Shaping an investable universe

Creating a field of focus and structuring potential portfolio candidates

Dear readers,

I have been thinking about my own activity lately. Most of the investors I admire share a trait I have been very bad at inhibiting myself. The trait I am talking about is: Inactivity.

Having reflected on why I am prone to activity, I have narrowed it down to two suspects:

I love researching, and I get excited when I uncover new ideas.

I am still shaping my investment process and strategy.

In terms of the first point, I notice that I have a tendency to use investing and research as a way to learn new things but also for entertainment purposes. I love understanding new businesses and figuring out what makes some companies better than others.

This unfortunately leads me to wanting to invest in these companies. With a limited supply of money, this has a tendency to make me sell. This is not how I want to act in regards to investing.

When it comes to the second point, I am more forgiving. This is the first year where I am putting as much thought, research and effort into my investment process. I am learning a lot of new things every month.

Throughout this year, I have made many stylistic and strategic choices. This has mostly had a restrictive effect on my investing. I have decided to not invest in many things, such as biotech, financials, and cyclicals (i.e., commodities, energy, and so on). I want to avoid these to simplify my own process and control for downside risk. There are definitely great companies in all these categories, but I don’t think I have any edge in assessing them and find them hard to own over long periods of time.

Narrowing my field of vision

I want to start digging in, and not expanding to much. I’ve therefore decided to add a decision-making speedbump to my process. From now on, I will be operating with a portfolio of watchlists. If I am to add a new company, the potential investment must have resided in my watchlist for at least three months. In addition to this I will of course ask myself some common-sensical questions:

Does this add a potential greater upside than what is in my portfolio already?

Will this addition spread out revenue streams and reduce risk of losing money?

Would I be able to own this company forever?

I want to continue to run a moderately concentrated portfolio of between 8-15 stocks. Currently I own shares in 11 companies (I count Topicus and Constellation as one). The company count hits a sweet spot for me - enough to get some diversification and limit overlapping risks.

In my portfolio run-down I introduced several themes I want to be invested in. I grouped these within three themes (and I later added another theme in electrification):

Niche dominators

Capital allocators

Wealth creation

Electrification

I am not entirely sure how happy I am with this categorization, as they don’t align on conceptual levels. However, this is all done to provide some system to my thinking.

My watchlist will not be based on these themes. I aim to be flexible in what themes I invest in, as long as they make sense over the long term. I aim to create an investable universe of excellent companies that I would be happy to own. For the baskets, I structure them within classical sector definitions: consumer defensive & cyclical, industrials, capital allocators, technology and healthcare. I have been considering having one for luxury as well, but struggle to find enough names to have it make sense to organize them in a watchlist.

I don’t want to have to many names to follow (no matter how tightly I will monitor the companies), and I will try to keep it somewhere between 30 - 50 companies.

Introducing my investable universe

I will briefly introduce each company in my investable universe. You can see key metrics such as revenue and EPS growth, ROIC and margins in the tables. I will put a ⭐ behind the name of the company closest to entering my portfolio currently.

Consumer defensive

Dollarrama

A Canadian dollar store running an extremely efficient business selling necessities with a bunch of smart moves, such as no fresh produce, not a lot of stuff that needs refrigeration, and so on. They have a strong value proposition for customers and are expanding at a high pace and profitability internationally.

Domino’s Pizza ⭐

An excellently run restaurant franchise selling cheap, but well made pizza and other snacks globally. They’re running their top-level business as well as their franchisees at high returns on capital, highlighting how well this business is ran. Great management that steered them through a highly successful turn-around. Some times referred to as a tech company that just happens to sell pizza. I am especially fond of how they use operational leverage, and the fact that they have leftover pricing power compared to peers.

AutoZone

I already own O’Reilly Automotive, which is situated as the second largest position in my portfolio. AutoZone shares many of the same business traits as ORLY. Well led, sector winning company gobbling up shares and steering through up and downcycles extremely well. I would like to own AutoZone as well as O’Reilly due to AZO expanding internationally and really carving out their space in attractive auto parts markets such as Mexico and Brazil.

Europris

A Norwegian discount retailer that has a track record of excellent returns over market cycles. They’re well led, manages their expansion admirably and has been a growth engine in a slow market over very long periods of time. I am often fond of Norwegian companies, both due to a home bias but also thanks to the fact that I get no taxation on dividends and so on. A potential candidate for a slow and steady dividend payer in a tax friendly account.

