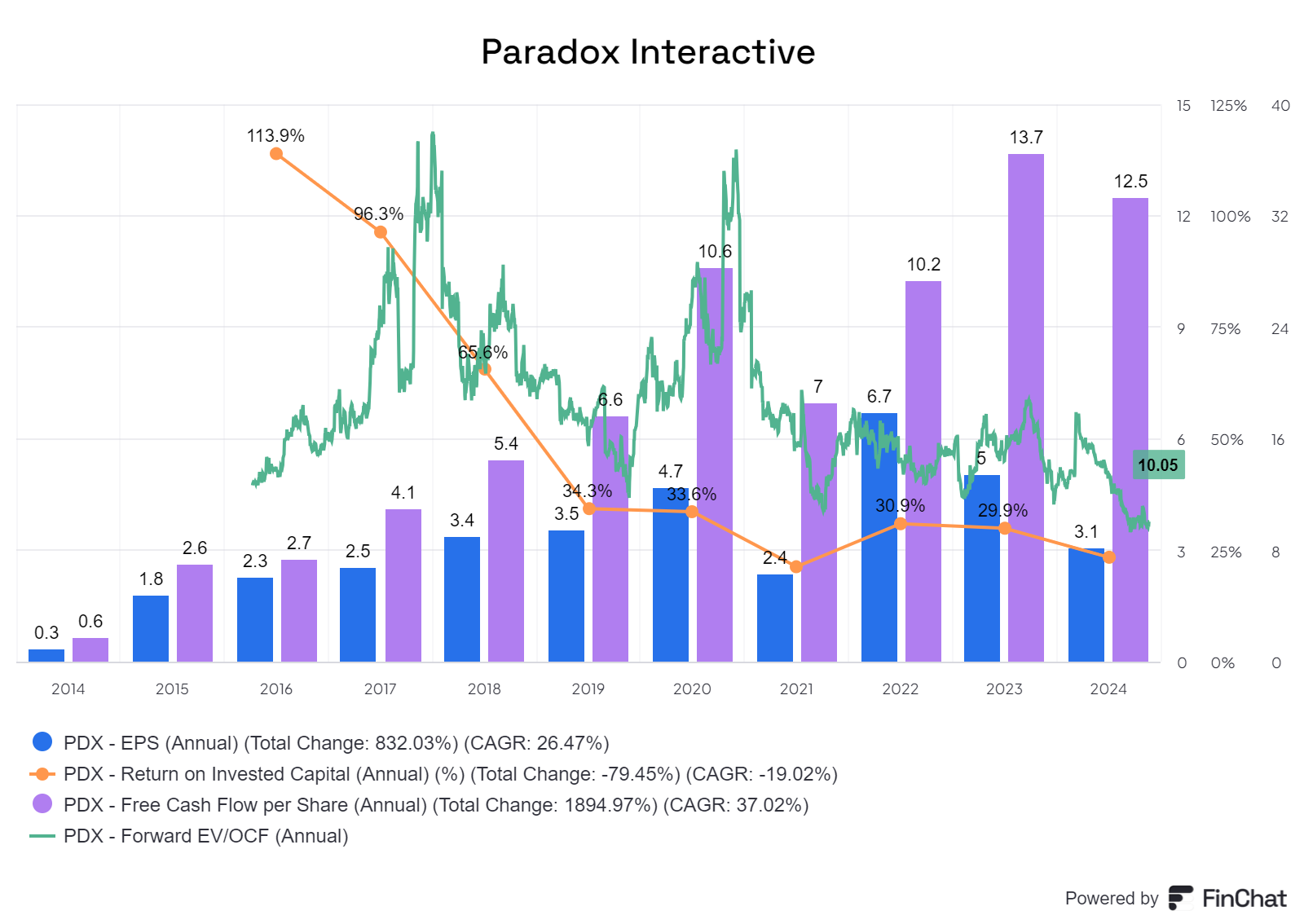

Paradox Interactive

A Swedish game publisher that makes long, hard-to-learn games that people play for decades and spend hundreds and thousands of dollars on. A remarkable story of boom and bust, that despite a volatile share price has shown a stable and recurring growth in underlying cash flows. Their products are used in university education and cater to a niche audience that loves to dive into details and create the stories themselves. However, headline failures have mired the company, distracting from the fact that the underlying business is running as well as ever.

