Interesting Insights - April 2025 edition

We're on this Donald Trump shit

, 1918 Reproduction")

Dear readers,

My portfolio has swung from barely breaking even in early April to a robust +10.3% year-to-date, with a striking 15% gain this month alone. As tech giants like Meta and Microsoft deliver reassuring results, digital markets stabilize while physical economy indicators flash warning signals. We're navigating a marketplace shaped by Trump's social media updates, actual policies and conflicting economic currents.

This tension between digital strength and physical weakness creates opportunities. I'm eyeing TFI International, the Canadian truck-freight giant, though cash constraints limit my immediate moves. For those interested in transport sector value plays, this rollup specialist deserves attention.

I’ve found this year to be summarized by Mac Millers song from 2011, which I quite often listen to as I’m running my intervalls. Because we are for sure on “This Donald Trump shit”.

Without further ado, let’s jump into the portfolio.

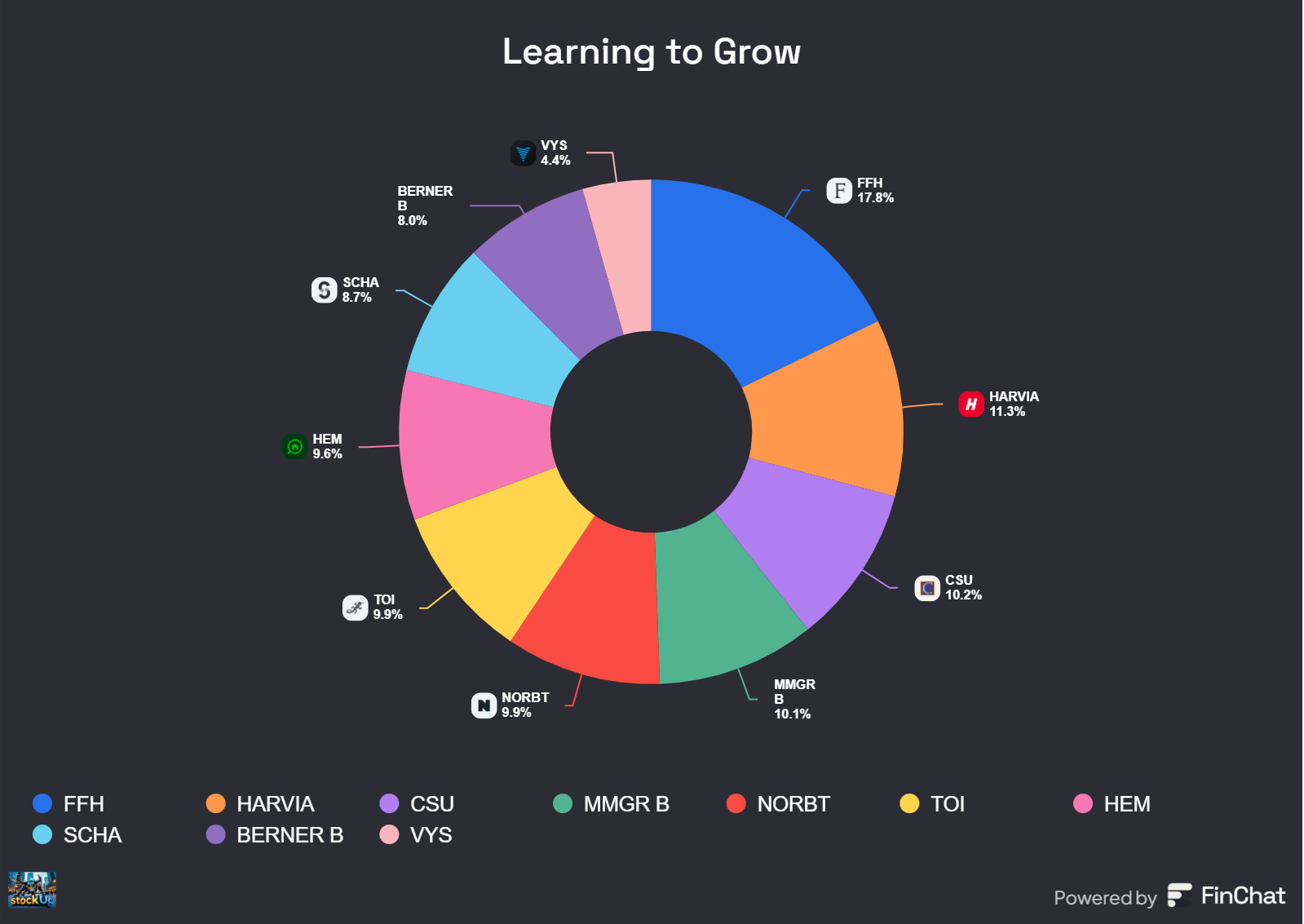

Portfolio Updates

My returns have risen quickly this month, largely helped by great development in Berner Industrier, Norbit and a recovery in Harvia. Detractors have been Momentum Group and Hemnet. The latter I was too quick to enter, as I mistakenly thought that markets wouldn’t price the share for a pricing package that was not operational in Q1. Oh well. I am looking to probably buy more Hemnet, and maybe some more Momentum Group as well.