Industrials

Linde PLC

A global industrial gas and engineering giant that's essentially running a duopoly with Air Products in many markets. They supply essential gases and engineering solutions to numerous industries from healthcare to manufacturing. Their business model features long-term contracts, high switching costs, and consistent capital returns. They've shown excellent execution in merger integration and maintain industry-leading margins through operational excellence. I did the grave mistake of selling my position in Linde earlier this year, and I still haven’t forgiven myself for that.

Borregaard ASA

A Norwegian specialty biochemicals company that transforms wood into high-value products like vanillin, cellulose, and bioethanol. They've carved out strong positions in sustainable alternatives to petroleum-based products. Their biorefinery concept maximizes value extraction from raw materials, leading to superior margins and returns. Strong R&D capabilities keep them at the forefront of bio-based solutions and they are a true quality company that keeps on surprising on the upside.

NCAB Group AB ⭐

A leading global PCB (Printed Circuit Board) supplier and trader. They've built their competitive advantage through rigorous quality control processes and deep relationships on both sides of their business. Their asset-light model combined with technical expertise generates high returns on capital while serving an increasingly critical part of the electronics supply chain. This is a typical industrial consolidator, operating in a sticky niche. I wrote more about NCAB in this post.

ASSA ABLOY

This Swedish company is a global leader in access solutions, from traditional locks to digital security systems. They've built their position through both organic growth and smart acquisitions in the fragmented security market. Their transition towards electronic and digital solutions has created new revenue streams while maintaining strong positions in traditional markets. High aftermarket revenue provides stability through economic cycles. I love how defensible this company is, and would really like to have it as a pillar in my portfolio.

Otis

The world's largest elevator and escalator manufacturer, with an incredibly profitable service business model. Sometimes cheekily referred to as a SaaS-business: Safety as a service. Their installed base creates recurring revenue through maintenance contracts, while their R&D positions them at the forefront of smart building technology. The business combines stable service income with growth from new installations, particularly in emerging markets. The new installations part is less important than their recurring revenue, but creates different growth levels in different macro-climates.

Fastenal

A leading industrial and construction supplies distributor that's revolutionized their sector through onsite locations and vending solutions. Their innovative approach to distribution, including their FAST Solutions program, has created strong customer relationships and recurring revenue streams. They've consistently shown ability to grow market share while maintaining industry-leading margins through operational efficiency. They do all this through best-in-class value creation for their customers, and unrelenting focus on making their customers lives easier.

Consumer cyclical

Harvia Oyj ⭐

I love saunas, and have a membership at my local sauna club. I get a bit giddy every time I spot a Harvia oven (just ask my girlfriend who has to endure me talking about it every time I do spot one). Harvia are a leading global producer of anything sauna related. They're riding the global wellness wave, but what really makes them special is how they've turned the ancient practice of sauna-making into a high-return modern business. They're not just selling heaters - they're capitalizing on the world's growing obsession with wellness while maintaining that coveted Finnish sauna expertise. What's particularly clever is how they've kept their capital-light model while expanding globally. Their expansion is being executed at high levels of capital proficiency, and they are really crushing their competitors.

Games Workshop Group PLC

This British company has managed to build a money-printing machine around plastic miniatures. There are almost nobody more passionate about their hobby as Warhammer miniature collectors. The beauty of Games Workshops business lies in their complete control - they own the IP, write the stories, make the miniatures, and sell them through their own channels. Add in that their customers often spend hundreds of hours painting each miniature, creating an emotional connection you rarely see in retail. They have also started to expand their licensing products with highly successful video games and a TV deal with Amazon on the horizon.

Sherwin-Williams Company

Everyone thinks watching paint dry is boring until you look at Sherwin's numbers. Sherwin-Williams have built an empire by understanding one thing perfectly - professional painters care more about consistency and service than saving a little bit of money on paint. Their store network is so dense that no painter needs to drive more than 15 minutes to get their paint. Combine that with their color-matching expertise and contractor-focused service model, and you've got yourself a beautiful business that just keeps compounding through every housing cycle.

Alimentation Couche-Tard Inc.

