The case for quality growth and more pompous reflections on investing

Understanding the mosaic of quality can yield very rewarding returns.

The case for quality growth

I have the simplest of tastes: I only like the best. Oscar Wilde

This remark from Oscar Wilde is something that Francois Rochon often quotes in his investment letters. I share this sentiment. I have a strong belief that there is simply no reason one should invest in anything but the very best companies.

In evolution, capitalism, history, and everywhere we go, the following pattern emerges: The best will over time not only remain the best but often manage to increase their competitive advantage gap. I seek to gain returns on my investments from this pattern. Therefore, an important part of my strategy is to align myself with companies that have already won. Another word for winners in the stock market is quality companies.

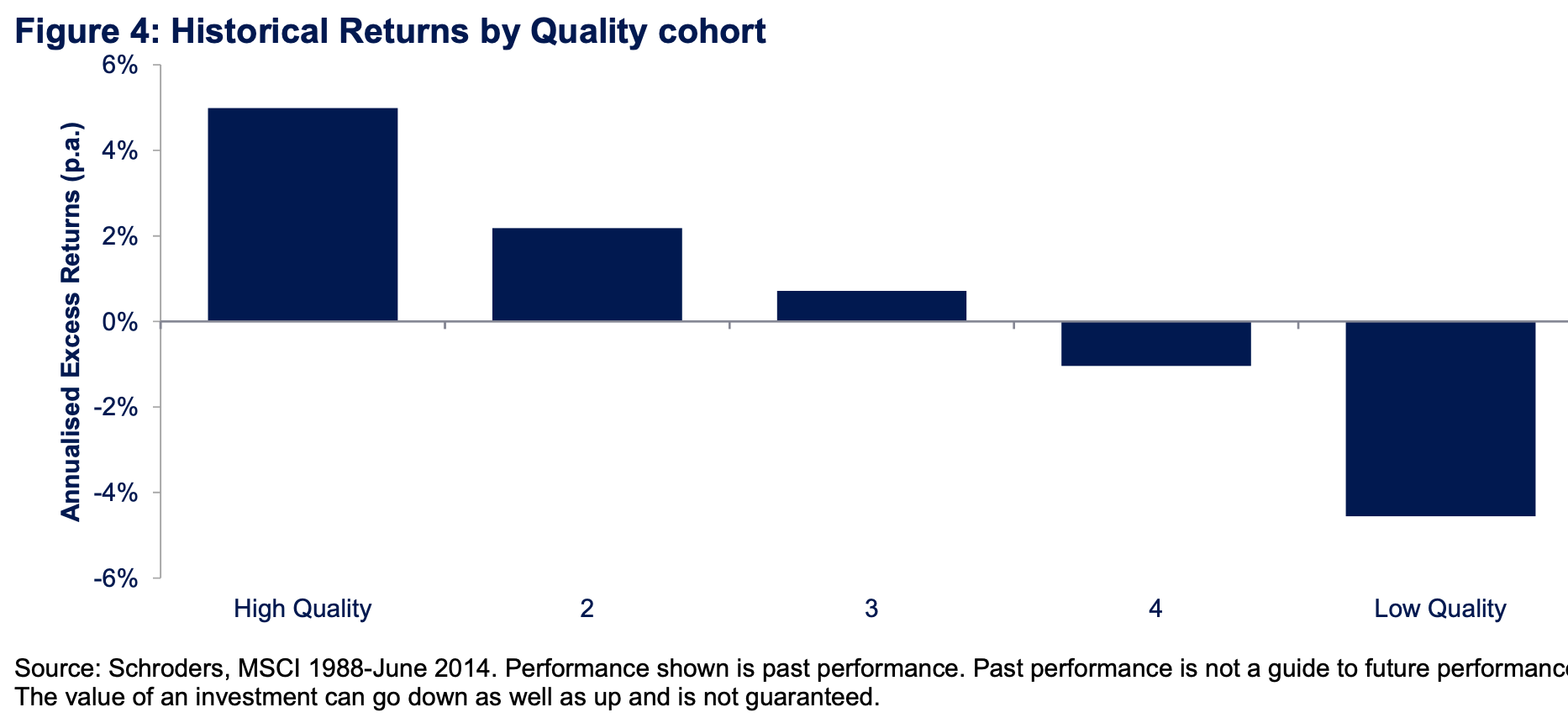

Just look at these two findings from Schroders paper on why quality investing can be like having your cake and eating it to:

There have been volumes on volumes written about quality investing. Quality as a term is a loose and often subjective definition. I believe it has to be subjective, and it is impossible to quantify. My investment pillars of growth in EPS, ability and runway for high returns on reinvestment, great management, and competitive advantages are some of the key ingredients to quality investing.

