Interesting insights - January 2025

Starting the year with several bangs and one let down.

Dear readers,

The year has started with a bang. A certain orange fellow tweets making stock prices rise or fall. In a public charade world leaders are negotiating and tugging and pulling, with media outlets as spectators and amplifiers. This creates tension and noise.

I’ve heard news about stock market movements several times this month from friends as well as the radio, and as I listen to the state radio which has little interest in the stock market, it’s been a remarkable month.

Nonetheless, it’s been a great start to the year for my portfolio holdings. I’m up around 9.1% for the first month, so things have started in a pretty hard speed.

Portfolio Updates

I’ve stated my intention to do as little as possible with my portfolio for this year. I failed to remain inactive in January (I apologize for sounding passive here). I made one and a half changes and added one company to my portfolio.

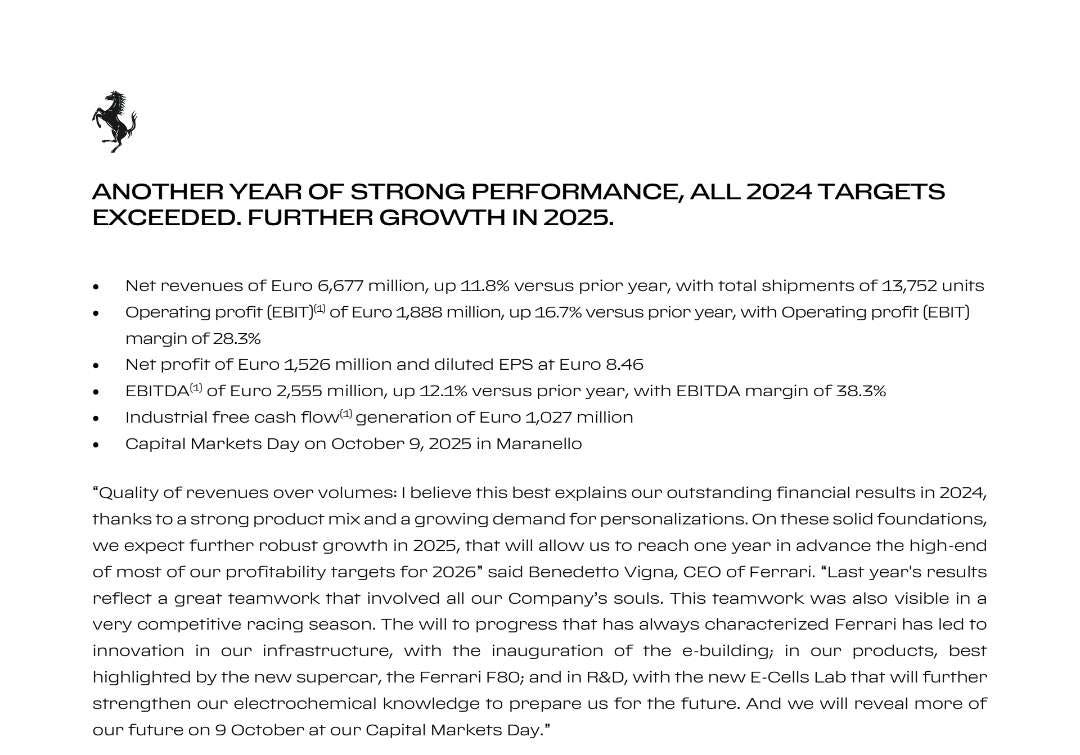

First, I sold Hermes and bought Ferrari. This turned out to be a lucky move in the short term. The decision to sell Hermes came after shares had risen 38% since my purchase this fall. I got the feeling that earnings and growth were being front-run, and investors were getting too optimistic. Hermes’ share price rose on the back of better luxury industry sentiment after several lower-quality companies such as Richemont provided better-than-expected results. This lifted every boat. Hermes is becoming priced for better-than-perfect results.