The Owl was started by a group of friends in Quebec, and rose to global dominance through the hard work and vision of Alain Buchard. They've turned the humble convenience store into a global growth machine. What I love most is their discipline - they'll wait years for the right acquisition, but when they move, they move fast and integrate brilliantly. They're always experimenting too - whether it's with fresh food concepts in Norway or EV charging stations in their European operations. Circle K might be their global brand, but their real brand is operational excellence. The 7-11 negotiating that has been going on lately has been a nail-biter, but despite probably not happening it was a bold plan showing the sustained growth vision of ATD.

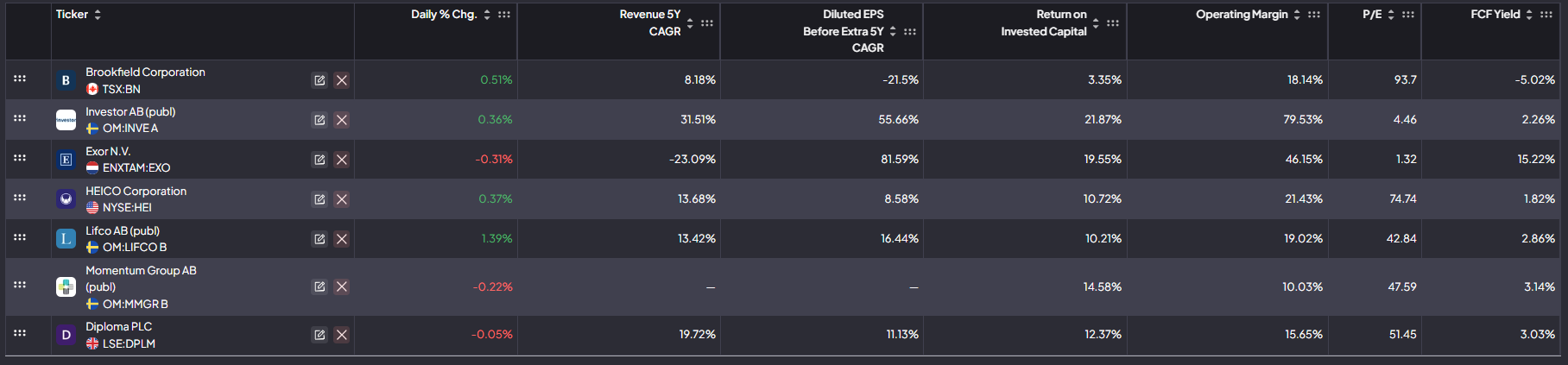

Capital allocators

Brookfield Corporation

One of my favorite capital allocators globally. Bruce Flatt and his gang have mastered the art of alternative asset management while maintaining significant ownership in their managed assets. What stands out is their contrarian approach - they're often buying when others are fearful, whether it's office buildings, infrastructure, or renewable energy. The complexity of their structure sometimes scares investors away, but their long-term track record of compound returns speaks for itself. I would love to earn Brookfield so that I get an exposure to private assets and important infrastructural investments.

Investor AB

This Swedish investment company owns some of the most well managed companies in the world, and practice a “own and improve” philosophy. Run by the famous Wallenberg family, they've been compounding capital for generations through both listed and unlisted companies. Their secret sauce? A remarkable ability to pick and develop market-leading companies while maintaining a super long-term perspective. They own stakes in everything from ABB to Atlas Copco, and their track record of developing these businesses is simply stellar. It’s like owning a Swedish compounder ETF where seasoned management is involved in improving the businesses and sharing best practices across a global handful of world-class industrials.

Exor N.V.

This company started as FIAT's holding company, this Agnelli family-controlled investment vehicle has transformed into something far more interesting. They're really good at capital allocation, owning controlling stakes in Ferrari, CNH Industrial, and more recently, luxury players like Christian Louboutin. What impresses me most is how they've evolved from traditional industrial roots to becoming sophisticated investors across various sectors while maintaining their industrial discipline. I am adding this mostly because I think the pricing is ridicolous, the NAV discount is quite high right now, but I am not sure I agree with how they value several of their holdings. Their industrial holdings are however almost priced for obsoletion, despite being conservatively and well-run.

HEICO Corporation

These guys have carved out an incredible niche in aerospace aftermarket parts. Instead of building entire planes, they make FAA-approved (think off-brand things, but just as good or even better) replacement parts at a fraction of OEM prices (think high-end brands made by the plane companies themselves). Their business model is beautiful - high margins, strong barriers to entry, and a management team that's proven masterful at bolt-on acquisitions. The founding family still owns a significant stake, aligning their interests perfectly with shareholders. I love how they operate, and seem like an expertely run company in one of the most sticky sectors in the world.