An important factor for quality investing is that it can’t be based solely on companies historical performances and growth. As investors, we aim to make money from the future returns on growth, not the past. We therefore have to have a deep, rational and most of the time, qualitative understanding of the companies in which we are co-owners. It is never enough to simply look at a company that has won and dug it’s moat, we need to understand how it will continue fortifying it’s moat and stay ahead of competition.

Conceptually, I think of quality as a mosaic. There’s many different-sized pieces that, if you look closely, seem entirely unrelated. They are angled differently, have many different colors, and studied to intently might seem like random ordering of things. But when we take a step back, we see the whole picture and realize each piece is an essential part of the picture.

In investing, I enjoy the definition of quality from Schroders research on quality investing (I’ve highlighted my favourite parts of this definition):

Quality companies are defined by higher profitability with a record of stable business performance over time and have the financial strength to be able to invest for the long term. The best performing quality stocks are also those that have good track records of returning surplus cashflows to shareholders. More specifically, we capture Quality with the following three key characteristics:

Profitability – Rates of returns, particularly return on equity, cash flow generation and the margins of the business, which measure the ability of the company to generate profits from its assets.

Stability – Whilst profitability is a significant driver of relative stock returns over time it can be enhanced by focusing upon companies with more stable fundamentals. We analyse the growth of dividends, stability of cash flows, earnings and sales over time which helps to avoid temporarily cyclically strong companies which may easily be mistaken for sustainable growth.

Financial Strength – Whilst some debt is fine, it is also important to distinguish between those companies that are expanding via excessive financial leverage. Companies with modest leverage and ample ability to service that debt are more likely to be masters of their own destiny. Thus Quality companies have appropriate leverage given the investment cycle, cyclicality of cash flows and opportunities to invest in high returning investments.

As Schroders research tells us, quality is about companies controlling their own destiny, that have achieved stability in their fundamentals and are able to generate better profits from their assets than their competition.

That is why one thing I look for in my investment is companies that are active in industries with a field of inferior competitors. I believe that there are great returns to gain from staying invested in companies that have higher ROICs and EPS growth than the rest of their direct competitors. Companies that are head and shoulders above their competition are likely to remain positioned for growth and capture market share. This is one place where we as investors can gain outsized returns from the general market.

It’s important to take into account research on what drives shareholder returns. I want to highlight three papers:

Michael Mauboussin research on general market returns: It is important to understand corporate demographics.

Henrik Bessembinders research on wealth creation in the U.S. markets.

Boston Consulting Groups report on shareholder returns in a turbulent time period.

These papers all point to some evidence backed findings:

There are few true winners.

Most shareholder returns come from a handful of companies.

The ingredients of investment returns are highly affected by holding times: Over a longer period of time, fundamentals matter more and price less (and vice versa over a shorter period of time).

To be able to earn money on these insights, my goal is to try to find companies by looking at boring, consolidated, or consolidating industries that are not changing as rapidly. There are plenty of quality companies out there, but I aim to invest in places where the spotlight does not shine so brightly.

Why is that? Well, I prefer to be invested in the biggest fish in smaller ponds. There are a couple of reasons for that:

Less media and headline attention allows management to spend their time focusing on long-term shareholder value creation.

The available edge to investors in many of these is to remain long-term minded. We only have to look at shares traded intraday to understand that very few investors reap the 12-20% yearly returns on companies such as Constellation, Visa, and O'Reilly over long periods of time.

I strongly believe that it is the companies, organisations, and individuals who are motivated by achieving fundamental results and not public lauding that creates outperformance over time.

Also, companies in more consolidated or more niche segments of the market face less competition. There are fewer players trying to outcompete the autopart retailer or the high-end pursemaker than the grocery stores or yoga pants makers out there. Why? Because it is human nature to seek validation, fame, and headline coverage. I prefer the factors of boring, unknown, and repeatably better.

This means that I stay away from fast-moving industries or companies. Everybody wants high and fast returns and often seeks high and fast growth. This leads people into three stories:

Hyper-growth and the next big thing.

Turn-around stories where a bad position will allow for a great recovery.

Straight-out scams.

I think the most important thing we as investors can do to enjoy long-term success is to avoid these things.

My goal as an investor is to enable myself to stay invested over a long period of time so that I can leverage the power of quality growth compounding. To enable myself to stay invested, and work for myself, I try to avoid comparing myself to indexes and other investors. My goal is to compound at around 12-15% a year. It might not sound like much, but over long periods of time, this is a lofty goal. I hope to achieve it, but I doubt I will, and I know I won’t every year. That must be OK. Because I can’t know what year I will underperform or overperform. All I can do is stay invested in great companies at rational prices.