At the same time, Ferraris' share price seemed to have a muted development and some pessimism baked in. I want to stay invested in the best luxury goods makers in the world, and I view Hermes and Ferrari as sharing the position on top of the echelons of the luxury industry. There was another practical reason for my swap, and that is the fact that my portfolio is quite small. This means that I can’t respond well to share price movements in Hermes: It’s hard for me to trim or add without seriously altering the portfolio balance.

Thankfully, I got lucky: Ferrari posted some great results, beating estimates and expectations. The Prancing Horse is a year ahead of its guided schedule and even after raising its guidance, it seems to be posting conservative expectations. CEO Vigna stated that they’re expecting strong results throughout the year. In the first half of the year, we’ll see a good product mix drive strong results, and in H2 the F80 will launch which will add another boost to growth alongside the excellent growth driver that has been personalization.

The following post by Lux Opes does a good job at providing more detail to earnings:

Further, I did a little trim of one of my top holdings: O’Reilly Automotive. The share price has gone up quite a lot since my purchase. As it was around 13% of my portfolio I wanted to make it a smaller part of my portfolio, as I prefer to have a lower risk of short-term multiple contractions in my overweight positions. O’Reilly now sits at around 9% of my portfolio.

This allowed me to add Gofore Oyj and with some fresh money: Momentum Group. I owned the Finnish IT consultant earlier. My original thesis was that 2024 was bound to be the year where IT spending finally picked up after the Covid spending boom. When it became apparent that the market (and then also growth) probably wasn’t going to be picking up in ‘24, I exited the position somewhere in late spring. After seeing results from Bouvet tick into the positive side, and seeing Gofore become a bit more realistic in their growth targets during their CMD (changing it from 25% to 20% annual growth) I became a bit more optimistic about the plan going forward. IT consultants have a great way to create capital-light compounding effects through great service and sharing of best practices. We’re bound to see organizational IT spending start increasing as corporations, governments and organizations look to adapt to the new AI reality. In addition, Gofore has a realistic chance to expand through the DACHs market in which they’ve identified several good opportunities to reach their growth target.

Momentum Group is the subject of my next company coverage. I’ll be looking to publish my deep dive sometime before their annual report, but I am very optimistic about this business. Springing out of the Bergman & Beving root system, with excellent operators and being positioned into niche distribution I think this is a viable candidate for a long-term compounder.

Without further ado, this is how my portfolio looks at the time of publishing:

Company news

Several of my portfolio companies have reported their earnings so far. I’ve already touched on Ferraris, but I want to catalog some thoughts on the results my companies have posted so far.