Lifco AB

A Swedish serial acquirer specializing in niche market leaders across dental, demolition, and construction equipment. They operate with a highly decentralized model allowing acquired companies to maintain their entrepreneurial spirit while benefiting from group-level advantages. Their acquisition playbook has proven extremely successful with consistent double-digit returns and strong organic growth in their portfolio companies.

Momentum Group AB

This swedish technical components and products company that's turned the seemingly boring industrial supplies business into a cash-generating machine. Their decentralized approach keeps entrepreneurial spirit alive in their subsidiaries while leveraging group purchasing power. They're not trying to reinvent the wheel - just executing incredibly well in their niche. It’s a new spin-off from the Bergman & Beving universe, having been a part of great companies such as Addtech, Addlife and Alligo.

Diploma PLC ⭐

British specialist distribution at its finest. These folks have perfected the art of distributing highly technical products across several niche markets. What I love about their model is how they combine technical expertise with high service levels, making them indispensable to their customers. They're not just moving boxes - they're solving problems, which explains their consistently high returns on capital. Add in the fact that they have a acquisitional expertise, having done a lot of great deals recently. I simply love this company and I am looking to find a spot in my portfolio.

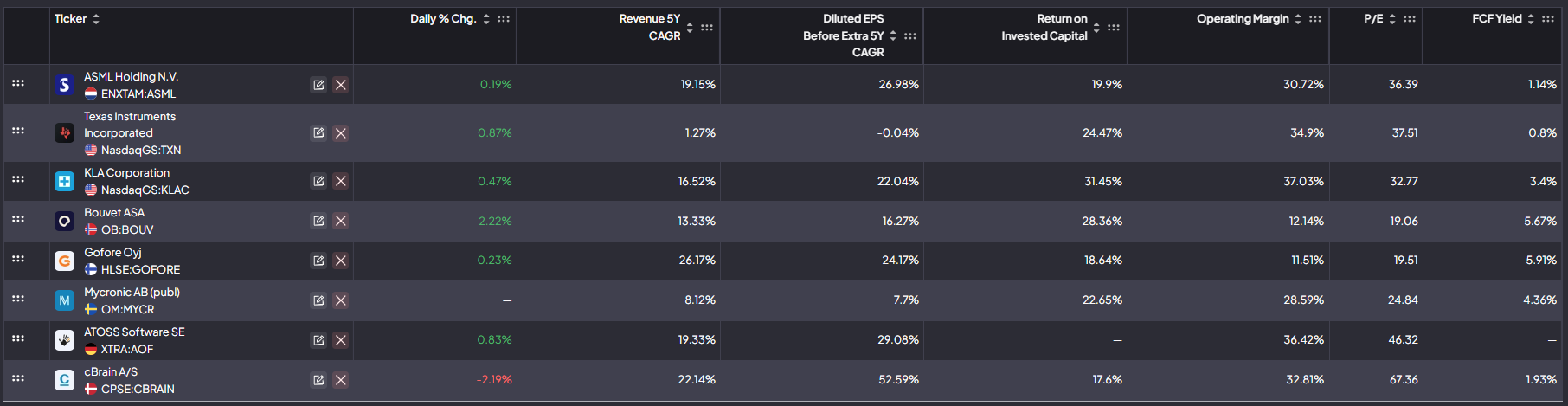

Technology

A note on this watchlist before proceeding with the company introductions. I tend to shy away from a lot of tech companies. I find them hard to assess, and I find the competetive landscape difficult to understand. I however think there are plenty of great companies that can be great investments that I want to monitor, and at least have half an eye on.

ASML

Imagine having a complete monopoly on the most critical machines needed to make advanced computer chips - that's ASML for you. They've created something truly extraordinary: a machine that costs hundreds of millions, yet has customers queuing up to buy them. Their deep understanding of physics, combined with their network of specialized suppliers, has created an almost impenetrable moat. I don’t understand nearly enough of their technology, but they make hyper complex technology and are essential for the current AI expansion.

Texas Instruments

While everyone chases the latest chip technology, Texas Instruments has built an empire in analog chips - the unsung heroes that connect our digital world to reality. Their brilliant strategy? Buy older factories at pennies on the dollar, then use them to make chips that barely change but are absolutely essential. They’ve got an extemely long trackrecord of great capital allocation, returning nearly all free cash flow to shareholders while maintaining their technological edge. Despite AI stealing the headlines, this old handheld calculator manufactorer makes the components that make our electrical world run.

