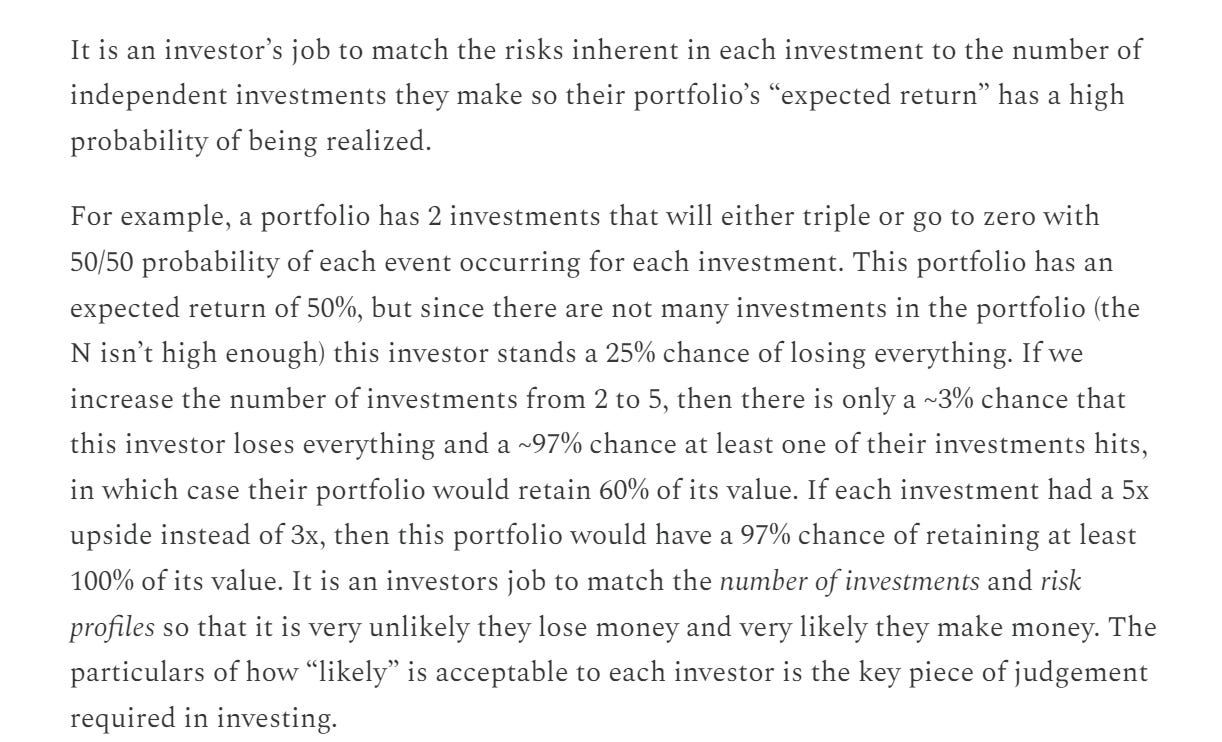

Risk and diversification - how many are enough?

Risk and diversification - how many are enough?

How to think about risk in a concentrated portfolio.

Thank you to everyone who has subscribed to Learning to grow so far! It's motivating to see that many are interested in joining the growth journey.

Today's substack post will address the following topics:

Risk and diversification in a concentrated portfolio

Overlapping risks

Company and risk comparison: Protector Insurance and Kinsale Capital Group

Risk and diversification

Central to any portfolio is facilitating good diversification that takes into account the inherent risks of our company composition, and an overall risk profile that enables you as an investor to achieve the desired return.

A classic method of risk management is diversification. In simple terms, putting your eggs in several baskets reduces the chance that when shit hits the fan, you'll feel less pain and not lose all your hard-earned money.

For investors, the conclusion is often that a portfolio will be less exposed to risk if you own many different shares, in different markets and sectors. The best example of the benefits of diversification is index funds.

But, how many companies are enough? Thomas Nielsen, a fund manager I have a lot of respect for, has written a good post about just how many companies an investor should own to benefit from the diversification effect. Let's jump straight to the conclusion:

After 15 companies in a portfolio, the effect of diversification starts to dilute. Read Thomas' full post here (article in Norwegian).

