The future - It's electrifying!

Two shallow dives into interesting industrial picks from the industry wonderland of Sweden.

Introduction

Dear readers,

In my last piece I jokingly wrote that I have no respect for my readers and that this is a purely egotistical project. I plan to publish at least two more related pieces to this last article in the coming week or so.

However, I do actually have quite a lot of respect for my readers, and I want to share two interesting companies that I have come across recently. It won’t be the length of my deep dives, but I can hopefully convey some important aspects.

Currently, the market for electrical components and production of these are facing strong macro headwinds. It’s been especially tough in Europe, as the continent is struggling in the face of war, energy shortage (despite lower gas prices) and weaker economies.

Everything is electrified

One theme I have been paying attention to from the sideline is the theme of electrification. There are many segments within this global megatrend, with sectors like EV, renewable energy production, data and cloud storage and of course the expansion of AI capabilities.

For my style of investing, these are all too uncertain and hard to predict. I label a lot of investments into these sectors “The Next Big Thing”. I discussed this a bit in my last piece on my investment strategy, but I simply do not think I have any edge what so ever to be able to predict the winners in fast-moving and growing sectors.

But, electrification is an undeniable trend. To mitigate climate change, we need to invest and develop a metric fuck ton of new technology, infrastructure and expansion into grid, distribution and production of energy. In 2024 we will exceed around 3 trillion USD in energy investments globally (around 2.5% of global GDP) and this number is expected to tick up in various ranges going forward. Projecting a TAM, or predicting the future, is highly complicated and as usual, my crystal ball is as opaque as others in regards to where this market is headed.

Some sources of reading: Tripling renewables by 2030, discussion on challenges faced by the US in grid renewal, global renewable outlook.

This becomes doubly complicated by the fact that investment into renewables is currently in a lull after a bubble and sentiment pop that happened in 2021. Add on that national economies are struggling to meet the demand for defense investments thanks to the aggression of the Russians in Ukraine, and with less will and ability to invest in future energy yields we have a proper headwind. Even my home country of Norway, at times called the “battery of Europe”, is set to face energy struggles.

The above discussion only centers on electrification in regards to renewable energy production. Let’s remember there are several streams building into the rapid river of the megatrend I call Electrification. So how do I think about playing this development?

I have previously discussed how much I like niches and network effects. I believe small value adders with a relentless focus on quality to be the companies I want to align with as a shareholder. I think I have found two well positioned in the middle of the electrification trend. Both are catering to complicated needs and hard tasks, and are performing very well.

AQ Group

AQ Group is a global manufacturer of components and systems for customers with high demand. They operate within the electrical manufactoring services sector and have a twofold strategy for growth:

Organic growth through taking on larger and more complicated orders from existing and new customers.

Growth through acquiring factories that they stand to either achieve synergy effects or that they are capable of improving efficiency.

As many of their comparable peers have issued profit warnings in the last weeks (1, 2) AQ Groups shares have tumbled. This was followed up by SEB, who issued an update of their analysis, saying they expected AQ to have a tough Q3 and H2 the shares stumbled down a couple more metaphorical steps. The aforementioned headwind is blowing strong.

Now, I want to give a brief overview of my investment thesis for AQ Group and why I believe there is value to gain from picking up shares in this tumultuous period.

What I like

AQ is a quality company

As shown in their investor presentation slide, AQ Group has an excellent track record of posting profits in every quarter for the last 30 years. They also show great historical growth in EPS. Compared to their peers, I find AQ Group to be in the elite class, if not the very best there is.

As we can observe from the above charts, they have shown a remarkable ability to grow NOPAT at 19% CAGR for the last 10 years. Their gross profit margins are actually improving for the third year in a row, and as I’ll show in a second, they have been able to mitigate some bad organic growth with excellent margin improvement.

The cherry on top in regards to AQ Group is how they have prioritised reducing their debt levels. AQ Groups CEO, James Ahrgren, is refreshingly candid and sober in his market evaluation. This is reflected in the company’s excellent balance sheet. They obviously listened to the weather forecast and prepared for the rising headwinds.

