Interesting insights - July 2024

Trying to follow earnings while kicking back.

Dear readers, a month has passed, earning results have been released and I have relaxed! I hope you have had the opportunity to take time off, kick back, maybe get to enjoy some of the sports that have been played this summer, or that you are headed for vacation right now.

I actually had a great summer, travelling to a remote area far away from home. This let me stay away from looking at stock prices for two entire weeks. When I got back online, not much had happened as per portfolio price change and I hadn’t missed anything important. Maybe it is something we all should try more? Stay away, and don’t pay attention.

Remember, life is short, and as investing is mostly a waiting game, we should all spend most of our time not following the market. Now, that is enough of me trying to justify not having posted anything this whole month. Let’s get on with it!

Portfolio updates

I have made some changes to my portfolio.

Exited Gofore and Medistim. The first was sold due to me wanting to focus more on companies with a global market. Gofore is too geographically concentrated for my taste. I might be overthinking it, but I believe the margin of error is smaller for companies that are so concentrated on one market, especially one with a language barrier (to digest news and understand what is happening in Finland is a tough task).

Medistim was sold as somewhat of a necessity. I wanted to buy more Evolution AB but did not have the funds for it. As I doubt Medistim will have a share price appreciation in the near future, I decided to move those funds to Evolution and hope to get aboard the Medistim train before it potentially takes off again.

Other than adding to Evolution AB, I have opened a position in Visa (stupidly right before Q2 earnings) with the funds freed from the Gofore sale. It is a great company, with a global reach and margins to dream of trading at historically cheap multiples. Why complicate things any more?

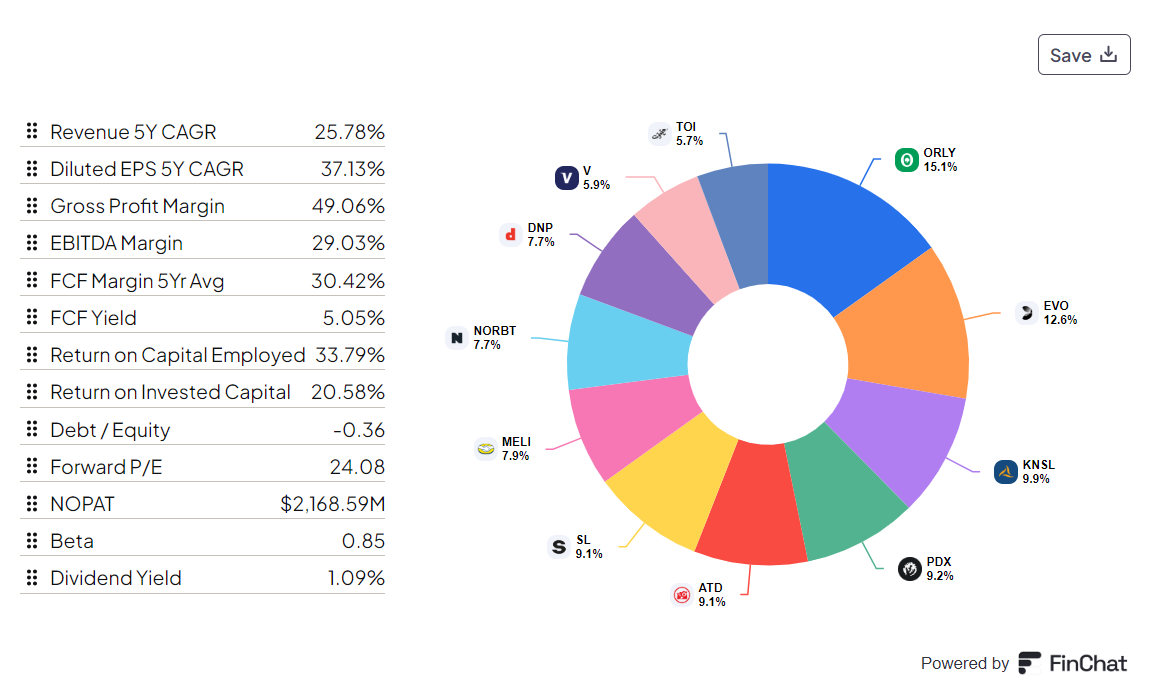

My current portfolio allocation and metrics:

Earnings galore

A lot of my companies have presented their quarterly results. I will not go too much into detail on each of these events, but I will try to share great pieces on the quarters and add colour where I can.