Adding to these two names would probably happen on the expense of Fairfax Financial. Not because I think FFH is expensive, or have any troubling signs on the horizon, but because it’s simply to big. I have had a tendency to get carried away, and size positions a bit to large. Having taken some learnings from my Evolution and SanLorenzo mishaps, these misses could’ve impacted my returns to a lesser extent if I’d simply not get carried away by the valuation. But on the other hand, buying in to negative trends is often a sign of the contrarianism often adored by value investors and Buffett-disciples. This is something I want to avoid, which is why I haven’t bought more Hemnet and Momentum already.

The conundrum I find myself in is: Fairfax is a bit to big - I’ve come to learn that I am most comfortable with a portfolio where positions aren’t bigger than 15%. Why did Fairfax end up being as big as this? Well, I bought the dip in FFH on the tariff fears. It’s been a good little portfolio trade so far, as I’m up around 15.3% on my dip buy. But, Fairfax is developing more nicely than Momentum and Hemnet. Should I then listen to the sizing tactic of my portfolio mangement, or the “own the winners” tactic? I haven’t decided yet.

Earnings

Since my last update in the first quarter letter several of my holdings have released their earnings. Let’s spend some short time on each

Hemnet

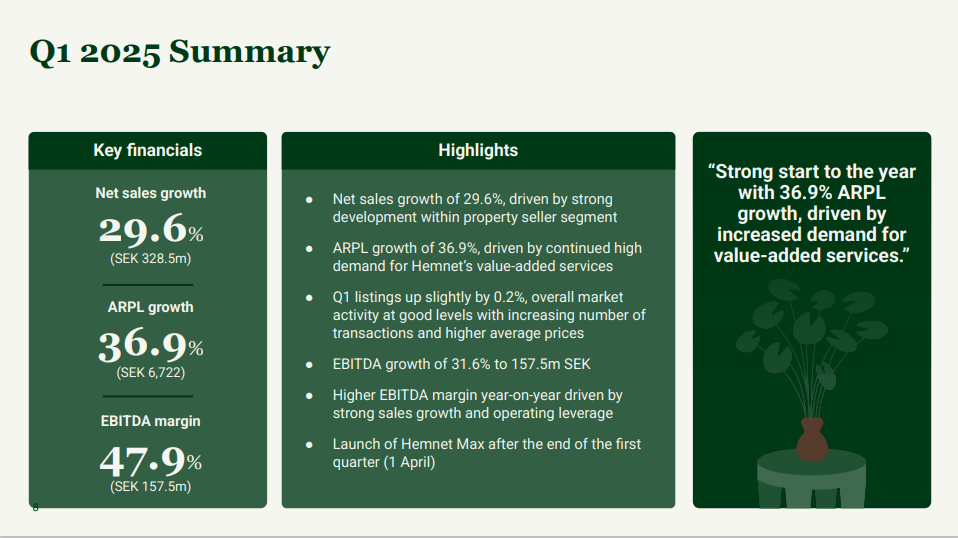

The leading online classifieds market for real estate in Sweden reported what is quite frankly stellar results:

Despite this, the market reacted negatively and the shares fell from ~380sek to ~318sek on what has been seen as a miss to estimates (Net sales growth came in at 29.6%, and not >30.x%). In the trade up to the release, the share price appreciated much because analysts raised their estimates for 2025. This raise was largely made because the new pricing package, Max, is coming online after the end of the first quarter. Mr. Market wasn’t paying enough attention it seems.

The results we got were quite frankly excellent, and exceeded Hemnets long-term goals of 15-20% growth. It is important to keep in mind that there is some cyclicality in listing sales, tied to how the real estate market works: The first quarter is not a good month for sales, simply because it’s a dreary period.

Hemnet grew it’s average revenue per listings by ~36% from Q1 2024, despite a flat volume development. It’s a testament to the pure pricing power of Hemnet.