2024 so far has been worse than ‘23 and ‘22. The last two years have been some glorious days for the EMS producers and AQ has thrived. They’ve had several years with achieving results far above their targeted 15% annual growth.

A comment on the organic growth: -6% is not good, but if we adjust for the loss businesses of battery production, we end up at -2%. Still not good, but within normalcy for a company in a cyclical sector coming out of a high growth period.

When it comes to margins, the company has shown an ability to consistently outperform their goal of an EBT margin of 8%, and they have managed to achieve outperformance in 8 out of 14 quarters since 2021. Ahrgren commented on the longevity of these margins over, but would not say that they were looking to raise margin goals or if these were the new normal levels.

To wrap up a short diagnosis of the current conditions of AQ Groups ability to face the worsening macro conditions:

Reduced debt level.

Cost control is visible through margin improvements.

Some one-offs is making it look worse than it is.

I believe this is presenting an opportunity for the long-term minded investor.

AQ is positioned in industries with secular growth trends

As mentioned, the world is going to need a lot of parts for electrification. We have explicit goals and needs to make transportation, data storage, energy production, construction more modern and efficient.

Now, why AQ Group, and not many of the other EMS industrials? I believe the company has a couple of strengths that others lack:

They intentionally try to aim at hard-to-make products.

They want to work with demanding customers in complicated technologies.

They have a relentless focus on quality and on-time delivery - their goal is to be the best.

Why is this important to me? Well, as Ahrgren likes to point out: AQ Group does not have any proprietary products. It’s not their products or technology that gets customers shopping with AQ, it’s how they execute and meet customer demand. As they deliver parts that are complex and hard to make, they are often the most important parts of the full construction, and these need to work for the truck, railroad, or solar panel to work. The cost of parts that AQ produce are also relatively miniscule compared to their importance.

Therefore, AQs customers are more interested in the quality than the price. In addition to this, to complete and get their electronics up and running, they need the parts delivered on time (OTD). Currently AQ achieves a 92% OTD, but if you listened to Ahrgren, you would think it was below 50% with the disappointment he is expressing in the quarterly calls. Gotta love the drive.

In sectors where you are providing customers with non-proprietary products, making life easier for customers is often where the real money is. AQ Group has a relentless focus on their customers satisfaction, and this is where the real moat is. After a while, their timely, high quality deliveries become integrated and essential parts of their customer companies daily operation which creates strong and lasting relations that customers probably value very highly. This is in my theory, what allows AQ Group to perform better and more resiliently in a cyclical sector.

Aligned management with high integrity and their heads in the right place

This is probably my favourite part of AQ Group. I have mentioned CEO James Ahrgren quite a bit, but it’s time to introduce the founders: Per-Olof Andersson and Claes Mellgren. Read more about the board members of AQ Group here, and management here.

Andersson and Mellgren founded AQ Group in 1994, and they’ve been highlighted as some of the best entrepreneurs in Sweden (which is quite a tough place to compete for that title in). Andersson and Mellgren are both core owners of AQ Group, and they both are still active with the company through the board where Andersson is chairman. Andersson has a stake of 19.45% and Mellgren 19.7%, owning around 40% of AQ Group.

Ahrgren himself only owns 64,000 shares in AQ Group, which is a low total share count, but could very well be a considerable part of his net worth.

What is important is, however, not how many shares the different key people hold — but how they are leading the company and what they are focusing on.

Here’s an interesting discussion on this topic:

This brings me to my favourite part of AQ Group: their culture, structure, and organisation. I’m sure Andersson and Mellgren are the ones who implemented this. But it seems to me that AQ has a strong focus on their core values of reliability, customer focus, simplicity, entrepreneurial business, cost efficiency. As a global company that practices an entrepreneurial spirit they value decentralisation and agency highly and encourage their group companies to do what they think is best. They also have a lean headquarter, with a focus of promoting from within.

These are all filled out in more detail in this document, that they share with every employee in the group:

Now of course, just because a company say they need to do X to achieve Y doesn’t mean that all the employees act that way automatically. But management is very focused on eating their own lunch. James Ahrgren recently had an interview with a swedish podcast where he explained that when he’s travelling he always flies economy class, books the cheapest hotel and so on - and he hopes that the example he sets influences the employees of AQ to act the same way and work in line with the core values.