KLA Corporation

Ever wondered who inspects the inspectors? That's KLA. They've carved out a fascinating niche making the machines that test semiconductor manufacturing processes. In an industry where a speck of dust can ruin a million-dollar chip batch, their tools are irreplaceable. Their market share in critical process control steps is quite high, and they've turned this position into a cash-generating powerhouse. I like these niche plays on big trends.

Mycronic AB

A Swedish precision technology champion that dominates several niche markets in electronics manufacturing. Their mask writers for display production are particularly impressive - they're practically the only game in town for certain critical applications. They combine Swedish engineering excellence with smart market positioning, creating several mini-monopolies in their chosen segments. Their fundamentals are stellar, and they keep hitting it out of the park.

Bouvet ASA⭐

A Norwegian consulting gem that proves you can build a fantastic IT services business without the usual race to the bottom. They've created a culture where consultants actually want to stay long-term - a rare feat in this industry. Their focus on the Nordics, combined with their deep client relationships, has resulted in remarkable stability and returns. They have deep customer relationsships, and their products and services are saving money for their clients. Their data monitoring and efficiency processes are deeply embedded into their customers businesses, creating long lasting relations.

Gofore Oyj

Another Nordic consultant. These Finnish digital transformation specialists have managed to grow organically while maintaining quality. What makes them special is their transparent culture and ability to attract top talent in a competitive market. They've built a reputation for actually delivering on digital promises - something surprisingly rare in the consulting world. Their public sector expertise provides stability while they expand into private sector opportunities. Gofore has highly (perhaps to high) ambitious growth goals, and are currently establishing a foothold in the DACH markets. I am looking forward to following them going forward.

ATOSS Software

German efficiency personified in software form. They've turned workforce management into an art form, becoming absolutely crucial for their clients' operations. Their transition to a SaaS model has been brilliant - maintaining high margins while building an even more predictable business. The German Mittelstand loves them, and they're gradually expanding their success formula across Europe. They make their customers lives better whilst achieving high capital returns, in an underpenetrated and fragmented global market where they’ve just started expanding outside their home markets.

cBrain A/S

A Danish government digitalization specialist that's turned the typically slow-moving public sector into a growth market. Their F2 platform is fascinating - they claim to have decoded the DNA of public administration and turned it into software. Their high retention rates and expanding footprint in German public sector shows they've cracked the code of selling complex software to government clients - no small feat indeed. Their software is a sort of one-stop-shop for any bureaucratic system handling cases, files and reports which makes data easier to assess and processes swifter and more nimble. The sell makes it sound like a bit of a wonder product, and I am currently happy to watch from the sidelines while I try to understand if it’s too good to be true or just really good.

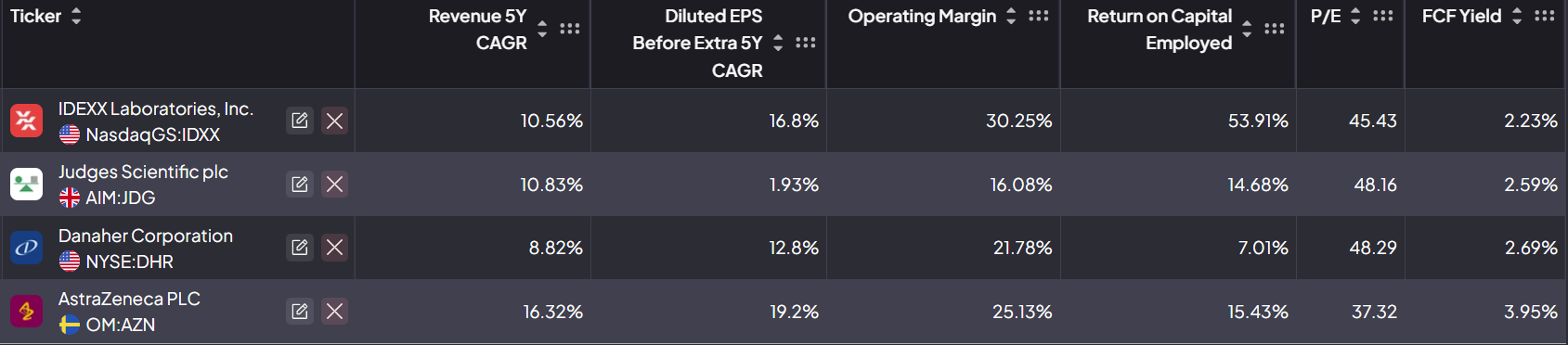

Healthcare

I’m slightly sceptical towards my ability to pick any winners in biotech. I think there is other dynamics in some technology and health service sectors. These are complex fields on many levels: Regulatory, technological, demand and competetive it’s hard to know the winners and stayers from the laggards. In the same manner as with the technology bracket, I want to keep an open mind and choose to follow a set of companies in the health sector.