Capital allocators

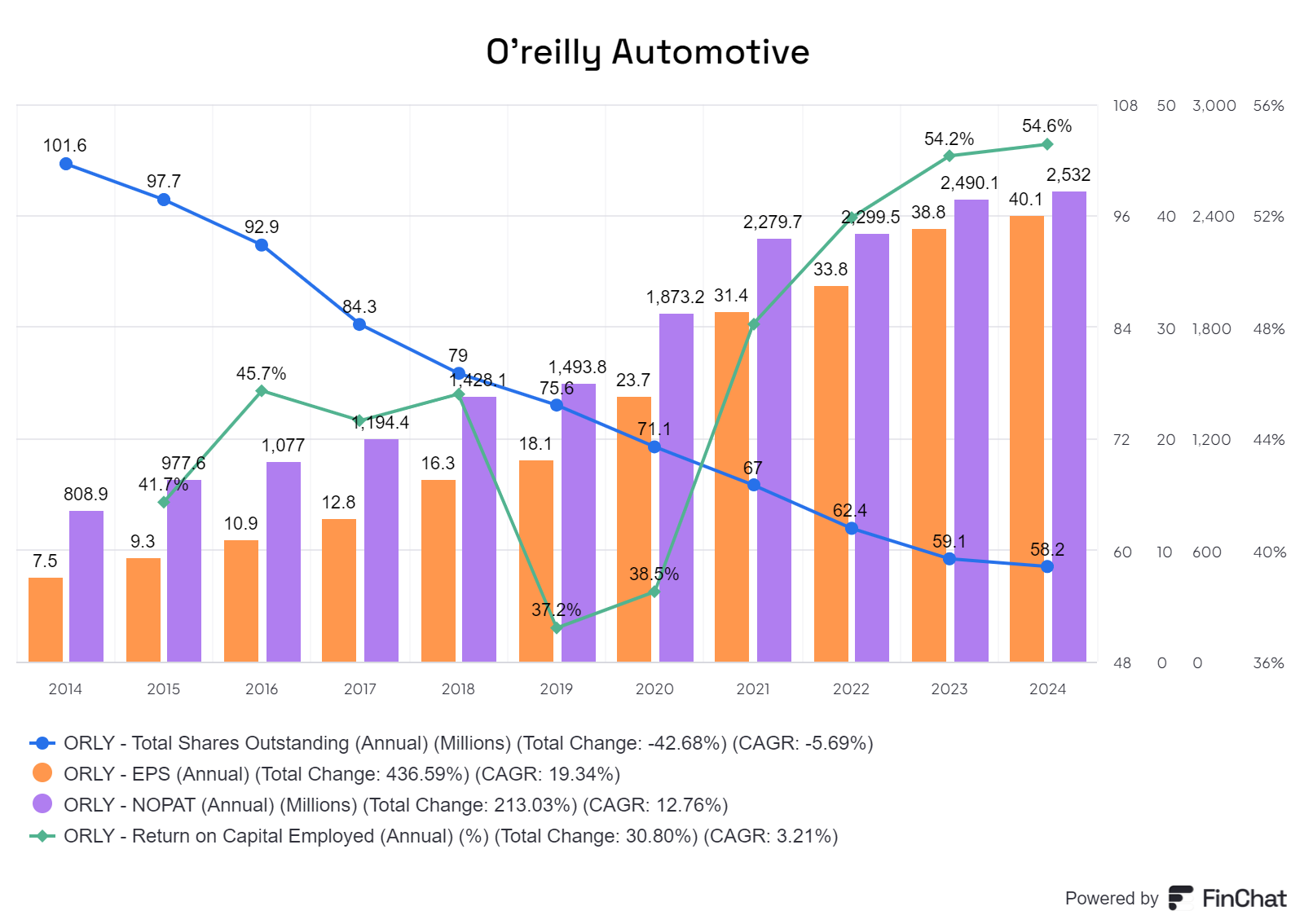

O’reilly Automotive

The company can use their business advantages to continue taking market share and out-compete other auto part retailers through an excellent distribution network, best-in-class inventory management and capital management, and use this underlying growth to strategically buy back shares, creating a positive self-enforcing flywheel of shareholder value creation.