Another thing I greatly appreciate with AQ is that they never give forward looking statements, consistently underpromise and overdeliver and are always open about that they don’t know the future - but they will do everything to achieve their goals. It’s very much a focused management.

What I don’t like

There’s a lot to like about AQ Group, and I could probably go on for quite some time. I, however, have some gripes with the company, which are fewer, but they do hold some weight.

Margins

EMS is a low margin sector. They will never become a high margin, capital light model. I think in AQs case there are good arguments to be made for them navigating this well and adding scale through both their customers organic growth and M&A activity into new niches and factories. But there’s less room for failure, and this is one of the main reasons AQ will never be a large position in my portfolio.

Cyclicality

EMS is highly exposed to their consumer and underlying industry cyclicality. This is something that is out of AQ Groups control. I believe they have taken important steps to integrate into the value chain of their customers and that they offer lean and cost-efficient production. But as we see at the moment, AQ will have a shareprice affected by the world around them to a greater effect than many others. If they time M&A badly, cyclicality can effect them to a greater degree - and shocks such as supply chain issues like we saw with Covid hit AQ quite roughly.

Key personell risk

This is the flip-side of great management. I think that the organisation of AQ Group is bigger and more robust than the three big names (Andersson, Mellgren and Ahrgren) but in the case of either the founders selling some to live more comfortably in their retirement, or future family members doing so, we can see a negative reaction to the share price. This is not a fundamental risk but a volatility risk.

Valuation

I want to do a rough and rowdy attempt at showing some valuation assumptions for AQ Group. As a reminder, I prefer to look backwards to get a concept of what to expect going forward. Here’s a reverse DCF model based on H1’2024:

We see that the market is expecting around 11.2% growth in the first 5 years and 8% growth in year 6–10. Given AQs historical NOPAT growth of close to 19%, I think the market is being to pessimistic with AQs ability to grow their earnings going forward.

Their focus on EPS is also something that I suspect can hide the near-term effects of M&A on their results further down the balance sheet (illustrated by the gap between EPS at 15% CAGR and NOPAT at 19%.)

Let’s try to peak into the future. Here’s a rough and rowdy EPS and P/E assumption going forward:

I assumed same H2 results as H1 results for 2024 to arrive at 7.96 SEK of EPS for the full year. This might prove to be a bit optimistic. As assumptions, I baked in a multiple compression from ~15.5 to ~14.5. I did not see it justified to assume a substantial compression, and a 14.5 P/E would have AQ slightly over the current pricings of competitors such as Kitron and Note who are somewhere between 13-14 P/E.

All in all, I think AQ Group is currently an attractive investment and have made my library card position into an actual portfolio position. To me, it appears that if the company is to achieve it’s own goals (which it has routinely beaten) over the coming 5 years, I would stand to gain a fair bit of return on my investments made at around 117 SEK. AQ Group currently sits at around 3.9% of my portfolio.

NCAB Group

NCAB Group is a Swedish printed circuit board supplier with a leading position as the nr. 1 (and only) global supplier of this critical component within electrical products.

First, a little bit about PCBs: These circuit boards are the electrical glue of the modern world. There are various segments of the PCB market:

Producers, i.e. PCB factories

Traders, this is (with a twist) where NCAB is positioned, where companies buy from the producers and sell to customers needing PCBs in their products.

The PCB market can further be divided in two:

High-Volume, low mix: These are typical mass produced PCBs for consumer products such as smart phones, computers, TVs et.c.

Low-Volume, High-Mix: These are orders for PCBs designed for complex products, often industrial and/or high tech with a specific niche design. This is where NCAB is positioned.

I like to think of PCBs as one of the core raw materials for the electrification process. These circuit boards are the joints of electrification, and the more complex customer and market you are serving, the higher the quality of the production and design is essential.

NCAB also has a two-sided growth strategy:

Leverage organic growth driven by demand for customers products.