Let’s start with the presentation that caused negative share price reactions (or the bad ones):

Evolution AB

Evolution AB presented their Q2 results on July 19. and the market was underwhelmed by the apparently falling margins and slowing growth. It is definitely something to pay attention to, but I believe that Mr. Market is throwing a fit at short-term numerical misunderstandings.

First of all, the underlying growth of the company is still great.

As we see above, the cash from operating activities is up 34%. Network activity (rounds of Evolution games played) are up 37%. These metrics are great indicators of growth.

Evolution AB also invested into more people, meeting the demand of dealers and tables that have been pent up. The share price has dropped to below 1000 SEK a couple of times since Q2, and I have added to what I find to be a great opportunity.

Margins are under pressure for the company, and U.S. growth seems to come at a price for the rest of the group. One of the pieces below discusses this well; however, regulators are working on a nation-wide regulatory framework in the U.S., and sentiment in key states such as New York is turning more positive. I’m not too worried about these last two slower quarters.

Now the capital framework is the big news. Depending on the growth, the share buybacks that Evo will commence in the coming five years should result in the company returning around 45%–60% of the current market cap in buybacks and dividends combined. This cash flow return is, in my opinion, wild, especially considering this is still a company in growth mode (37% increase in activity YoY is a number that signifies a growth company).

Here are my two favourite articles on Evolution ABs Q2 results:

Paradox Interactive

Paradox Interactive reported its Q2 results on July 25. The results were horrible if you take it at face value. EPS was down 88% compared to Q2’23.

However, the second quarter for Paradox showed the strength of the company’s core business model. In the quarter, Paradox achieved MSEK 575.8 in revenues, a drop of 22% from last year's Q2 MSEK 737.3. This looks bad, but Q2’24 was the company’s fourth-best quarter in its history, revenue-wise. The reason revenue is down 22% YoY is because they launched no major base game in the quarter, whilst Age of Wonder 4 (the biggest success of 2023) was launched in the comparable quarter.

The immense drop in EPS is due to the write-down of the Life by You game, where the hit to the bottom line was taken in full this year, despite costs having been paid and accrued earlier years. I think the comments on Q2 from CEO of Paradox Interactive, Fredrik Wester, puts it well:

No article tips on Paradox Interactive, as I promise that

and I will publish our deep dive on the company some time this month (probably this coming week). But I give you this meme as compensation:

Topicus

Topicus, the ugly duckling of the CSU family (I’m just jesting), presented it’s Q2 results on 01.08. The company presented strong cash flows and good growth in cash from operations.

Net cash from operations +49% YoY H1’24

Free cash flow available to shareholders +53,9% YoY H1’24

So far this year, Topicus has acquired 9 companies for a total of €70.6 million, and the company is lagging its H1 2023 acquisition sum by around €25 million. This goes to show the cyclicality of finding good deals. We might expect to see a ramp-up in acquisition activity for H2’24. Time will show, and time is the magic in these wonderful compounders.

For the best summary and knowledge on anything Constellation Software, look no further than to The Compounding Tortoise:

O'Reilly Auto Parts

My portfolios largest holding, O'Reilly Auto Parts, reported earnings of $24.07. The initial reaction on the report was a 4% sell-down in the after-hours market. However, overnight, the sentiment shifted as analysts acknowledged the fact that H2 is bound to see accelerated growth and that, despite minimal misses to estimates, O'Reilly continues to gain market share. We can also see that the mix of DIY and Professional Services are flat, and that DIY seems to be trending downward.

")

My favourite part with O'Reilly is how they are able to combine strong growth with disciplined share buybacks.

ORLY continues to execute it’s buyback program diligently, deploying most of H1 buyback capital at the lowest possible price to ensure the highest possible return to it’s investors. Great stuff!

Two good write-ups on Q2 results:

How O'Reilly gains market share and maintains it’s strong position, by Seeking Alpha author Tomas Riba.

Kinsale Capital Group

Kinsale reported a very strong second quarter.