My own goal is to have a concentrated portfolio of good companies. My guiding star in the investment world is: KISS. Keep it simple, stupid.

In order to deliver good returns over time as a retail investor with limited time, I am completely dependent on leveraging what I learn and my time spent researching being able to generate returns. Therefore, my attention and knowledge will be diluted if I have to spend time getting to know 20-40 companies well, rather than deeply understanding around 9 to 15 companies. I need to keep it simple and a concentrated portfolio will allow me to know the companies I co-own deeply.

But how do I manage to avoid too much risk with a concentrated portfolio? I think it's possible to do so by staying focused and aiming for reducing the overlapping risk in the portfolio. Having as little risk overlap as possible combined with my investment pillars will hopefully help me achieve my expected return.

On the surface, it's a pretty simple equation: Good companies led by talented people delivering on realistically high growth targets, combined with my basket of companies sharing as few risks as possible.

What are overlapping risks?

The idea I'm going to discuss now popped up in a podcast episode from Speedwell research on The Investment Matching Principle. The podcast and The Synopsis substack are a fantastic opportunity to learn about investments and quality companies, which I highly recommend.

Let’s return to what I actually was writing about: Overlapping risks.

Overlapping risks means that different companies can have similar risks. These risks can be very obvious, e.g. how the two Norwegian oil and gass producers, Aker BP and Equinor both are exposed to fluctuations in oil and gas prices. There are also less obvious risk overlaps, such as the fact that delivery and production delays created large inventories for both ultrasound technology company Medistim and fitness and outdoor chain XXL. The same event has negatively impacted the performance of both these companies in very different sectors.

In other words, if I were invested in both XXL and Medistim, and expected risk diversification by owning different companies in different sectors, the same negative event would still hit both companies and negatively impact my returns.

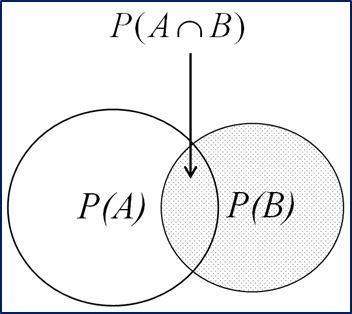

Overlapping risk can be illustrated like this:

If the chance of one of risks A and B happening is 5%, then there is only a 0.25% chance of both risks happening at the same time. The lesson from this is that as long as you manage to spread your risks across independent factors, your portfolio will be robust. If you have several independent risks with a relatively low probability of occurrence, you will have a good chance that single negative events will weigh to heavily on your returns.

Unfortunately, in the world of finance and investment, it is difficult to choose companies with completely independent risk factors. All companies are affected by interest rates, inflation, salary developments and regulations (etc.). Another risk is also the general market pricing, which can negatively affect expected returns during periods of high expectations (also known as cycles). And most importantly, no one can know what the future holds.

It's not possible to find X number of companies in a portfolio that gives a perfect spread of risk. There is no recipe other than thorough risk analysis of the companies you own and strict control of your portfolio's risk profile.

It's important to pay attention to which risk factors the companies in your portfolio share. The more shared risk factors, the greater the effect unforeseen events will have on your total return.

Speedwell provides an illustration using probability theory:

But why not just own enough companies to spread the risk well?

Because a larger number of companies in a portfolio does not automatically lead to less overlapping risk.

One example of how the number of companies in a portfolio does not necessarily mean good risk diversification is the Norwegian stock exchange. Our domestic index is dominated by companies with what I would call overlapping risk profiles. The Norwegian index is crammed full of oil and gas companies, a number of cyclical materials companies exposed to fluctuations in energy prices, the financial sector that derives the lion's share of its earnings from oil and gas, the service sector for oil and gas, etc. etc.

It is easy to think that you are well diversified when you buy an index, but owning a Norwegian index for the sake of diversification exposes you to a highly overlapping risk profile, as the main risk for the majority of Norwegian companies is fluctuations in oil and gas prices.