Consolidate a fragmented sector through M&A.

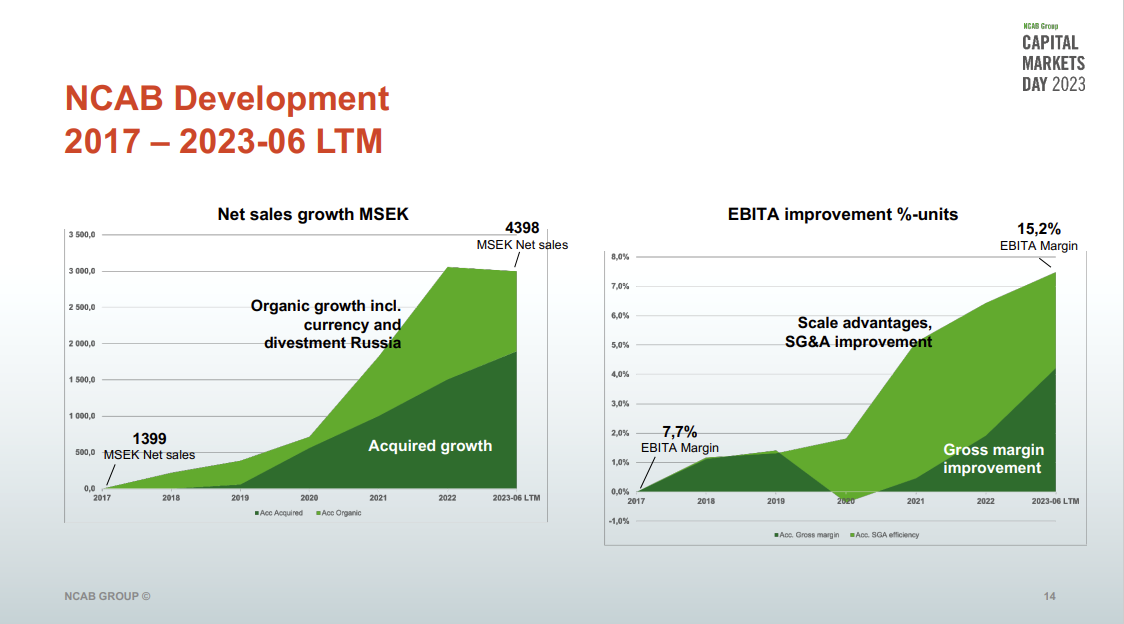

NCAB have shown an impressive ability to grow NOPAT at ~24% the last 10 years, whilst having a FCF margin that is surprisingly robust for an industrial company.

What I like

They operate within a highly rewarding niche

NCAB is, as mentioned, a supplier of PCB for demanding customers. As suppliers, they do not own any factories or production equipment. My first reaction was “Oh, so they’re an expensive middle man?”.

But it turns out thats not their business model. As a supplier to high-demanding, quality conscious smaller producers of electrical stuff, NCAB act as an efficiency broker between niche players in a two-sided network that creates win-win dynamics on both ends.

They work with the buyers of PCB to understand their needs, volumes and so on, and then they have a large network of factories that they then take these customer needs and match them with the best factory for what they want. On the factory side, they assist with the design project, work-flow and act as a guarantor. This gives both the buyer and the producer of the PCBs a bunch of benefits, such as:

Effective selling and buying processes

Scale

Purchasing leverage

Lean processes

NCAB serves a range of high-demand sectors where there are strong needs for low failure rates. The PCB is typically one of the more important parts of the construction, but in the most costly examples, only 2% of the total cost of the equipment.

NCAB is also the only fully global supplier, purely focused on HMLV PCBs. Their strategy is to continue only focusing on PCBs, and a lot of other traders for components tend to sell more than PCBs. I like this focus, and I believe focus is an important part of any great company.

They have constructed an impressive network of cooperations with main factories, and they have positioned themselves with factory management offices in close proximity to their main factories. This allows them to strengthen ties with factories through assistance from their engineers and expert personnel, which further strengthens their integration into customers value chains as they are quick to make needed adjustments and react to things that need to be done differently.