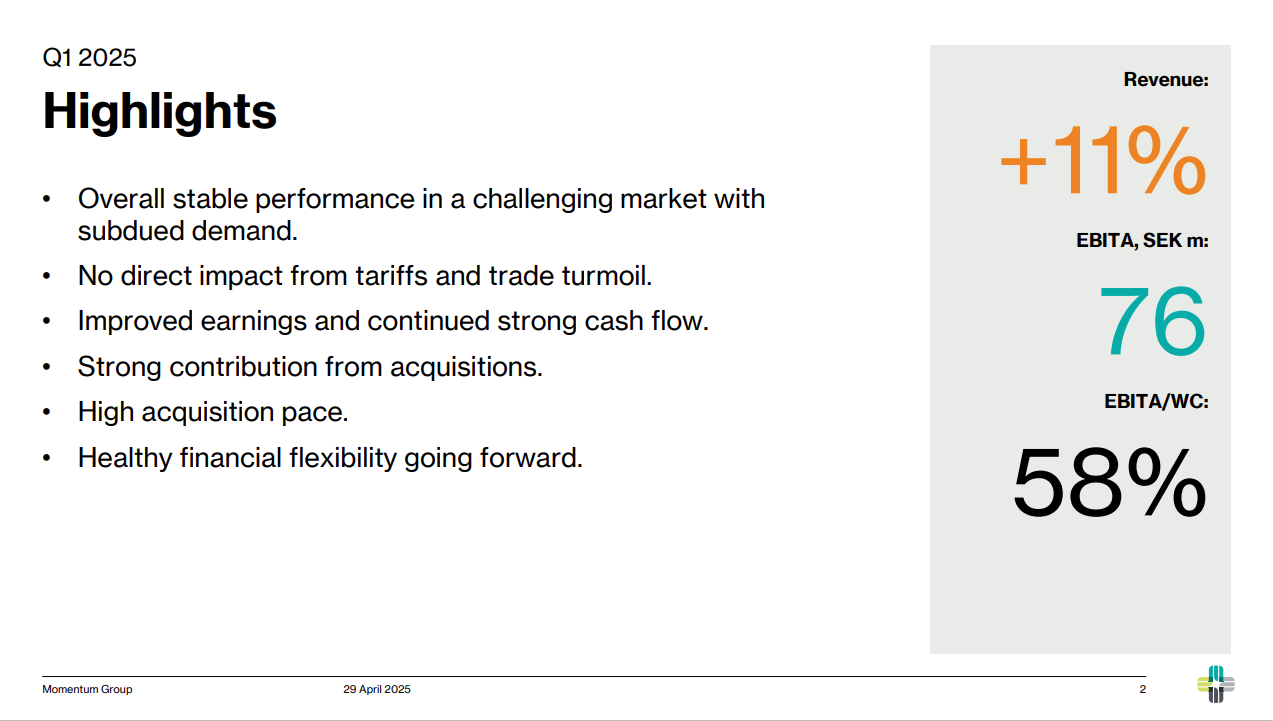

Momentum Group

The serial acquirer reported a rather stable, but slow quarter. Revenues increased by 11%, driven entirely by acquisitions as growth in comparable units was -1%. This shows two things:

They’re keeping up pace with acquisitions well, mostly through cookie-cutter acquisitions.

The industry in the Nordics is still not very active.

On a R12 basis the performance was driven largely by the infrastructure segment which grew EBITA by 48% (but a -4% performance in Q1. Industry however posted a 4% R12 EBITA result, with a stronger Q1 at 7% growth. Mixed bag of a quarter, but given how much cash Momentum Group have acquired a turnover of roughly 104mln SEK (adjusted for ownership % and currency) and are en route to greatly outpace the level of acquisitions in 2024. Q1 was in other words a very strong quarter for acquisitions, and with their latest acquisition of Håland Instrumentering in the south of Norway, Momentum Group have entered a new country which should be exciting in and off itself.

Given that we’re only in the beginning of May, Momentum Group are in line to present their second best acquisitional year. 2023 was a special year, as they acquired Askalon which accounted for 317mln in turnover for 2023. I.e., if we normalize out the “exceptional” acquisition of Askalon, we should probably expect a record year for Momentum Groups programmatic smaller acquisitions. The purchase price consideration in Q1 (ex. Håland) was 170mln SEK with lease obligations added back. So we see some good cash deployment, and the group is chugging along as expected.

Berner Industrier

My freshest serial acquirer posted some very strong results in Q1, but most importantly they announced the acquisition of Autofric. This naturally sent the share price soaring - as it’s a confirmation of Berners acquisitional strategy.

Autofric will add 60mln in revenue, with good profitability. Autofric posted a ~16% EBITA margin in 2024, significantly higher than Berners average EBITA margin of 7 - 10% these last years. Add in that Autofric has had CAGR of 22% in the period 2017 - 2024 and this looks like a highly accretive deal. In addition, the price paid is at between 5.6 - 8x EBITA (depending on how the earn out optionality lands), and a 0.9x sales multiple.

Let’s assume that Autofric grows a bit less than 22% due to macro uncertainty (not likely to affect Swedish water treatment demand that is driven by old pipes and new regulations), and we say a 15% growth from ‘24 - ‘25 with a 15% EBITA margin and we land at 10.35mln in EBITA from Autofric. This adds around a normalized 17.5% of EBITA in 2025 for Berner on a stand-alone basis. This goes to show the low hurdle rate for growth at Berner from acquisitions alone.