Evolution AB

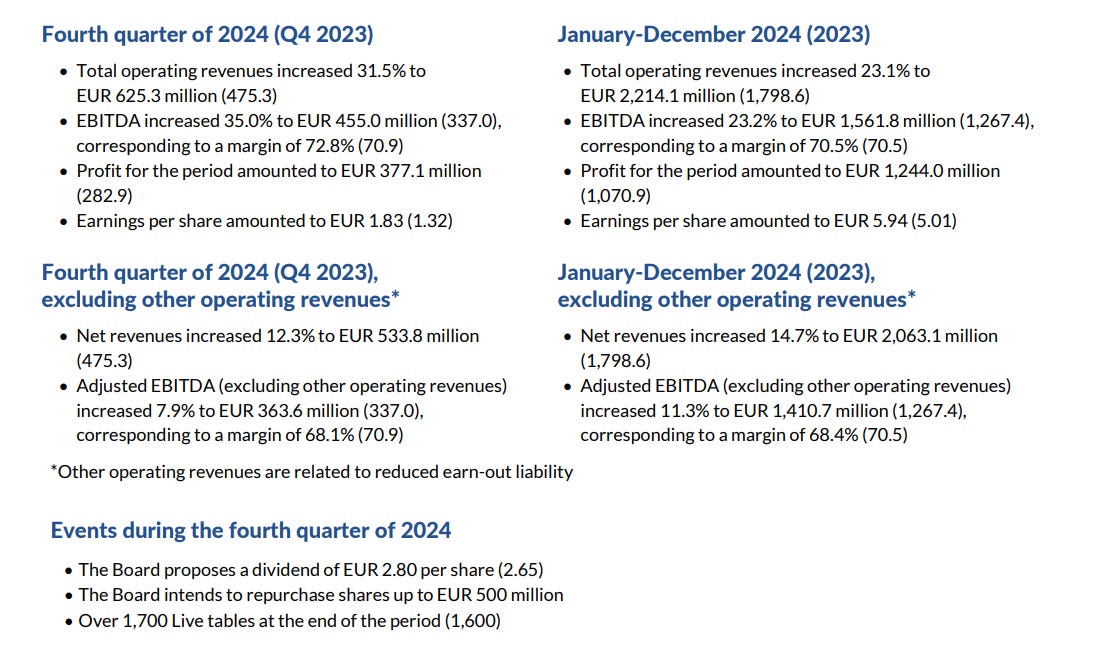

The leader of online gambling and live casino games globally posted what I would call OK results.

I am optimistic about the financial development of EVO going into 2025. The company has had the worst year ever in 2024, with nothing but bad news. A strike in their largest studio cyberattacks pawning off their games and stealing customers and revenue in their biggest markets (Asia), scrutiny over compliance issues both by short reports and governmental regulators (UK) whilst investing for growth in a large market that has high capex requirements to get started (US).

At the same time, the company posted a 14.7% increase in revenue and 11.3% in EBITDA growth. When a company experiences one or two negative events in a year, this is usually enough to offset growth. With this context in mind, I don’t think Evolution did all that bad. Lowering the margin guidance should have been expected in my opinion, and I was quite frankly surprised by the market reaction to this.

I’m very happy seeing Evolution increase their shareholder return by quite a lot. Buybacks increase by almost 25%, and dividends rise (but thankfully not a lot) by around 5%. Evolution is also set to have around €700mln left over in cash to either spend portions on share buybacks in H2, or complete acquisitions.

At the same time, the market reaction to Evolution’s earnings is nothing but frustrating. I would not be surprised if the share price reacted negatively to these results at a price of say 1 400 - 1 600 SEK per share. But shares tumbled over 8% on the day, and weakness has remained. To me, it looks like a shakeout. Unfortunately, it’s hard to see any signs of institutions accumulating or any concrete catalysts on the horizon. I doubt the sentiment and/or share price will turn positive any time soon, so I’ll be taking Evolution as a lesson in patience and discipline, as I see no rational reason for selling a predictable mid-double-digit grower over many years for 10-11x forward earnings based on conservative growth expectations. Oh well, we can always console ourselves with bigger share buyback effects with the depressed share price.

I recommend checking out

excellent summary of the earnings for more detail, and less whining:

Visa

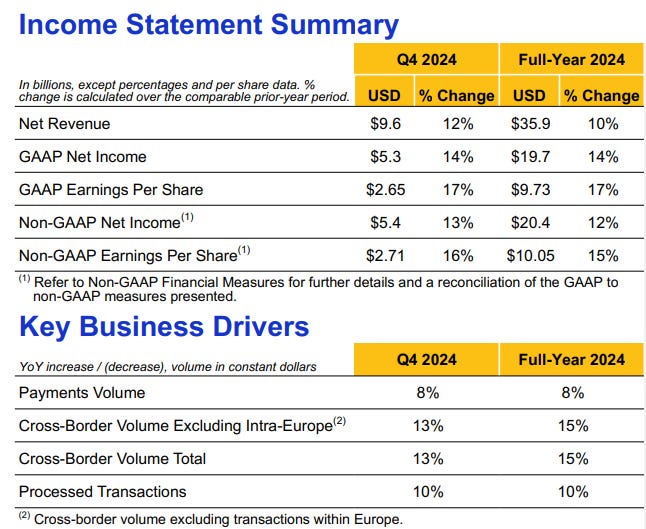

As one falls, another rises. Reporting on the same day as Evolution, Visa posted the type of results that prove why I want to own them and why I will find it hard to part ways with shares if they ever started becoming to stretched valuations-wise.

As we can observe, they grew EPS by 17% year over year, posted great results in their Key Business Drivers, and seem to be chugging along at the speed we want them to be going at.