They also have rigid processes to vet and quality screen factories they work with where they go through long screening and spend a lot of time ensuring that the factories can do what they need them to do. They work with factories to ensure safety for personnel, sustainable production, and to ensure maximum factory output.

For their customers, this is a process that would consume far to much of both time, personneland money to do. So when a customer making sophisticated electrical products needs PCBs for their products, they can use NCAB to effectively handle factory follow up and order placements.

Excellent M&A consolidators

NCAB Group have shown an impressive ability to consolidate and add new growth through acquisitions. The dual flywheel of growth that has been so successful for many other companies (especially in Sweden) seems to be very much at play in NCAB as well.

Their M&A strategy is focused on several things:

It’s easier to buy new customers than to win them from competitors.

They see good opportunity for revenue growth, and increased margins.

Scale effects that lead to better profitability.

Improved working capital mechanisms.

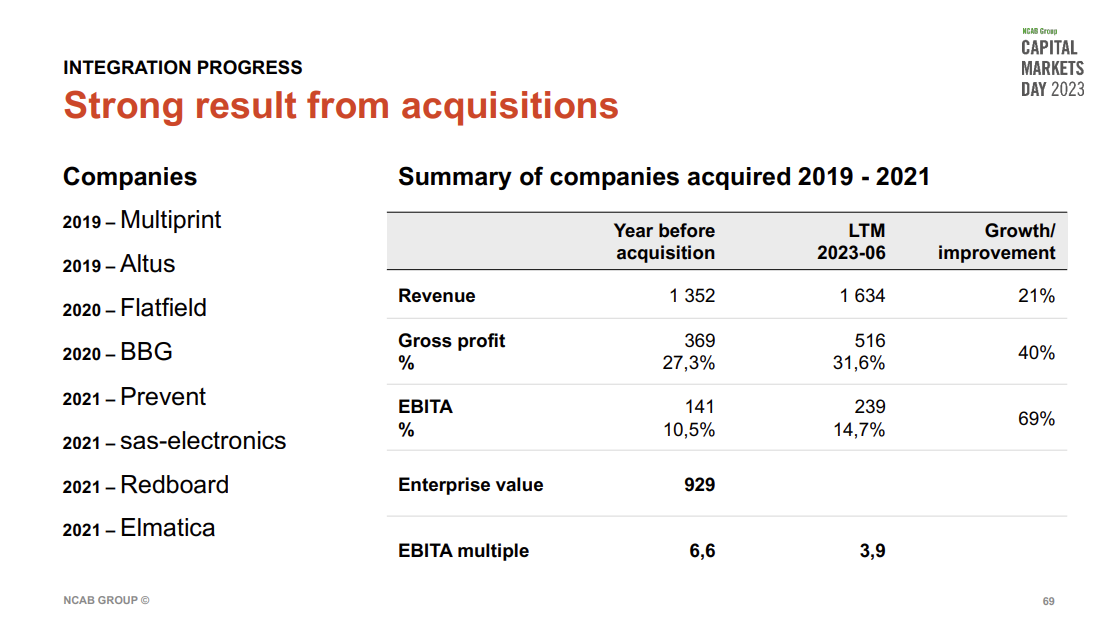

They have been able to consistently improve their acquired targets both in terms of gross profit margins, revenue growth, and EBITA margins.

Particularly impressive or thought puzzling is how the market seems to underappreciate their acquisitions, as the multiple on acquired targets seem to compress. At any rate, paying an average of 6.6 times EBITA for their targets from 2019 - 2021 shows good discipline. Another important factor that suggests that NCAB does some good M&A is that they have a focus on smaller targets. This is an important qualitative factor in that if they miss, the drag caused by the acquired company won’t hit NCAB to hard.

During their capital market day in September 2023, they reported that they have around 51 companies in their M&A pipeline, out of a total of ~200 PCB trading companies. This means that they have plenty of targets, and with a strong operational cash flow, they have the ability to continue buying targets at a good price. With the aforementioned headwinds blowing harder, some good opportunities might present themselves in the time to come.