This is an exaggerated example, but in my opinion a good illustration of the fact that it is not enough to simply choose enough companies to achieve risk diversification.

The relevance for portfolio building

But what does this really have to do with Protector Insurance, you might be thinking. As I mentioned in the introduction, I'm unsure of Protector Forsikring's position in my portfolio, even though it's one of my best investments so far.

I currently own two insurance companies: Protector Forsikring and Kinsale Capital Group. These are positioned in different geographies, and with different business models. Before I go any further, I would like to give an introduction to the companies.

If you find the insurance industry confusing and are unsure of how investment companies make money, click here.

Protector Forsikring

Protector Forsikring is an international insurance company based in Norway. It is listed on the Oslo Stock Exchange and has been a phenomenal compounder for its shareholders since listing, but especially since 2020. They define themselves as a challenger company that aims to be a cost leader in its segments. Protector's main segments are construction and vehicles, and they specialise in customers from the public sector.

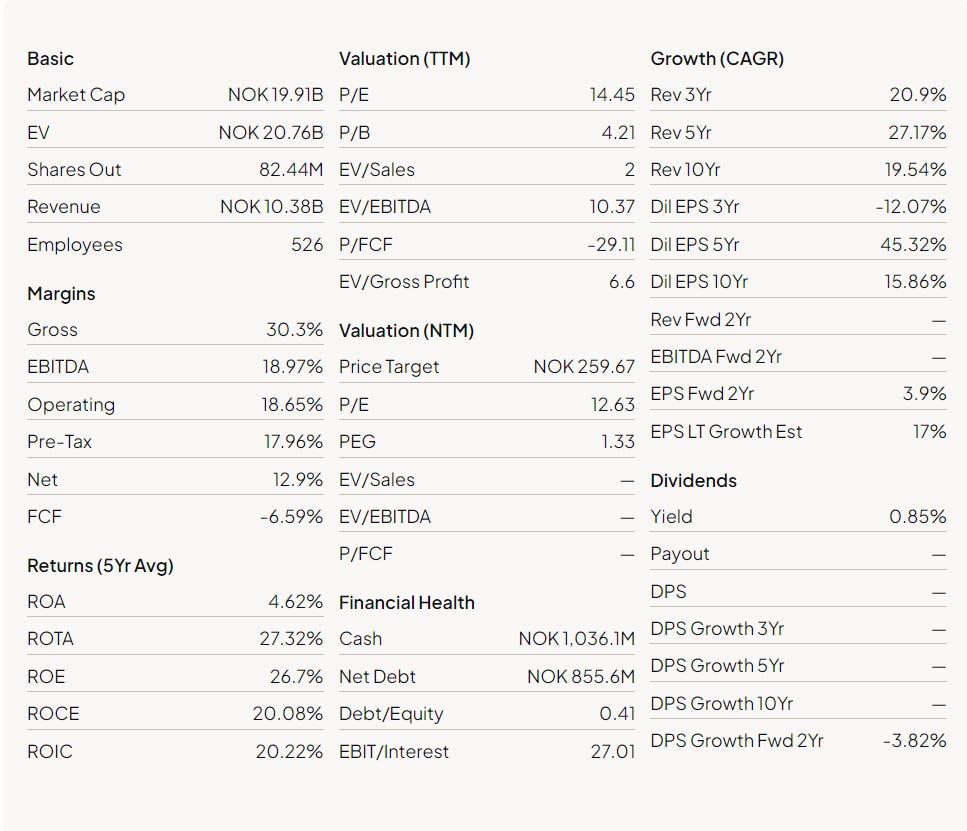

As I mentioned in the introduction post, I have five investment pillars. How does Protector score on these? (Key figures for the company from Finchat.io)

High reinvestment capacity: 5 years average ROCE: 20% ✅

Competitive advantages visible through higher margins than competitors: Gross Margin: 30.3% ✅ & Operating Margin ~18.6% ✅ (Well illustrated by having double the OM of GJF's ~9%.)

