Interesting Insights - August 2024

Just another regular month in the markets.

Dear readers,

Yet another month has passed, and the moon has circled the earth yet again. It’s been a busy month for me, travelling for work in two of the four weeks with weekends spent trying to squeeze the last drops of summer with friends.

This month I’ve released one article, going through my portfolio holdings and musing over the various changes I’ve made to my portfolio. If you haven’t caught it yet, you can read it here:

Some of the changes I made have in the short term proved to be rather lucky ones. Both Alimentation Couche-Tard (-9.6%) and Dino Polska (-8.3%) have had a pretty torrid month.

Ironically, Alimentation Couche-Tard launched news that I view as potentially great news, and Dino Polska showed better results than what I feared. ATD has launched a bid to acquire Seven & I Holdings, potentially increasing the canadian retailer scale substantially, and giving attractive inroads to the asian market. There’s obviously a long way forward before we know if the bid succeeds, but I’m very surprised the market has reacted negatively to the news. A way to explain the negative reaction might be the market fearing that the only road to real growth for ATD in scale, is through large acquisitions. When it comes to M&A, size compared to origins is often a big risk factor, however, I would find it hard to bet against ATDs M&A track record.

Without talking too much about a company I no longer hold, I found Dino Polskas results to be rather OK given the news of other retailers. With DNPs stronger margins, better-than-inflation LFL sales, longer growth runway and strong niche position, I would bet that the company will succeed in taking further market share in Poland.

The reason I’m spending some time talking about past holdings is that I find this to be a good example of trying to explain outcomes of decisions. If I wanted to, I could celebrate having “outsmarted” the market, and try to claim that my fears materalized and I didn’t have to bear the brunt of the downside. But that’s not at all what happened. The timing of my sales were pure luck, and if I had continued to own stocks in these businesses, I would be bullish about the catalysts that caused this drawdown. However, I also don’t see this price drop as a must-buy opportunity. They are both well run companies, that I prefer to not own at the moment due to a mix of factors discussed in the article on my holdings shared above.

Portfolio news

This month the half-year reporting has continued and several of my companies have presented. Luckily, most of my holdings have shown excellence this quarter as well, but we should not be to happy about these short term movements. Easy come, easy go.