This combination of well-executed M&A and an underlying robust organic growth has yielded good results:

Plenty of market growth

I also really like the fact that NCAB are still very much in their early innings of growing. The HMLV market was in 2022 assumed to be worth roughly $25bln (out of a total PCB market of $80bln). The main producing region is China and Asia (ex. China & Japan).

As we can see from the above chart, Europe and USA consume far more than they produce, whilst China and Japan produce more than they consume. NCAB has a leading position as a global player in PCB supply, but they are still quite early in their market penetration

The company also expects the underlying growth of the PCB market to have a very healthy CAGR going forward:

NCAB aims to capture their piece of the growth cake through 4 avenues:

Geographical expansion driven by M&A.

Market consolidation by leveraging scale for cost and capability advantages.

Fully focused on PCBs.

Deepen customer relationships and increase market share in existing markets.

An asset light business in an asset heavy sector

I’ve ocassionally mentioned that NCAB is an asset light business. We can know this as the company do not own and operate the factories from which they source PCBs, but rather optimise and pick them through diligent processes.

Being asset light basically means that the company does not hold a lot of assets in capital heavy property, plants or equipment. Industrials typically have a lot of capital in their physical means of production. I’ve given a run-down of the qualitative side of NCABs asset-lightness, but let’s look at two ratios that highlight this: PPE / NOPAT and PPE / Operating Revenue.

We can observe that the metrics that can tell us something about asset-weight in NCAB are as follow:

PPE / Operating revenue: 0.05

PPE / NOPAT: 0.47

Said in other terms, it’s quite clear that the capital bound up in physical means of production (in NCABs case, inventory) is quite low compared to the operating revenue and profits generated by their business.

Another important metric for NCAB is how quickly they can turnover PCBs from the factories they work with, to their customers. We can observe this through inventory turnover.

A higher rate of inventory turnover is better than a low one. We can see that the Covid-19 pandemic hit NCABs turnover and it’s almost halved from the top levels of 2018 to 2022. Now we see inventory turnover pick up again, indicating normalising inventory levels post-covid which should continue to lead to less capital tied up in physical stuff, and more returned to the company for higher levels of reinvestments which we want.

We should expect PPE to pick up as they grow their customer base. If they manage to pick up inventory turnover this should lead to the higher base of PCBs distributed more quickly to more customers and giving a higher generation of earnings.

Growth ambitions

During NCABs market day last fall, they had high confidence in achieving net sales of 8bln SEK in 2026 (LTM ~3.7bln SEK) and an EBITA of 1bln SEK (LTM 605,8mln SEK). Currently, this seems to be an overly ambitious goal. On 1. October they revised their sales estimates by 10% and they expect negative impacts on EBITA margins and sales growth in both Q3 and Q4.

But, let’s assume that NCAB shaves of 1bln SEK in sales, and 150mln in EBITA (greater than the 10% revised guidance). These are still goals that point us to a 37.5% sales growth and EBITA growth of ~18.5%.

This is probably also to ambitious. The company now expects sales of between 880 to 900mln SEK for Q3, and an EBITA between 110 and 120mln SEK. They ended the profit warning with the following statement:

Even if it means that the turnaround in the market is some time away, it does not affect our general view of our growth opportunities in the medium and long term

- President and CEO of NCAB, Peter Kruk

Still, they might post results far below expected going forward, and the headline of the Q2 report was “Darkness still looms in Europe”. Grim news.

Short and medium term growth seems to be a bit up in the air, but that’s what this article is all about. The headwinds are blowing, let’s hold onto our hats and try to separate the trough from the rest.

Management alignment and experience

NCAB has a management that has been there for a lot of it’s history. Christian Salamond, the chairman of the board took the company from a smaller Swedish company focused on the nordics and run by the former passionate founder Lars Östlund. Salamon has been with the company since 2007.

The current CEO, Peter Kruk, took over the reins of the company in 2020 after long time CEO Hans Ståhl retired. The largest shareholders are currently major funds and asset managers. Salamond owns around 2% of all shares outstanding, so given the size of his wealth this is surely enough to create alignment.