EPS of $3.75, a 27.2% increase YoY (beat by $0.20)

Revenue of $384.55M +30.0% YoY (beat by $10.77M.

Gross written premiums increased by 20.9% to $529.8 million compared to the second quarter of 2023

Net investment income increased by 48.3% YoY to $35.8 million.

Underwriting income was $76.1 million in the second quarter of 2024, resulting in a combined ratio of 77.7%.

I’ll let my man, Mike Kehoe, tell it like it is:

"We are pleased with our second quarter results highlighted by continued growth and strong margins. Delivering long-term value for stockholders remains our focus as we leverage underwriting and technological competitive advantages and our low-cost model to profitably grow market share”

MercadoLibre

Let’s end this Q2 review on a high note. What a company MercadoLibre is, and they showed great strength again this quarter.

MeLi smashed the estimates for Q2:

10.48 EPS (25% beat on estimated EPS of 8.34)

Revenue BLN $5.07 (8.33% beat on estimated BLN $4.68)

YoY bottom line growth at 103%

Gross merchandise volume is up 83% YoY.

Impressive quarter by an impressive company. My only regret is having to little MercadoLibre in my portfolio. As

says they doubled profits and accelerated growth at the same time.

In other portfolio news

There’s been a couple of non-reporting events happening in my portfolio companies this past month.

Norbit officially reported the customer who put in a substantial order (€160 million) for OBUs on July 29.. The customer is Toll4Europe, which works with companies like Shell, T-Mobile and Daimler trucks (amongst others) and describes themselves as “leading in EET and providing fully integrated cross-border solutions for transport in the EU”. It's good to see a name, and the deal also involves working with Toll4Europe to improve Norbit’s OBUs and make them even better for Toll4Europe, as well as attract new customers.

SanLorenzo bought the company Nautor Swan (01.08). Nautor Swan is a leading maker of high-end sailing boats, making this an attractive and expansive addition to the SanLorenzo brand. Swan will probably continue as a satellite for SanLorenzo, and it seems like a good way for SL to deploy some of the cash that has been gathering dust on the balance sheet.

However, the deal was made not only in cash but also in issuing new stock. 1/3 of the deal will be settled in SanLorenzo stock at a higher multiple than SLs current multiple. This is probably a result of SanLorenzo stock being very cheap at the moment, valued as a typical industrial shipwright rather than a luxury brand in a highly attractive niche. This multiple discrepancy might give the impression that it’s a bad deal, but it looks to be a great strategic decision.

This should allow SanLorenzo to retain all the earnings from the purchase of Swan from the get-go, and seems like the most agile way to create shareholder value. An added bonus is that the highly concentrated ownership structure of SanLorenzo gets less concentrated as the former owners of Swan (Sawa S.r.l.) get substantial ownership in SL and reinvest in the company. This should lead to Sawas ownership land at around 2.1% based on 9x EBITDA of SWANs results. They also keep Swans sellers on board and create strong cross-selling opportunities for the company going forward.

This seems like a very interesting step forward for SanLorenzo, strengthening my impression of the company working towards becoming a nautical luxury power-house.

What I’ve read and listened to this month

As I’ve already shared many articles, I want to keep it simple and recommend two very good reads for the compound-minded investor:

Seeking Winners continues to write very good stuff on important matters and is an investor to follow, in my opinion. Soak up all you can learn from the highest-quality newsletter that is still free!

My podcast tips from the past month

A fascinating talk with a great investor in a private fund that has achieved strong returns while holding the best companies over time:

Rochon is an inspiration to myself, and this conversation is a proper treat.

As Visa is my freshest addition to the portfolio, I can’t avoid recommending this absolute marvel of a podcast on one of the most fascinating business stories out there:

And one video with a great lecture that is worth watching (yes, I am a Howard Marks fanboy):

Nothing I’ve written in this article should be understood or interpreted as investment advice. I’m a simple hobby investor who likes writing, and I am not competent or qualified to be giving investment advice. Do your own research, be critical of my assumptions and look into the companies discussed before making any investing decisions.

Thanks for highlighting the MELI report

Great piece, thanks for the mention(s)! Well-balanced portfolio that should take you to the "Promised Land" ;-)