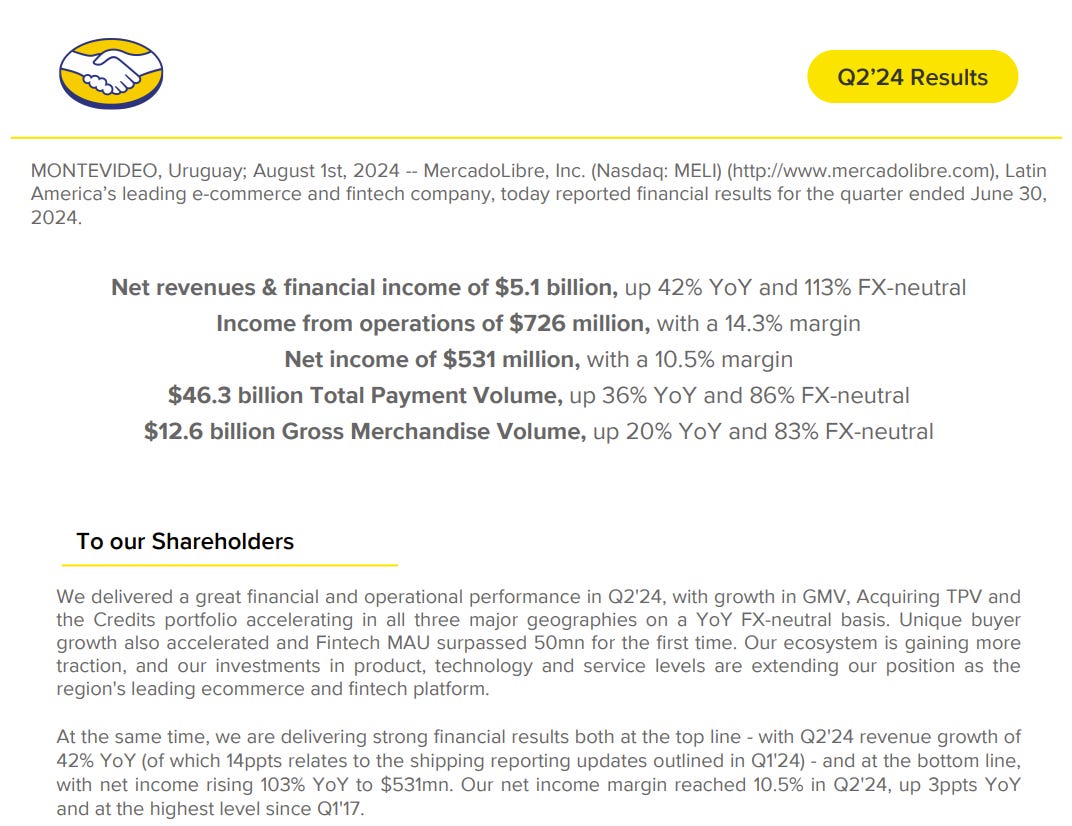

MercadoLibre

The South-American e-commerce giant delivered excellent results for the first half year. If you haven’t, I really recommend reading the shareholder letter of MercadoLibre.

As the company themselves say, the results were great. There’s honestly not much to add, other than the fact that they have shown strength across all segments. For my readers who are disappointed at the brief comment I’m making on MercadoLibre, I can only recommend reading this article summarizing the results excellently:

Norbit

Before I touch on the second quarter for Norbit I would like to briefly take us back to the first quarter results that were presented that were 15.05. The company reported results that if we looked at it isolated, were disappointing. Personally, having read the results and listened to the management, it was obvious that the sales experienced short term volatility and cyclicality. The headline numbers caused an intraday drop of somewhere between 5-9%, taking the share price down and briefly almost eradicating any gains made for the first five months of the year (I believe we touched sub-60 very briefly).

Looking back, this was quite the opportunity. As we can see from YTD total return, the company has been on a tear. For shareholders of Norbit, it is important to remember that the sales in the Ocean and Connectivity segments often experience intra-year volatility. This also happened in Q3 2023, after H1 2021 and so on. This sales and ordre volatility is something that the management has talked about extensively, and I continue to be surprised at the outsized reactions to single quarters. However, these reactions are opportunities for investors with a longer view than some single quarters.