More importantly is how they work with promoting key personell. NCAB has a strong tradition from promoting from within, which is a trait I value highly of my companies. However, there is a bit of a difference between AQ and NCAB in the founder-factor.

In the overview of the group management, we can see that all of the key managers of the company has share ownership to various degrees. This is something I find positive.

What I don’t like

Reliance on PCB production in China: This being a shallow dive I haven’t been able to figure out the exact amount of PCB NCAB sources from China. But given that China has a dominating presence in the production of PCBs, it’s fair to assume NCAB is heavily dependant on Chinese production. This puts the company in a bit of a pickle in regards to macro-tensions.

Core markets being in Europe: I think that this is what is creating an opportunity to get in at the current valuation. But given the scale of their reliance on European industry, which is struggling quite a lot, it might prove a sticky endevaur to turn the profit ship. I doubt European industry is dead, so I hold a more positive view than the doomsayers on the region.

Cyclical business: The PCB markets are highly cyclical. I believe that NCAB can leverage this to further ingrain themselves in both sides of their network, but shareholders should expect a bumpy ride.

Ownership structure: I would’ve liked to see ownership being more in the hands of institutions or individuals with a keen sense and ambition.

Forward communication: I’m skeptical of NCABs growth ambitions, and their intention of communicating in this way. We have seen many EMS companies be far to positive, for far to long and it’s a shame that NCAB has this same style of optimism. I only hope they have a handle on the long-term growth targets, but I assume they are going to miss their medium-term ambitions.

Dilution: Share count has increased by 4.7% annualy the last 10 years, mostly due to acquisitons. I still don’t like it, but at a glance it’s been accretive to the business strength and earnings.

Valuation

NCAB Group is a cyclical business in the midst of a what seems to be a generational industrial downturn in Europe, their largest market. I tend to not look to much at cyclical businesses, and find it hard to evaluate their normal valuations, but I’ll take a stab at it anyway.

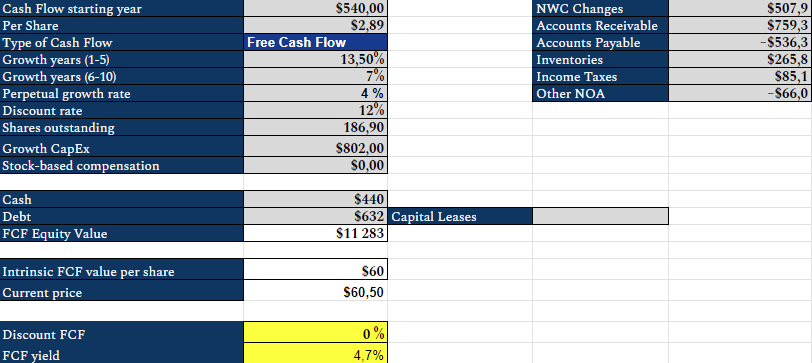

I’ve performed a reverse DCF, looking at what amount of growth the market is pricing in per H1’24 report:

As we can see, the market is assuming around 13.5% growth in the coming years, with a halving of the growth in year 6-10. I’ve also set an unusually high perpetual growth rate at 4%, but I believe that given the historical growth of PCB market (which has been around 4%) it is fair to assume a rather high long term growth for the market as PCBs are used in more stuff.

Further I’ve done a quick run-down playing with some future assumptions on EV/EBITA basis. I’ve assumed a decline in FY24 EBITA and a result of 500mln SEK EBITA (a 22,7% decrease compared to FY2023 EBITA). In addition I’ve assumed a compression of multiples to 18 EV/EBITA (a 18.2% multiple compression). This does not take dividends into account for the IRR.

This shows that we need quite some growth to see a good return on our investments. With the assumption that the market is pricing in (13.5% 5yr growth) we see that we will get sub-par returns on our investments at the current share price of around 60-61 SEK, also at the bear case we arrive at 3.3% return on investment over the five years. If the company manages to get around 18.5% growth in EBITA (which aligns with their guided growth for FY24) we willl see a nice investment return.