The case for stability and predictability

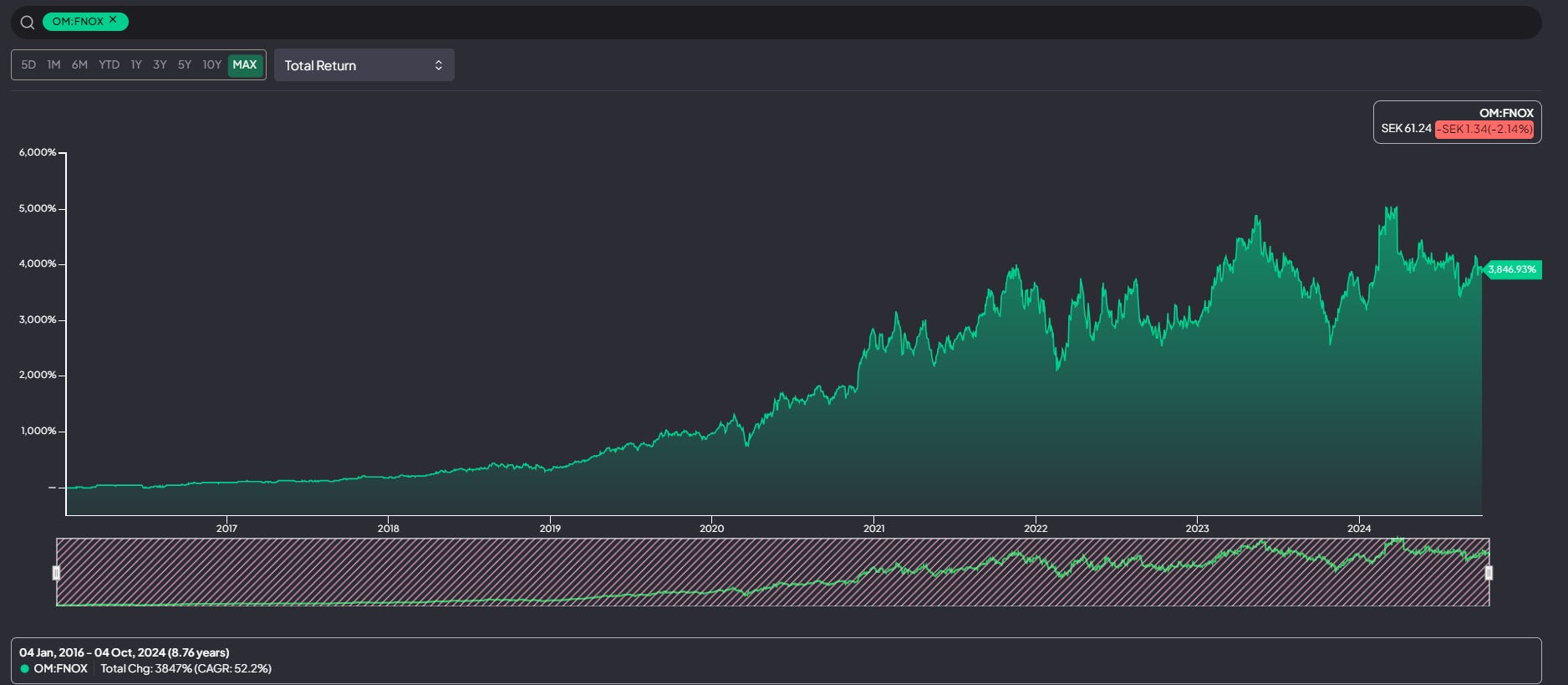

A couple of terms I want to spend some time discussing is predictability and stability. As investors, it’s easy to pull up charts of great performers such as Microsoft, Fortnox AB, Nvidia and Vitec AB. Just look at Fortnox’s total return since IPO:

We can all pull up charts to see how a company has done historically. We can study return profiles and historical fundamentals and say, “These traits made this compounder, I need to look for similar companies.”. It is not necessarily the wrong approach.

But we need to avoid taking to many shortcuts. Our goal as investors is earning money on future growth and reinvestment. The past does not necessarily repeat itself.

Therefore, we have to understand the drivers of historical returns, and evaluate whether we find it probable that it will repeat itself.

As outlined by the Schroders report and many other research findings, the strong usually get stronger. But in fast-moving sectors with many moving parts (i.e., uncertainties) it is hard to understand the full picture. The younger an industry is, the more new challengers exist, and the faster the innovation in the sector is going, the harder it is to understand the history, and predict the future.

We can never know what the future holds. As investors, all our crystal balls are as bad as everyone elses. But we can position ourselves in companies and sectors that are not exposed to the rapid tumbles of the future. The needs of a rich person who wants to buy a yacht are probably not that far away from what they were a hundred years ago. The wants of auto-repair shops to have easy and rapid access to the parts they need to do to get the job done stay the same tomorrow as today. The ability to produce complex parts for the electrical industry better and more reliably will continue to be rewarded in 2030, as it is being rewarded in 2024.