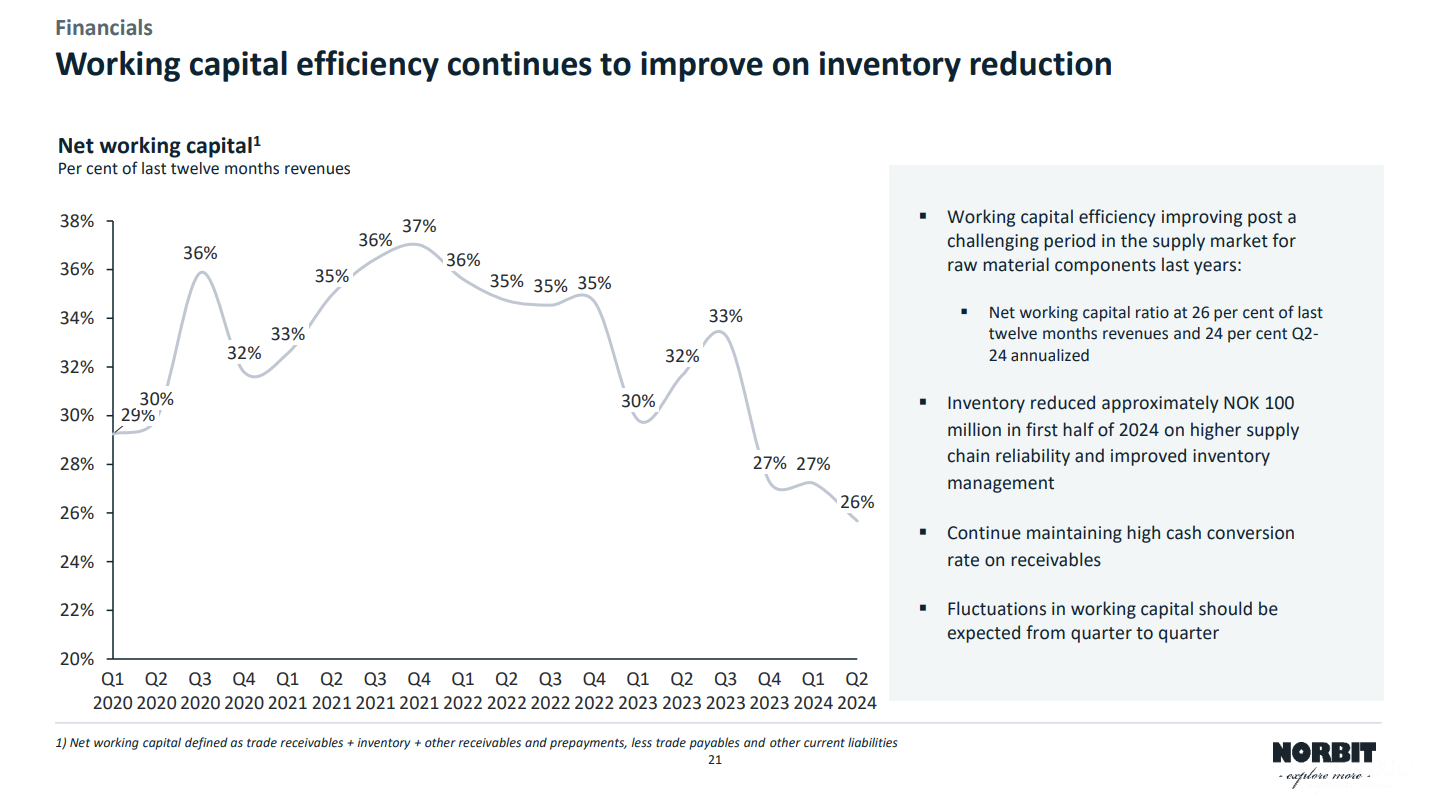

The opportunity of the Q1 results have now become evident to all Norbit investors (and would be investors). The H1 results were excellent, and Norbit showed an all-time high revenue in Oceans, a (well known) weaker quarter for Connectivity due to the delay of a large order in the segment and a surprisingly strong EBIT margin of 24% for Q2, taking the H1 EBIT margin to 17% after a disappointing Q1. There was also a small, but welcome, improvement in the margins in the PiR segment, landing at a 15% EBIT margin (Q1 8%). And shareholders should be very happy with the continued improvement on working capital effects, as illustrated by the below slide from the Q2 presentation:

Norbit reiterated their strong long-term guidance, which is always nice to see. I would however, not be to surprised to see them raise guidance, or achieve the goal of 2.75bln revenue before 2027 due to the strong addition of Innomar (remember that the the revenue guidance was for organic growth though).

Innomar have been described by both management and analysts as accretive, and the German company’s technology fits as a glove to the rest of the product portfolio. Innomar also shows better EBIT margins and should add to the growth velocity of Norbit well. The plan is to allow Innomar to operate alongside and in a decentralized manner with Norbit, which should limit the potential for mismanaging an integration of the product. By allowing Innomar to exist as a portfolio company, they should be able to reap benefits of scale and synergy, and avoid tampering with the existing customer relations and sales of Innomar products. If Norbit is a new company for any of my readers, I have a previous deep dive on the company, which you can read here:

If you appreciate my writing, pitching in for a cup of coffee is much appreciated and provides a proper motivation boost:

Constellation Software & spin-outs

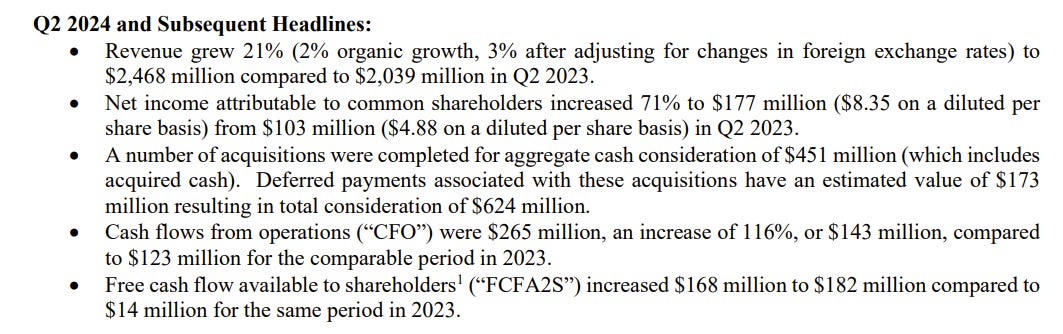

As I wrote about in my portfolio article, I now own the breadth of the CSU-universe. All three companies reported earnings in august. I bought into both CSU and Lumine after their reported Q2s. Constellation surprised me by showing a better value and better growth at stand-alone figures. Seeing the apparent over-focus on Topicus and Lumine thanks to their perceived longer runways for growth made me realize I had done the same mistake.