Growth ability: 5 year average: Revenue growth: 27.17% and 45.3% EPS - NOPAT CAGR last 4 years of 26. ✅

Skilled management that works for the shareholders: High ownership among insiders (largest owner is the chairman), management has share incentives that are spread over 5 years, and operational senior management with long experience in Protector. ✅

Low or no debt: Debt/Equity: 0.41, and a larger cash balance than debt. ✅

Protector Insurance has grown EPS by 20% annually since 2015, giving investors an annualised return of ~37% since 2015. They are priced at around 12 FWD P/E if we give a conservative growth estimate of around 10% for FY2024 (worth noting that this is a halving of EPS growth from the 10-year average). This is cheaper than the FWD P/E for both Storebrand (~14) and Gjensidige (~18) - the two leading Norwegian insurance companies.

Protector has delivered strong combined ratio figures over a long period of time, and turned the ship around properly after the difficult years in 2018 and 2019.

Protector Forsikring has been one of the Oslo Stock Exchange's absolute best investments over the past 5 years, and I believe they are well positioned to continue to deliver strong returns to their investors.

The company continues to win customers, and show good cost and loss control. Protector was started as a company that would challenge the large and established companies through better use of technology, efficiency and good relationships with their insurance brokers and customers. They have largely succeeded in this.

Given that this is not a deep dive of the company, I recommend readers to review some presentations from capital markets days and annual reports. I've also included an interview with the former CEO and one of the founders of Protector Forsikring at the bottom of the newsletter.

Kinsale Capital Group

My second insurance company is the American company Kinsale Capital Group. They operate in the Excess & Surplus (E&S) segment, which in short is a segment of customers with risk profiles that traditional insurance companies will not offer insurance to. Kinsale has increased EPS by 50.2% annually since 2019 (yes, you read that right) and is priced at LTM P/E 24.9. That's a high valuation, but actually the lowest the company has been priced at since 2016.

E&S is an insurance segment that has experienced strong growth over the past five years, and Kinsale has managed to deliver growth stronger than their market. Growth is expected to slow somewhat in the future, so one should not expect the same history from Kinsale for a long period to come. At the same time, last quarter Kinsale showed an annual growth of 76.7% in EPS.

It's important to emphasise that although Kinsale sells insurance to customers other insurance companies won't or can't sell to, this doesn't mean that their customers are exclusively into extreme sports or building houses in forest fire zones.

The E&S segment exists because, within current regulations, ordinary insurance companies are unable to write policies that take risk assessments into account, or because customers' needs are in niches that are too small for major players to make money from.

Examples include window cleaners who work on the fronts of high-rise buildings, or home insurance in the state of Florida, which is increasingly becoming an E&S segment due to frequent extreme weather. We could almost say that Kinsale is a quirky way to monetise climate change.

Want to understand Kinsale Capital Group better? I highly recommend this deep-dive article from Fundasy Investor.

Given that I've been discussing risk and risk management, it's fitting to highlight a company that has a business model based on being best-in-class at managing risk. To make money in E&S, you need to be disciplined and experienced to avoid making big mistakes. Kinsale is a shining example of risk management.