The financial payments sector has had a great start to the year, with both Mastercard and Visa beating expectations and companies such as Adyen and Fiserv chugging along.

Visa is probably the least sexy of this sector, but serving as the toll booth on the global spending I think this is a great place to be. I see it likely that Visa will have another good year, but doubt it will be as strong as it was in the latter part of last year. Anyway, a great company to have serving as a foundation for my portfolio.

Topicus

Topicus was one of my top picks for 2025, and what a start of the year they’ve had!

This serial acquirer in the Constellation family had a slow 2024. Last year they deployed around $130mln, and since splitting out of Constellation they’ve averaged around $100-135mln annual spend on acquisition. The Dutch-Canadian lizard has so far this year managed to deploy well over $300mln in acquisitions and investments! Cash deployment and acquisition of companies is Topicus’ bread and butter, and seeing this start of the year is highly positive.

They have bought companies in two new markets: Cyprus and Indonesia. The latter entry is particularly interesting, as the thesis for investing in Topicus has for many been that they will be able to do what Constellation has done in North America (and globally to be fair) in the fragmented European markets. But now Topicus has a foothold in four Asian countries (Vietnam, South Korea and Thailand as well as Indonesia)*. This adds an interesting optionality to Topicus - but where they buy companies is not what is important: It is the rate and price.

But more impressively is the acquisition of Belgian Cipal Schaurbroek and their investment into Polish accounting and business-software acquirer Asseco.

Cipal Schaurbroek looks to be a huge acquisition for Topicus, adding around €110mln in revenue. The opportunity came from motivated sellers, and this company has been joint ownership between the owning family and governmental agencies. This suggests that profitability hasn’t been at the core of Cipal. Given Topicus and CSU’s track record of improving margins I think this will be a substantial driver of growth in Topicus. Cipal is the largest acquisition Topicus has done since going public.

Another pretty huge deal has been Topicus's swift movement to secure ~25% of Asseco. This Polish software company is a publically listed company, which for the first three quarters of 2024 produced around $3bln in revenues and around $90mln in net income for the first three quarters of 2024. Asseco is one of Europe’s largest software companies and has operated as a serial acquirer for years. Topicus will become the leading shareholder of Asseco, and I believe we should expect them to work their magic with Asseco on several sides of operations:

Through better contract bidding and operational efficiency

Better capital deployment and disciplined management

Margin improvements

The Asseco deal is also beautifully structured: They bought shares from the selling party (Cyfrowy Polsat and Asseco itself) at 85pln, representing around a 25% discount to the current market price of around 116pln. In addition, the proceeds from the sale of shares from Asseco to Topicus will be paid out to the owners of Asseco. This means that Topicus will get back around 25% of the cash they’ve paid to acquire shares in the company. The cash deployed to buy shares in Asseco represents €420mln capital deployed at an initial return of around 15%.

Again we see why Constellation and its family is at the forefront of serial acquirers.

What I’ve enjoyed learning about in January

Podcasts

This great episode by Best Anchor Stocks and John Rotonti on investing in industrial and infrastructure:

Speedwells yearly summary and Q&A:

I discovered Far from the finishing post this January, and my life has been better for it. So far this is my favorite (but be sure to check out this episode with the Chairman of HGTrust, Jim Strang as well):

Writings

I’ve read this annual report by REQ Capital (a serial acquirer-focused fund) several times so far, and I’m sure I’ll be diving back in every now and then. Read REQs Annual Letter here.

This run-down on Mastercard’s recent performance by Douglas Ott is excellent:

For readers who follow Evolution AB, I highly recommend this summary of Ali Gündüz's visit to ICE:

This very interesting deep dive into Nilörn AB, a Swedish clothes label maker:

* In my first post I wrote that Topicus had operations in two Asian countries, but they have in four. I’ve updated this 06.02.2025.

As always: None of this should be understood as investment advice. I am a hobby investor, with no professional training. I may sell or buy stocks without disclosing it at once, so you should not be following me. Do your own research, or you are bound to lose conviction when convicition matters.

Thanks for sharing the req link!