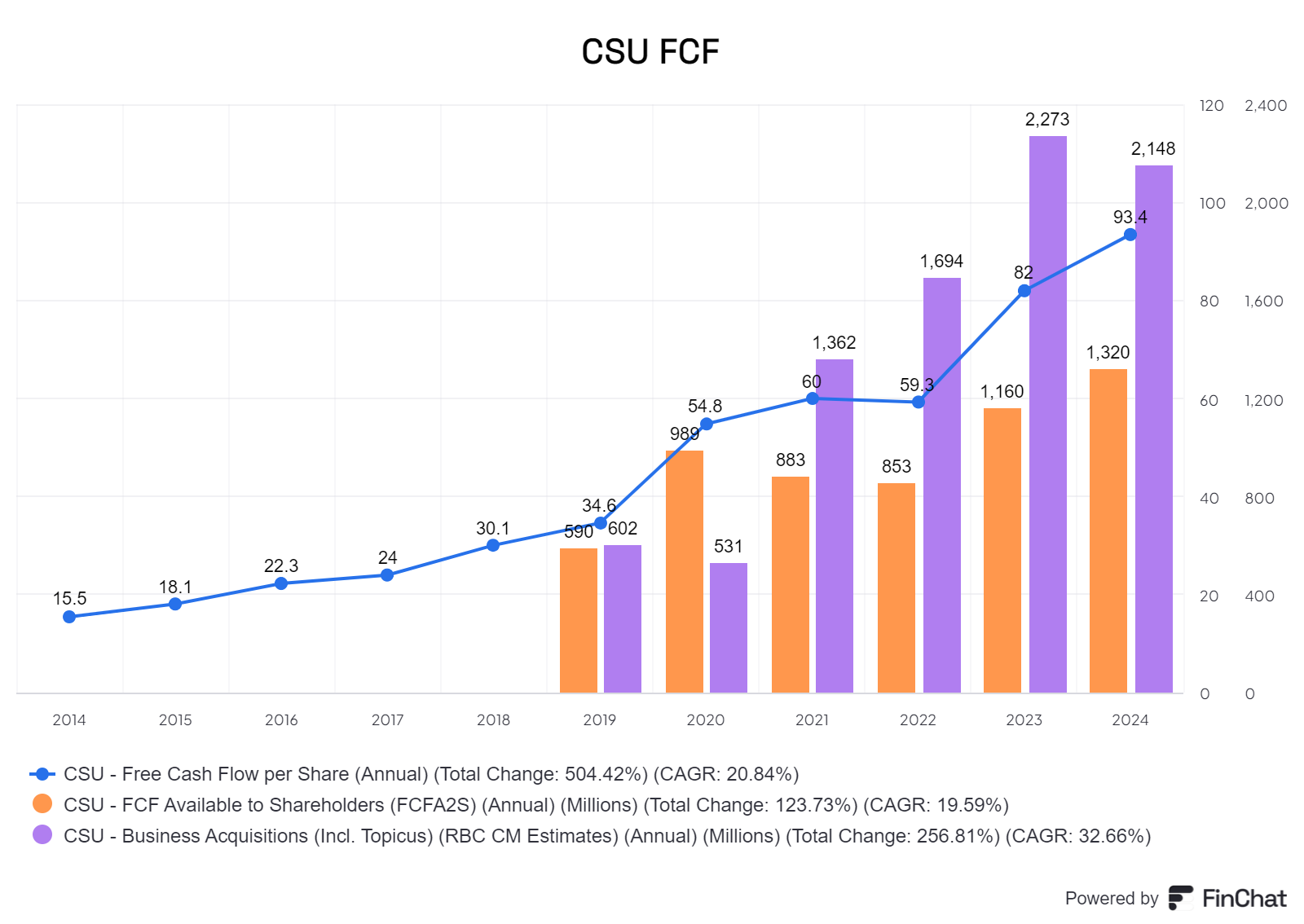

The Constellation Software family

Constellation Software are historically one of the most successful compounding stories out there. They acquire vertical market software companies at attractive valuations with the goal of being eternal owners. These mission-critical products are sticky, hard to change and excellent platforms to generate above-market returns for long periods of time. CSU has the winning recipe and culture to succeed with these acquisitions and are looking set to continue finding creative and ingenious ways of compounding capital at great rates.