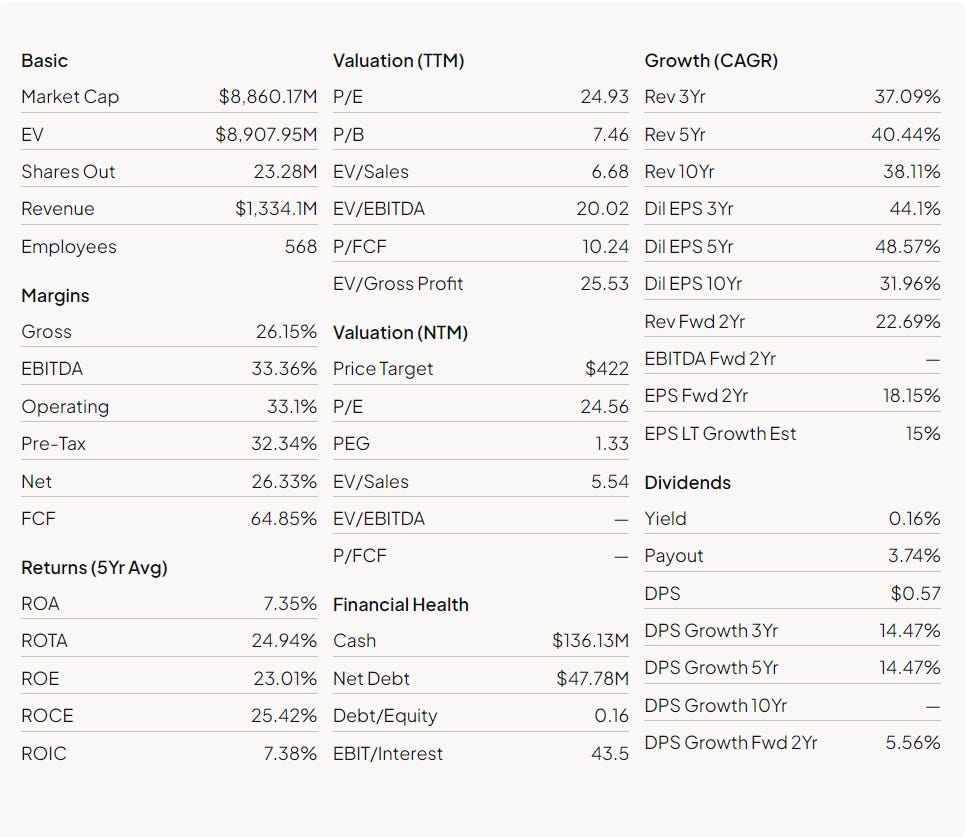

It's fair to hold Kinsale to the same standards as Protector as they are both smaller insurance challengers carving out growth in niches by outcompeting larger legacy players. Let's see how Kinsale scores (Key figures for the company from Finchat.io)

High reinvestment ability: 5yr average ROCE: 25.42% ✅

Competitive advantages visible through higher margins than competitors: Gross Margin: 26.15% ✅ & Operating Margin 33.1% ✅ (this is far better than Kinsale's main E&S competitors who have somewhere between 5-15% operating margin)

Growth ability: 5yr average: Revenue growth: 40.44% and 48.57 EPS - NOPAT CAGR last 5 years of 38% ✅

Skilled management that works for the shareholders: The company is entrepreneurial driven by a skilled management team with over 30 years in the E&S industry. The CEO owns 4% of the company and has his entire fortune in the company and can be considered to have aligned interests with the shareholders despite somewhat low inside ownership. ✅

Low or no debt: Debt/Equity: 0.16, and more cash than debt on the books. Very good balance sheet. ✅

The insurance industry has some other parameters that are important to monitor in addition to those mentioned above. In particular, the combined ratio (CR) and loss ratio are important for specialist insurers like Kinsale, and a deterioration in the loss ratio should be the first thing Kinsale shareholders look for in quarterly and annual reports.

Kinsale's worst CR since listing is on a par with the best results for Protector and similar insurers (Figure 1). The company also delivers consistent, and very strong, loss ratios, again making Kinsale a market leader (Figure 2).

Figure 2:

Kinsale is in a league of its own when it comes to profitability and risk management. This is because E&S insurers are exempt from regulation and are freer to price their premiums than more traditional insurers. This gives Kinsale the ability to calculate and charge higher margins of safety on its policies, creating a more solid foundation than its competitors.

The efficiency of its operations allows Kinsale to offer better pricing and far faster case processing than its competitors. When you mix together that Kinsale is more efficient, has a technological edge, and strong customer relationships compared to its competitors, then you have a winning recipe.

Did you find the company review educational or exciting? If you buy me a cup of coffee, I will be motivated to continue writing company analyses. Flattery always helps!

Risk control

What exactly is the problem, why not be happy that you are invested in two wonderful companies?

That's the question I've asked myself several times. Protector and Kinsale are both well positioned to continue their strong performance. Kinsale operates in a market that is expected to continue to grow strongly (15.2 per cent market growth annually until 2027 (remember that Kinsale has consistently delivered stronger growth than the market)), and Protector is reasonably priced compared to its growth. The company also has ambitions to expand into new markets. Protector highlights good opportunities in a fragmented and inefficient insurance market for public sector players in Europe, and believes there are good opportunities to capture market share.