On a free cash flow available to shareholders (FCFA2S) level the results continue to show great strength, with H1’24 compared to H1’23 increased by 34.46% for Constellation inc. spin-outs which is just immensly strong results. On a quarter to quarter basis the numbers were even more impressive, but it is important to remember that this is a result of big deals that do not come often, and the effects of these deals have been well known for a while:

I'll briefly touch on the Q2 results of Topicus and Lumine. I would say that it was business as expected for Topicus. We are still waiting for an acceleration in acquisitions from the Europe-focused spin-out. I think investors should remain a bit cautious of overestimating the fragmentation of Europe as a potential for a high M&A runway, as the fragmentation on the flip side also means higher complexity and more competition in diverse national markets. Anyway, Topicus saw a 14% YoY revenue growth, and despite a small sum of acquisitions by €16.6mln they have a M&A pipeline of around €54mln in H2.

With Lumine they experience a bit of headwind due to the timing of their M&A strategy of carveouts, which typically leads to larger and fewer acquisitions. Having completed a couple of big deals this time last year, the comparables are tougher for Lumine. This, however, lead me to get a chance to open a position in the company.

For the best coverage I know on Constellation Software, I highly recommend everyone to either engage with or plain out subscribe to Compounding Tortoise. Here is his summary of the groups Q2 results:

O'Reilly Automative Analyst Day

I won’t delve to much into this as I’m planning to do a write-up on business culture using O'Reilly as a case study, amongst others. However, I’d like to show some interesting (but known) slides that they used in their analyst presentations.

As we can see, O'Reilly has a lofty ambition of being the number one player in all it’s markets. The way they do this is pretty simple, but not easy: by having the parts the customer needs available, or being able to deliver these parts faster than others and having knowledgeable and passionate service people providing assistance to customers coming to their stores. As CEO Brad Beckham himself said it:

Well, again, at O'Reilly, we work in a pretty boring industry and we are a pretty boring company in terms of it's very solid. It's basic fundamental execution and its basic leadership of people. Again, no revolution needed.

I recommend everyone interested in the company to use the two hours or so to tune into the analyst day, and listen to the team talk about the secret sauce of O'Reilly: culture, efficiency, and unmatched service.

I haven’t really done a lot - I’ve bought a teeny tiny portion of Omda AS (currently at around 2% of my portfolio). I’m still not really sure whether or not I’ll sell or build this position. Other changes have been described in the earlier mentioned post on my portfolio construction (linked above).

What I’ve read and listened to this month

Fantastic episode of Founders that brings up a bunch of lessons and aspects of great leadership and company management:

The spirits business have had a rough time lately, and I find Campari to be one of the most interesting companies in this space. Read this great introduction to the company:

To complement this piece on Campari, it’s worth it to listen to this episode on the general spirits sector:

I have been on a Constellation binge lately, and revisiting one of the original takes on the company makes for a great read:

This was an interesting take on investing checklist:

A very nice and condensed list of lessons from the NBIM on the topic of what makes a good investor:

This discussion on Baskin Wealths performance in the first half was a nice listen:

For my Norwegian and nordic readers I recommend this great chat about quality investing on the StockUp podcast with fund manager Bernt Berg-Nilsen.

If you appreciate the work I do there’s two primary ways to support my writing: Either by purchasing a Finchat subscription through my affiliate link or by buying me a cup of coffee.

Nothing I’ve written in this post should be understood as investment advice. This is purely for informational and entertainment purpose. I’m just an amateur writing about stuff I learn and read about, so please don’t think I’m someone that you should base any investment decisions on.

Thank you for highlighting the MELI write up