But how AI will develop in the near future is not easy to know and doubly difficult to get right; how the need for accountant software will develop in Sweden is hard to predict; and what the training equipment people want to spend money on is subject to short-term popularity swings.

By positioning myself in boring, slow-changing industries with a few dominant players, I seek to compound my investments through proven, profitable, and probable companies.

We cannot know the future. I avoid making bold assumptions about future earnings, and I avoid having to much confidence about who is going to win a race with many fast-driving cars.

I like to look to for companies that have shown stable and better than average growth in key metrics such as NOPAT, EPS, and FCF generation. It’s important to not obsess to much about the bottom line: A high FCF yield is often seen as a positive, but it might also signal that the company has few options for reinvestment. That is not good, in my opinion. True outsized returns come from companies with plenty of good reinvestment opportunities at high ROIICs.

I also think there’s a case to look for margin and growth stability. If there are high fluctuations with a company growing NOPAT at 0% one year, and then 20% the next, it suggest a cyclicality and instability of true control over growth. I much rather want a company growing it’s NOPAT at 8-10% a year every year for decades.

Dullness and frugality are competitive advantages

I believe that boring companies that are frugal and conservative have competitive advantages. They tend to try to find margins to squeeze, synergies that make their business run better, they save cash for troubling times and they stay focused on what matters for their companies.

Staying focused on what matters does not necessarily mean an obsessiveness of one particular product. For Amazon, it has always been intensely focused on customer experiences; for Hermes, it has been to take quality and leatherworking to the greatest extent possible; and for a company like Norbit, it is about trying to solve the toughest problems out there in their niches.

If you are occupied with appearing flashy, having sleek investor pages, talking to your peers in conferences, flying first class, and so on, you are not spending time running your business. I do not judge anyone seeking to build networks, present well-sorted information and travel comfortably. But I remain sceptical to these sorts of practices in companies. Ultimately, dullness and frugality are about respect for investors and the business.

As Warren Buffett put it:

Absence of change is how you get rich in investing.

Change is exciting. Predictability, stability and slow-and-steady growth is boring. That is what I want.

Be mindful of dilution and comparisons.

There are plenty of OK, good and almost great companies out there. They do not interest me. I want to invest in the market leaders of niche and slow-moving industries.

But there are also plenty of great companies out there. Fastenal, Games Workshop, and LVMH are all great companies. But they are not in my portfolio. Why?

It’s a mix of several factors: Pricing of the companies compared to historical multiples, sentiment signaling it’s probably not pessimistically priced, but most importantly: They don’t contribute to reducing the risk of the portfolio, and they don’t increase or secure my expected return profile by a lot. Why own LVMH and Hermes when Hermes moves in tandem with LVMH upwards, but falls less and more seldomly? I don’t see why I would want to dilute my potential positive outcome and add just as much overlapping risk.

Now, at times this strategy is bound to underperform. Looking to often at other investors or indexes when they are roaring upwards might make you unhappy and tempt you into changing your portfolio in a year of relative underperformance. This should be avoided as much as possible. Remember, the edge is being able to stay invested with quality growers over long periods of time.

Summary

Let’s try to summarize how I think about quality growth investing. For me, it’s about the old saying: Slow and steady wins the race.

I try to combine quantitative factors such as historically good and stable earnings growth and pricing power (margins) with a qualitative understanding of the companies’ business model and competitive advantages. I often give more weight to the idea than the numbers.

It’s important to understand success factors for these quality growers. In my opinion, great companies share some important qualitative factors:

Frugality

Trying to solve difficult problems, sharing and creating value for customers

Management focused on improvement and not short-term goals

Honesty and simplicity

Ability to adapt and develop — longevity is no. 1 priority

That’s it for this piece on my pompous series of how I think about investment strategies: Stay tuned for more!

As always, thank you for reading my writings. If you enjoyed this piece, or found some interesting counter-arguments or opposing views, please let me know! That is how we learn.

If you want to give back, please spread the word of my Substack to those you think might be interested. And if you feel especially generous and want to pay back, there are two ways you can do that. You can sign up for a plan on the best investment research site out there, Finchat.io. You get 15% off, I get a cut of the sales. We both win!

Another way is to treat me to a cup of coffee. It’s the fuel of my writing, so any caffeine contribution is greatly appreciated.

And, nothing I wrote here should be understood as investment advice. This is written purely for entertainment, and I am in no way a trained expert suitable to give advice. Do your own research. I hold shares in several of the companies mentioned.

Great article. As I also own Norbit, I will turn to this deep dive now! Thanks!