Wealth creation

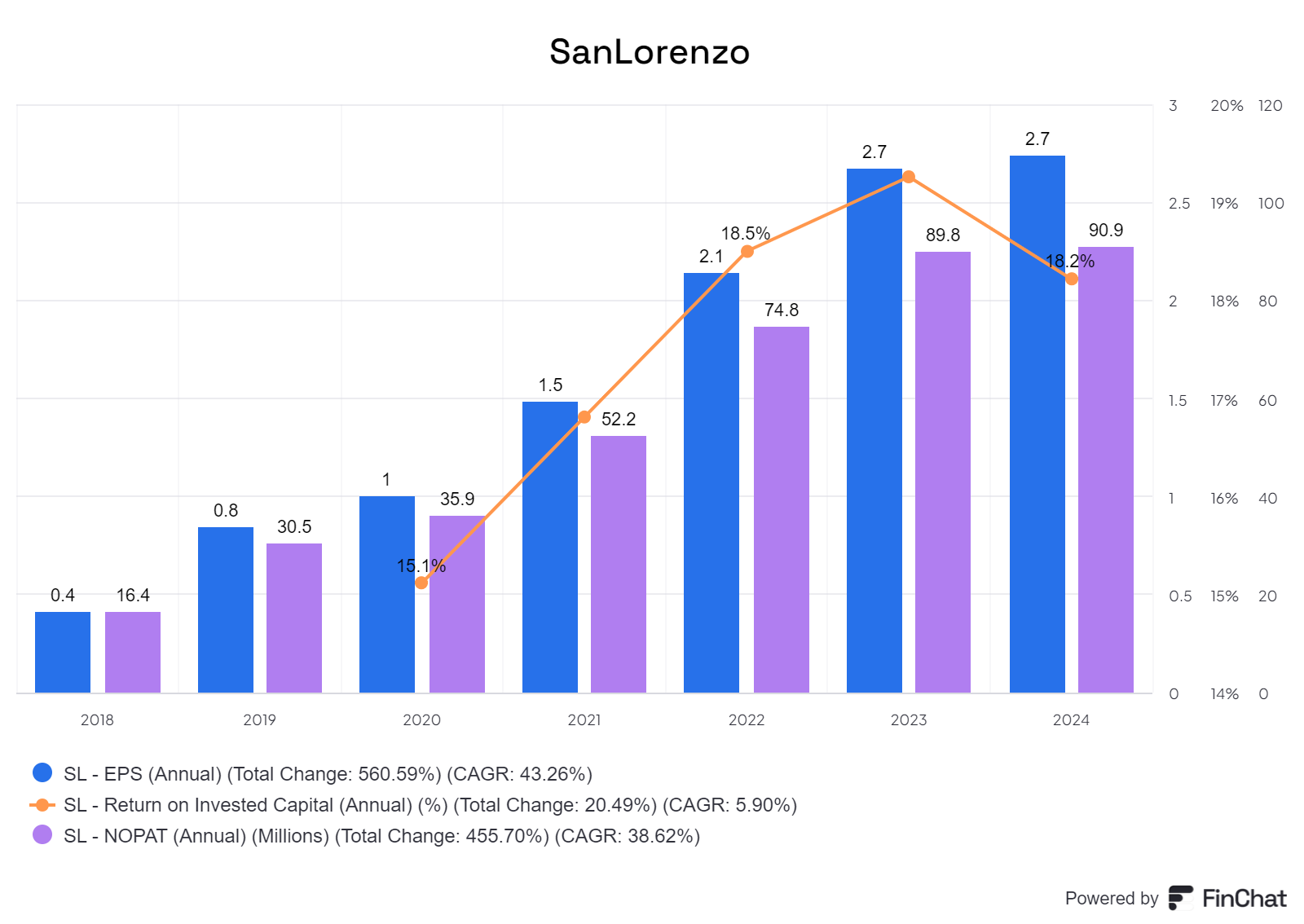

SanLorenzo

A yacht and luxury boat maker with aligned and experienced management operating in a recession-proof industry. Their working capital management is great, albeit they are a bit conservative with their cash management. They make the vehicles for ultra-wealthy people to live out dreams and establish their status in society, with a wide offering ranging from mega-yacths, smaller bluefield vessels and now also luxury sailboats.