Now, that would be great if we assumed it was an isolated growth factor. But as Q1 results came it, we got confirmation that cash flow, order intake and profitability in the excisting base of businesses all are developing nicely as well.

With orders up 18.2%, EBITA up by 26.3% and debt reduced by 16.3% we it’s quite clear that things are running very well for Berner even without any acquisitions. If we take order intake of the last two quarters to be indiciative for the coming growth ex. acquisitions, we are bound to see very good growth for Berner in 2025 and 2026. And, the positive optionality is that if they acquire 1-2 companies each year, we very quickly see and added 15% - 30% growth added through acquisitions on top of a core that is hitting is stride. It’s no wonder that share price is up by 43% the last month.

Fairfax Financial Holdings

Fairfax Financial Holdings released their Q1 earnings, delivering significant outperformance versus analyst expectations. The company reported EPS of $42.70, substantially beating estimates of $25.15 - a 70% beat to estimates. Net profit after tax (NPAT) increased by 23.82% year-over-year, largely driven by realized investment gains of approximately $1 billion. However, operating earnings declined by 23.5%.

The combined ratio deteriorated to 98.5% from 93.6% in the previous year, primarily due to losses related to California wildfires. The California fires alone amounted to a 690mln loss.

Analyzing the insurance segment more closely and adjusting for the extraordinary costs of the California fires, insurance service results reached $1.3 billion, representing 25% growth. When normalizing for catastrophe events and assuming the California wildfires never occurred, Fairfax's combined ratio would have been approximately 88-90% - indicating solid underlying performance.

The market appears to be mispricing Fairfax's business fundamentals, underestimating both their insurance operations and investment capabilities. Despite periodic catastrophe losses being an inherent part of the insurance industry, Fairfax's diversified business model continues to demonstrate just how robust they are.

Historically, FFH has delivered top-tier investment returns and maintains a strong position to continue this performance. Their investment portfolio grew by 5.3% during the quarter, imo it shows the strength of their value-based portfolio. It looks to me like analysts (and the market as a whole) fully discount out any and all realisations of investments. This is probably going to continue to allow Fairfax to outperform expectations going forward, as they have a portfolio primed for outsized gains.

In summary, while Q1 results were impacted by California wildfire losses, Fairfax's core economics remain exceptionally strong with impressive earnings outperformance, substantial investment gains, and healthy growth in their insurance service business. There's a ton of moving parts in this quarter. The investment gains were big enough to off-set the California fires and more so. It would have been an home run without this extraordinary catastrophe. FFH looks set to continue outperforming the market, and the analysts low expectations.

What I’ve enjoyed learning about this month

Liberty’s Highlights continue to be one of my favourite writers on this platform, for more than just investing. Well worth the follow:

Double trouble Topicus-edition:

Both

and have written good pieces on Topicus, which is having a stellar year in terms of acquisitions, capital deployment and share price development:

I really enjoyed this discussion on time horizons and investing:

Great discussion on how to think about success in investing

Addtech is the company within the B&B-family that I’ve spent least time on, so big thanks to

for sharing his work on the company:

Podcasts:

I loved this meandering talk with David Marcus in connection with Redeyes serial acquirer conference:

Given that David Marcus talks about Brad Jacobs’ book “How to make a few billion dollars”, I find it prudent to remind my readers about this great episode (which I featured earlier, but I’ve listened to it at least three times):

Another one from Investing by the books, this time about how we struggle to separate share price development and management quality:

Niklas from Redeye get’s three episode mentions from me! Here he guests TIP to talk about Serial Acquirers:

For those of us that speak and understand Nordic, and specifically Norwegian, this episode is a great listen:

And a bit untraditional, but I’ve also spent a substantial amount of time listening to Atomic Habits by James Clear on audiobook - A wholeheartedly warm recommendation, it’s a book with a ton of learnings relevant for anyone into investing.

As always: None of this should be understood as investment advice. I am a hobby investor, with no professional training. I may sell or buy stocks without disclosing it at once, so you should not be following me. Do your own research, or you are bound to lose conviction when convicition matters.

Thanks for the mention, really appreciated. Also interesting to understand more on Berner Industries!

Thanks for your April insight! Your portfolio changed enormously. Is this part of your strategy to change your holdings that much within months? I also opened a position in MMGR and HEM. HEM is more of a watchlist position for me, as I feel uncomfortable with the current valuation. That said, the moat is quite impressive at the moment. But technology is always more fleeting than a serial acquirer 😉

How do you value Topicus?

I’d love to learn more about Asseco and the entire group of holdings – ACP, ASE, ABS – but there doesn’t seem to be much information available out there. Did you do some research on them?

Also, have you ever looked into Pinetree? (It's run by Mark Leonard’s son, apparently 😉)