Where does the risk overlap?

As discussed in this article, it is wise to consider the companies' overlapping risk profiles. Both are insurance companies, and despite geographical and customer diversification, owning both Protector and Kinsale exposes me to a broader field of ‘bad luck’.

Protector took a real beating during their biggest ever crisis related to long tailed silverfish in the Norwegian housing market. This is clearly visible in their financial history (e.g. CR in 2019 was 103%, compared to less than 90% in the last three years).

Investing in the insurance industry also brings with it an overlapping exposure to unforeseen economic shocks. For Kinsale, this is a business advantage as they thrive on being the best insurance specialist. For Protector this is mainly a risk as they are an insurance generalist, and cannot bake in as high margins of safety into their premiums compared to Kinsale. If I had to choose one company, I would choose the one that specialises in extraordinary risk management, namely Kinsale Capital Group.

Ironically, Kinsale, which superficially appears to be exposed to the highest risk, is probably better equipped to deal with unforeseen events.

This brings me back to the question: Does my exposure to Protector and Kinsale give too much weighting to the risks insurers are exposed to?

Kinsale is more heavily exposed to regulation, catastrophes and competition, while Protector's main risk factors are weaker markets (especially among public sector customers), unsuccessful expansion, weaker investment performance and, of course, unforeseen events and competition (especially in the UK, but Protector's competitive landscape is more stable than Kinsale's).

Both also lead to a higher weighted exposure to a possible future economic systemic failure, of the portfolio if something were to hit the insurance industry or the equity markets. Should a black swan emerge in the insurance market, the weight of this shock will weigh more heavily on the total return.

My preliminary answer is that thanks to their different geographies, different segments and different business models, there may not be as much risk overlap. There is a significant difference in their customer groups, where Protector is exposed to predictable, large and good public sector customers, while Kinsale is the preferred specialist supplier in its markets.

The conclusion is that both companies are exposed to general insurance company risk, such as unforeseen events and catastrophes. At the same time, I consider the chance to have significant unlikely events in both Protector and Kinsale's markets at the same time to be low.

Update: At the time of writing I was unsure what to do. I ended up selling my position in Protector, prefering the American geography and the specialist position of Kinsale. Another factor for my decision was that Kinsales results were not affected by the ability to investing in stocks or bonds, which is another general overlapping risk.

That’s it for this time! Thank you for reading, and I hope to you can share your feedback if you have any.

Interested in learning more about the companies and concepts I've discussed? Here are all the links and then some:

Longriver Podcast interview with Shree Viswanathan about Kinsale Capital Group, among others.

The article about Kinsale Capital Group from Fundasy Investors Substack.

The Synopsis about overlapping risks etc.

Episode 7 of StockUp about investment choices and criteria, and episode 36 of StockUp about Protector and Gjensidige.

Ep. 17 of Børsbrøl - Thomas Nielsen's conversation with former CEO of Protector Forsikring Sverre Bjerkeli (Interview performed in Norwegian).

Hvaler Invest's website. Here, former CEO of Protector Forsikring, Sverre Bjerkeli occasionally shares his investment rationale.

Warren Buffett's key insights for insurance investors.

Three good Investopedia articles about the insurance industry:

The companies discussed on this Substack should not be construed as investment advice. The content of this article is for entertainment and information purposes only, and the author is not a certified advisor or someone on whom you should base your investment decisions. If you decide to invest, I am not responsible for any decisions you make based on what is written on this Substack. I am and may be exposed to the securities discussed, and therefore have an interest in talking about them. My investments can and will change without me updating this immediately. All investments carry a high level of risk, and in the worst case can break even.

By reading and using this Substack, you as a reader recognise that you are responsible for your own investment decisions and outcomes. The author is not responsible for any choices you make after reading an article on this substack, or the outcome of those choices.

Like all other information on the internet, the newsletter should be read critically. I encourage everyone to investigate multiple sources, and be aware that the writer has biases and possible misconceptions.