Idexx Laboratories

Who would’ve thought that one of the highest quality companies in public markets make a living out of diagonising pets? Idexx has made a brilliant razor-and-blade model around veterinary care - their instruments sit in vet clinics worldwide, generating recurring revenue from test slides and reagents. They make a living out of simplifying treatement through effective diagnosis of animal illness. Pet ownership soared in the pandemic, and the growth has slowed down the last days - but we are increasingly becoming more attached to our four-legged friends. They also provide diagnostics for farm animals, and water tests to identify harmful infections. The moat they've built through software integration and customer relationships is remarkable, and they keep innovating in a market they essentially created.

Judges Scientific

A British serial acquirer which has delivered stellar results from acquiring small, niche scientific instrument makers. Their model is beautifully simple (and recognisable): find owner-operated businesses making essential scientific instruments, buy them at sensible prices, then let them operate independently while implementing proper financial controls. What's clever is how they focus on instruments that scientists simply must have - often cited in academic papers by brand name. Each subsidiary might look small, but together they've created a compound growth machine that would make any investor smile.

Danaher Corporation

Danaher is a legendary name within the health and life sciences sector. The amount of companies which have headhunted a former Danaher manager to lead their business is quite long, and the Danaher Business System is lauded by many as the gold standard of innovation and corporate culture. They've mastered the art of acquiring companies in life sciences and diagnostics, improving them through their operating system, and then watching the returns soar. Their recent Aldevron acquisition shows they haven't lost their touch. The spin-offs of Fortive and Veralto demonstrate their ability to create value through both building and separating businesses. With a legendary reputation comes a stiff price, but this is definitely a name to monitor.

AstraZeneca ⭐

This is not your typical pharmaceutical company. Under Pascal Soriot's leadership, they've transformed from a struggling pharma giant into one of the most impressive drug developers globally. AstraZeneca is the healthcare jewel of the Investor AB portfolio which is expertly managed by the Wallenstam familiy. Probably best known for their Covid-19 vaccine which ended up not being the best one on the market. When it comes to what is good: Their oncology portfolio is particularly striking - they've built it from almost nothing into a powerhouse. They have a fascinating scientific development process, with an best in class approval rate. Their research partnership model, especially strong in China and at Cambridge, shows how modern drug development can work at its best. The way they've rebuilt their pipeline and reputation in just a decade is nothing short of remarkable.

Thank you for reading!

As always, if you enjoyed this article, feel free to subscribe or share - it greatly helps the growth of the blog. I also welcome any comment, question or critique. Especially the latter, that is afterall how we learn the most!

If you want to support my writing you can do so in several ways: Buy a Finchat.io subscription (if you like their tools, which I would think everyone would do!) through this link. You get 15% off any subscription, I get a cut of the deal - we all win.

If you prefer a more direct way, you can buy me a coffee through this link:

But in the end, I just appreciate you taking the time to read my ramblings. Have a lovely week!

None of this should be viewed as investment advice. I can be invested in any of the names listed above, and would invest without disclosing so first. Remember, you can’t borrow conviction - so do your own damn due diligence.

Quality content. Always wanted to learn about more European companies, especially Nordic. Subscribed. Thank you!

It's eerie how closely aligned our portfolios and target companies are. As a US investor myself, it's harder to get a good, local feel for European companies. Most of the ones I have settled on you have also written about (here and in your portfolio). Gives me a little validation, in some respects.

A few more from your region that I have been following (or purchased) that might align with your methodology:

-ChemoMetec (Denmark) - Missed my opportunity at DKK380, now have to wait. Notable growth and profitability in biologics/MA/CGT

-Admicom (Finland) - No idea if their ERP (construction focused) is really that popular and growing in Finland/Nordics

-QT Group (Finland) - substantial profit and growth from opensource licensing, and also has an IT consultancy portion of the business