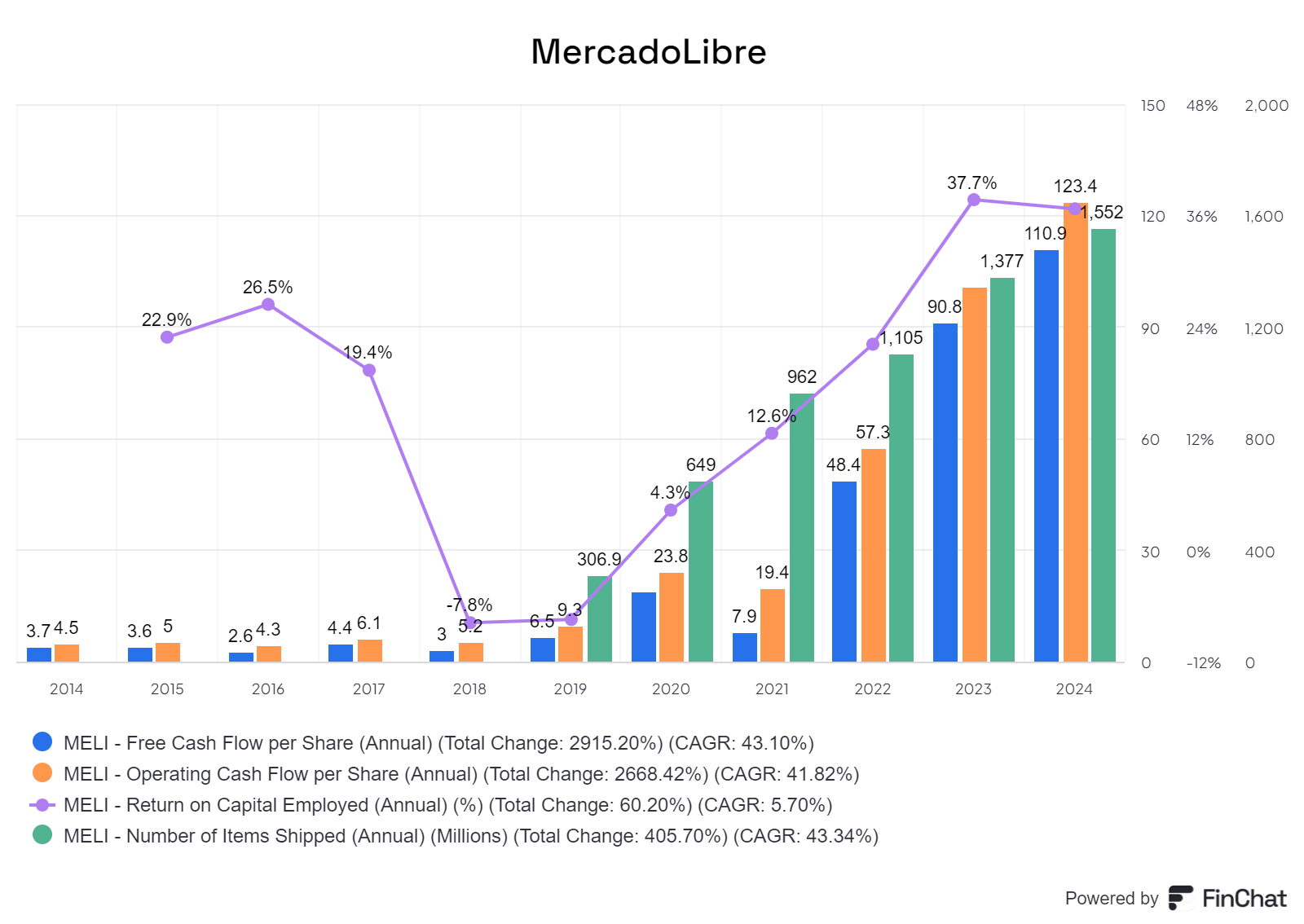

MercadoLibre

MercadoLibre, the online retailing, almost-bank and advertising powerhouse of Latin-America, is what I would call my high-growth play. I tend to shy away from rapid growth stories due to the difficulty of understanding and predicting when this growth will slow down. Meli is, however, an exposure to the economic growth that South-America is experiencing. They have an unmatched logistical and distributional network on the continent and are able to give same-day deliveries in small towns far into the Amazon. They are so dedicated into enabling online retailing that they’ve become a sizeable banking actor in the region and are working to give unbanked people of the region a digital payment offer. Marcos Galperin is also an operator I have great respect for, and I believe Meli is integral to the future of South-America.