It’s a bit harder to see surety in investments on NCAB. I however think it is a bit of an unfortunate time to assess this, as we are in the midst of the darkest trough in the European industry and we are assuming that the current market dynamics and exposures is what will be NCABs future market dynamics and exposure. There’s also an rather attractive FCF yield at around 4.6% currently. I think they have shown the ability to expand both geographically and in the current markets, and think that the headwinds are at it’s highest intensity currently. I have therefore initiated a position at around 4% of my portfolio.

Summary

Having provided a discussion on both NCAB and AQ Group, I want to summarize the thesis quickly.

I view these as attractive investments into one of the most dominant trends we have currently: Electrification.

NCAB works in a more capital light and efficient way, with more focus on using their two sided network to achieve great synergies both for their customers and producers. They lend their competencies and network to both sides, and creates agile processes. The first thought that struck me when I understood the combination of M&A and integrated growth with their customers was: Is this Vertical Market Hardware? And I sort of believe it’s not the worst way of looking at NCAB.

AQ Group is on the other side. They are integrated into their customers value chain with highly efficient, great quality and timely deliveries on complex jobs that are hard for competitors to try to steal. AQ Group is focused on themselves, and doing the best job for their customers. With a level headed management and an excellent culture they manage to grow with the same flywheel as NCAB - organically with their high-quality customers, and inorganically through M&A scaling.

Both are decentralised and have a culture of entrepreneurship going back to their founders in highly fragmented and demanding sectors. It fits my strategy like a glove.

Score on investment pillars

NCAB Group

Ability to reinvest well into business growth: Average ROIC at 27,84% over 10 years.✅

Competitive advantages: Yes - scale advantages and only global supplier of HMLV - gross margins at 38,2% and operational margins at 14,3%.✅

Fundamental growth: Achieved a 24,2% annual NOPAT growth over 10 years. ✅

Skilled management aligned with investors: Management is aligned through both stakes of ownership and incentives.✅

Low or no debt: Solidity of 40,6% and a cash flow that well manages the debt. ✅

AQ Group

Ability to reinvest well into business growth: Average ROCE at ~15% over 10 years (which is a good return for an capital heavy company).✅

Competitive advantages: Yes. AQ Group exhibits quality at a scale advantage with deepening customer relations - gross margins at 54.5% and operational cash flow margins at 13.8%.✅

Fundamental growth: Achieved a 19% annual NOPAT growth over 10 years. ✅

Skilled management aligned with investors: Management is aligned through both high stakes of ownership and incentives.✅

Low or no debt: Solidity of 64% and a cash flow that well manages the debt. ✅

I hope this has been a piece that adds some value and highlights how I think both on a thematic and individual company level. I have been looking to add some industrial exposure to my portfolio, and I am happy to position myself within industries looking to benefit from the secular trend of electrification.

If you enjoyed this article, I just want to take a minute of your time to say thank you! There are many ways you can give back: Leave a comment with criticsm or feedback - I really enjoy discussing with other engaged investors and feedback is what helps me grow.

You can also subscribe to my publication, or share it with a friend you think would get some value out of reading it. And if you are especially generous there are ways you can pitch in: Either by buying me a coffee through the button below, or buying a subscription on my favourite investment data platform: Finchat.io. You get a 15% discount, I get a part of the sales - win win baby.

Anyway: Thank you for reading this article, I much appreciate it. Never hesitate to reach out to me, you can reach me through Substack or on Twitter @ikkenopes.

Have a lovely weekend!

As always, none of this is investment advice or a recommendation to either sell or buy shares in the discussed companies. I hold shares in both, and you should remember that I have a positive bias towards these companies.

I am not authorized or experienced enough to be accounted as someone who should be listened to in how you manage your money. Please ensure to do proper research and due dilligence before investing in anything I discuss. I can not be held accountable for any action taken after reading this blog. My writing is purely entertainment and ramblings from a hobby investor looking at stuff I find interesting.

Loved this one, especially the parts digesting their business models. Will be very interesting seeing how these develop. I also find OEM International and HMS Networks as companies I want to watch closely, if valuations were to fall further.

I think you copy past gross margin and operating margin. Both are mentioned same.