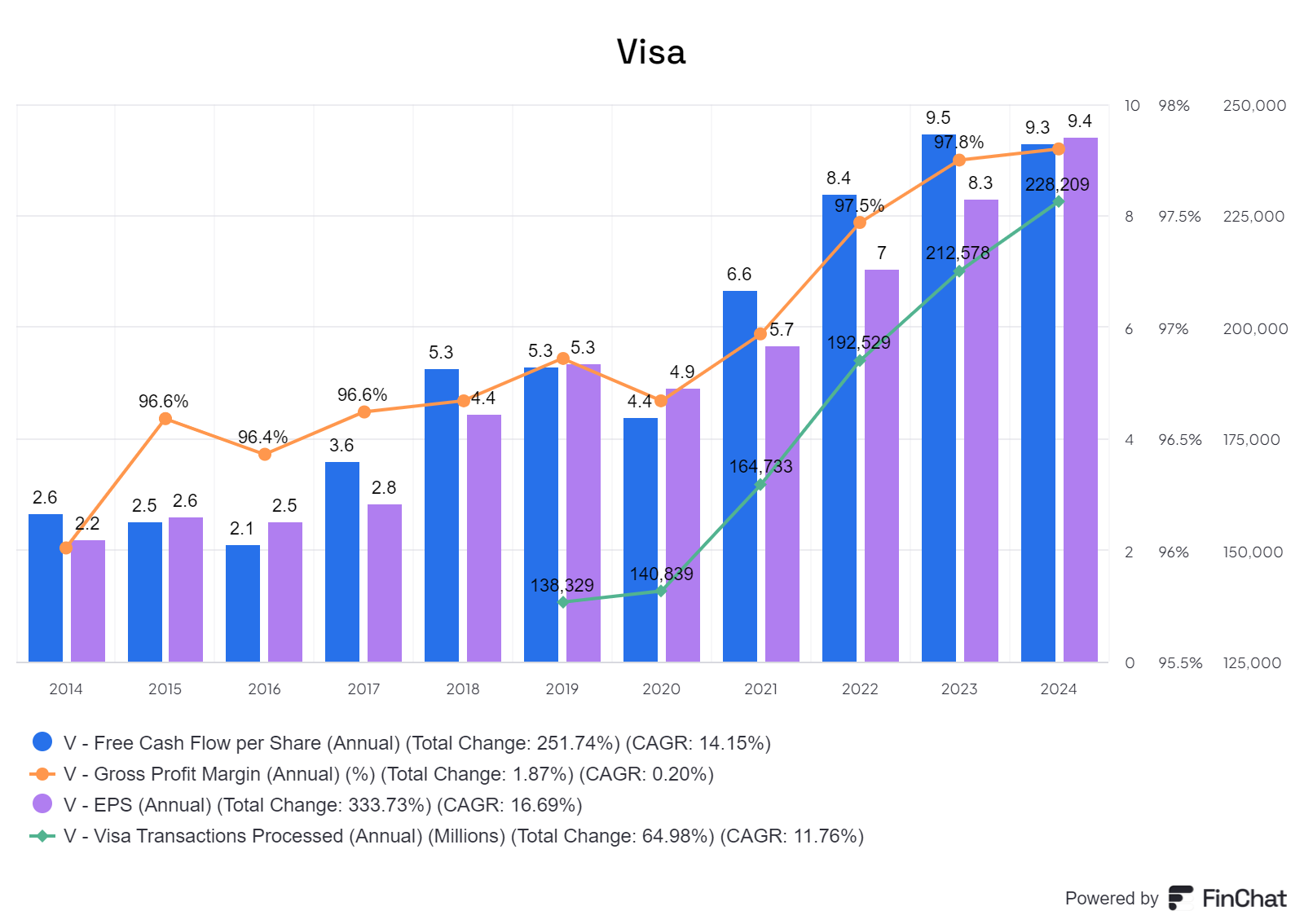

Visa

Visa is in everyone’s pockets, and Visa and Mastercard are the global payment transaction network. The moats of both companies are, in my opinion, amongst the very elite of the publicly listed companies of the world. They have unmatched profitability, an absurdly low need for reinvestment and growth that is likely to continue to not only follow global wealth creation but exceed it as more Visa cards end up in more pockets all over the world. Visa is one of the most impressive companies I know.

That’s it for this article! Thank you for reading, I hope this has been an informative introduction to my portfolio. Have any feedback? I’d love to read it, so please leave a comment!

If you like my writing and articles, I get a ton off motivation from readers treating me to a cup of coffee. It’s much appreciated! Another way to support my writing is by making your purchase of a Finchat subscription through this affiliate link.

Nothing I’ve written in this article should be understood or interpreted as investment advice. I’m a simple hobby investor who likes writing, and I am not competent or qualified to be giving investment advice. Do your own research, be critical of my assumptions and look into the companies discussed before making any investing decisions.

Excellent write up. I deeply appreciate you thoughts and insights regarding these stocks. Thank you!